CBDCs gain ground as monetary policy falters

For decades, monetary policy has been treated as the central lever of economic management. Interest rates and quantitative easing were expected to steer inflation and define the money supply. That model is now becoming obsolete. The structure of the economy has shifted and political pressures have intensified. Yet the core mechanisms meant to support growth have remained unchanged.

The rise of central bank digital currencies (CBDCs) is ostensibly a modernizing alternative that offers attractive benefits. However, this response risks reinforcing the very problems it is meant to address.

New tools, old approaches

Central banks were designed to operate independently of the whims of successive governments, but in practice they are often influenced by highly charged policy environments. Moreover, in many advanced economies, debt levels have reached historic highs. This constrains the scope for monetary tightening, as higher rates increase servicing debt costs and expose underlying imbalances.

Alongside these longstanding challenges, which have intensified in recent decades, new inadequacies are emerging as financial markets fragment and digitize. The transmission of monetary policy depends on the traditional banking system, but financial intermediaries are rapidly evolving. Capital markets, shadow banking, fintech platforms and cross-border flows all dilute the impact of policy decisions.

The rise of digital finance has further exposed these limitations. Payment systems, savings vehicles and even forms of money are evolving faster than regulatory and policy frameworks. Stablecoins, tokenized assets and platform-based financial services operate alongside traditional structures.

It is against this backdrop that CBDCs have emerged. By creating a new form of central bank money that can operate within digital ecosystems, policymakers aim to modernize the monetary system itself. The digital euro is no longer a theoretical exercise. It is moving through design, consultation and political negotiation stages that point to a high likelihood of implementation.

One argument often evoked in favor of a European CBDC is the continent’s growing reliance on American infrastructure for digital payments. Yet this risks misdiagnosing the problem. When viewed through an institutional lens, the solution naturally appears to be another public instrument. But the issue is not the absence of a state-backed digital currency. It is the relative weakness of Europe’s own innovation ecosystem. Reducing dependence on foreign platforms will not be achieved by introducing a new form of public money, but by creating the conditions for competitive private solutions to emerge and scale. Without that, a digital euro risks adding a new layer to the system without addressing its underlying imbalance.

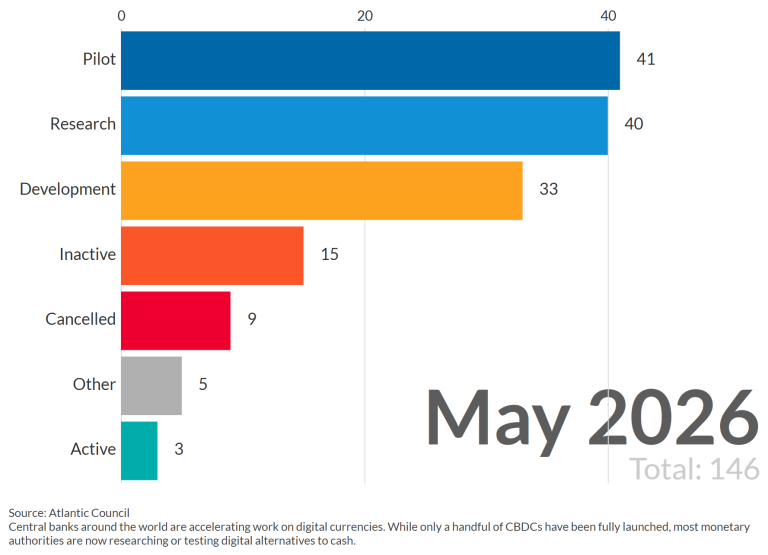

Facts & figures: Number of countries and currency unions exploring CBDCs

A similar logic applies to the question of monetary sovereignty. The United States is actively promoting dollar-backed stablecoins to reinforce its currency’s global role in the digital age. At the same time, some central banks are seeking to diversify away from the dollar, even as its dominance remains entrenched. In this context, CBDCs are often presented as a way for Europe and others to reassert control.

This argument, too, risks missing the point. Sovereignty cannot be engineered solely through new monetary instruments. It rests on the credibility, openness and dynamism of the underlying economy. Rather than attempting to counter U.S. influence with a new state-backed currency, Europe would be better served by enabling its private sector to innovate and compete on equal footing.

Technical and operational pitfalls

CBDCs promise several advantages. They can anchor trust in public money in a digital age, provide a resilient payment infrastructure and potentially enhance the effectiveness of policy transmission. They also offer a way to respond to the rise of private digital currencies while preserving monetary sovereignty. But these benefits come with potential threats.

