America’s innovation economy solidifies its leadership

Several important events occurred in the economy this June. Topping the list was the record initial public offering of SpaceX, which will be followed by two IPOs in the artificial intelligence sector: Anthropic and OpenAI. On the less positive side, inflation remains elevated and public debt continues to soar across the developed world, including in China. Central banks are trying to deal with these challenges, but monetary policy alone is no longer sufficient. The euphoria surrounding a reopening of the Strait of Hormuz will likely prove short-lived.

The SpaceX IPO was remarkable not only because of its size and valuation. The company is a conglomerate, a structure that investors are normally cautious about. It includes businesses in space exploration, communications and surveillance, such as Starshield and Starlink, as well as X in social media and AI. So far, only one of these businesses is profitable.

Space exploration especially is a very long-term venture that will require substantial additional investment. Break-even or positive operational cash flow appears far away. However, space exploration is likely to generate numerous secondary innovations, making the project valuable even if the “colonization of Mars” appears utopian. History shows that utopias can become reality, although often in a different form than originally imagined.

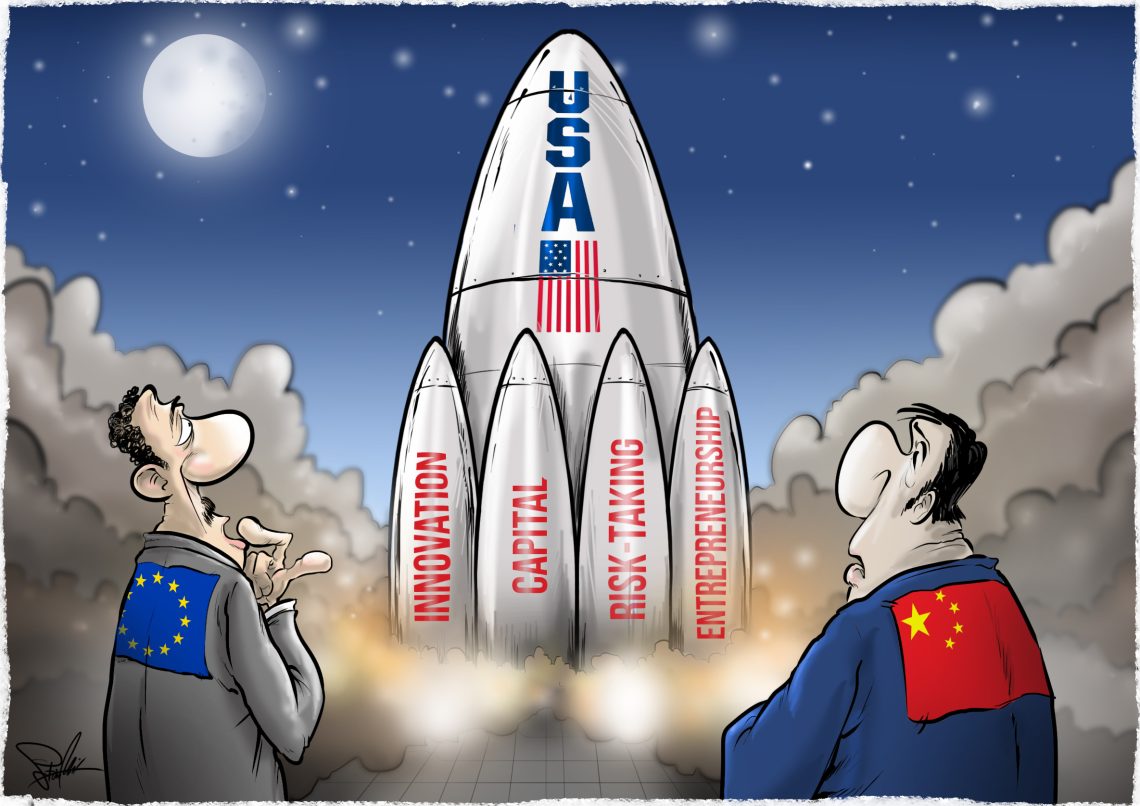

There are reasons to be more optimistic about the American economy than about other large economic blocs.

Ambitious space projects demonstrate entrepreneurial courage and a healthy willingness among investors to take risks. The appetite of the capital markets will be tested further by the forthcoming IPOs of the two aforementioned AI giants, Anthropic and OpenAI. The technology sector may already be overvalued and could become even more so, resulting in corrections. However, this does not appear likely to discourage innovation in the United States.

This entrepreneurial spirit, together with the size, professionalism and risk appetite of American capital markets, is one of the foundations of the growth and resilience of the U.S. economy, strengthening its global leadership.

The threat of inflation and public debt

Inflation remains a global threat, linked in the industrialized world, including in China, to public debt and oversized government. Central banks of the world’s most important currencies met in mid-June to decide on interest rates and discuss inflation. However, excessive government spending, which is itself inflationary, makes it difficult to fight inflation solely through higher rates. The U.S. is certainly not a shining example, and the situation is increasingly problematic. A related issue that is often ignored is implicit debt. Implicit debt, particularly pension and healthcare obligations, is higher in Europe. Debt-servicing capacity is supported by higher productivity in the U.S. China faces the largest challenge due to the combination of rapidly declining demographics and low per capita productivity.

There are, however, other reasons to be more optimistic about the American economy than about other large economic blocs.

We have already discussed the capital markets. Although the U.S. consists of 50 states, it has one large and highly flexible capital market. It is a market that searches for the best opportunities and is not heavily influenced by bureaucratic or technocratic planning. Healthy regulatory and economic competition among the states makes the economy even stronger.

In China, by contrast, government influence remains dominant in the allocation of capital, meaning market priorities are often secondary. The European Union and its member states have still not succeeded in establishing a truly integrated European capital market. The technocratic centralists appear to believe that a prerequisite for such a market is not only the internal market – which makes sense – but also a common economic policy and regulatory system. This would eliminate what still remains of healthy competition.

Productivity and demographics

Due to its demographics and size, China has a chance to become the world’s largest economy, though not necessarily the strongest. Chinese per capita productivity remains only a fraction of that of the U.S., while American productivity continues to increase by roughly 2 percent annually. China, with its doctrines of communist centralization, Marxism and the concept of a “socialist market economy” – a contradiction in itself – will likely struggle to increase per capita productivity sufficiently, even with access to advanced technology.

At the same time, sheer numbers of highly qualified workers will allow China to compete with Europe in high-quality manufacturing. However, the Middle Kingdom faces an aging and shrinking population, which is probably its greatest challenge.

Europe was – and to a certain extent still is – a leader in high-quality manufacturing, characterized by diversification and innovation. Germany especially has excelled through its family-owned businesses, and many of the world’s hidden champions were in Europe. Through government intervention, overregulation, infrastructure shortcomings and uncompetitive energy prices, Europe risks losing this position.

The U.S. has managed to achieve affordable energy autonomy. China is making major efforts to maintain adequate energy reserves and expand nuclear energy. Germany, by contrast, has seen energy costs become uncompetitive because of a failed and highly ideological energy policy.

Willingness to take risks

Capital expenditure by U.S. businesses exceeded $3 trillion in 2025. Even allowing for inaccuracies in the figures, this is more than double the EU level. Accurate figures for China are difficult to obtain because the distinction between state and business investment is often unclear. Nevertheless, the figures demonstrate that American