The first major risk is that people and businesses shift their money away from banks and into CBDCs. Banks could lose a reliable source of funding, making it harder to lend, forcing them to rely more on unstable funding sources and increasing volatility in the financial system. Even with safeguards such as holding limits, the mere existence of a risk-free digital alternative alters incentives. In stress scenarios, the movement of funds could be rapid and destabilizing.

As such, CBDCs could accelerate digital bank runs. In a crisis, the ability to instantly transfer funds into central bank money may amplify panic rather than contain it. What was once a gradual process mediated by frictions becomes a real-time shift. Managing these dynamics would require new tools and constant calibration, adding complexity to an already challenging policy environment.

Another concern is the impact on monetary policy itself. While CBDCs are intended to improve transmission, they also introduce new uncertainties. The relationship between interest rates, savings behavior and credit creation may change in unpredictable ways. Design choices will have far-reaching implications. A digital currency system inherently increases the visibility of transactions. Even with safeguards, the perception of state oversight could undermine trust and adoption. Striking a balance between privacy, compliance and functionality is not straightforward. Too much control risks eroding civil liberties.

As part of critical national infrastructure, CBDCs will need to be resilient to cyberattacks, system failures and technical vulnerabilities. The scale and sensitivity of the system make it an attractive target. Dependence on external technology providers could also introduce new strategic risks, particularly if key components are not fully under sovereign control.

There is also the question of competition with private money. CBDCs could crowd out innovation if they dominate the payment landscape. Alternatively, they could fail to gain traction if they do not offer clear advantages over existing solutions. In that case, private platforms and stablecoins could continue to expand, potentially weakening the role of public money. Their success depends on design, regulation and user adoption, none of which can be taken for granted.

CBDCs are often framed as a tool to preserve monetary sovereignty; however, foreign CBDCs could circulate across borders, and private digital currencies could remain attractive. If domestic CBDCs are poorly planned or slow to scale, they may fail to achieve their intended purpose.

Legal and governance issues add another layer of complexity. Decisions about access and usage rules raise fundamental questions. Who decides how digital money can be used? Under what conditions can it be restricted or redirected? These questions have political and societal implications that extend well beyond central banking.

Finally, there are transition risks. The shift from the current system to one that includes CBDCs will not be seamless. It will require coordination across institutions, regulatory adjustments and public acceptance. Missteps could lead to confusion, fragmentation or a loss of confidence. The transition period itself may be the most fragile phase.

CBDCs are not a simple solution to the shortcomings of existing monetary policy. They are part of a broader transformation that introduces new trade-offs. Citizens therefore have a critical role to play, and expectations should be high. Transparency and accountability are essential. The design and implementation of CBDCs will shape the financial system for decades.

The direction is becoming clear, but the starting point is far from ideal. Monetary policy, in its traditional form, is no longer sufficient for the demands of a digital and interconnected economy, yet it has already been strained by years of mismanagement and mounting imbalances. At best, CBDCs will offer a partial solution to the problems they seek to address. At worst, they risk becoming a retrenchment dressed up as modernization.

Scenarios

Most likely: CBDCs reshape finance without replacing it

CBDCs are introduced gradually. Central banks first deploy wholesale versions, with retail CBDCs following, but only on a limited scale. Safeguards such as holding limits prevent large-scale shifts away from bank deposits. Stablecoins are regulated and integrated into the system. Banks continue to play a central role, and monetary policy evolves incrementally rather than undergoing a radical overhaul.

Moderately likely: Fragmented monetary system with competing forms of money

The monetary landscape becomes more fragmented. CBDCs coexist with bank deposits and regulated stablecoins, each serving different functions. Users and firms choose between them based on convenience, trust and specific use cases. Central banks expand CBDC functionality over time, potentially introducing more targeted or programmable features. At the same time, private actors continue to innovate. The system becomes more competitive and complex. Managing interactions between different forms of money becomes a key policy challenge.

Less likely: Disrupted transition driven by instability or weak adoption

The rollout of CBDCs encounters significant challenges. In one scenario, a crisis accelerates adoption, leading to rapid shifts to central bank money and amplifying stress in the banking system. In another, CBDCs fail to gain traction, leaving private platforms dominant and public money less relevant. In both cases, the transition is uneven and potentially destabilizing. Policy trade-offs, particularly around privacy and usability, undermine confidence. The outcome is either a more fragile system or one in which CBDCs fall short of their strategic objectives.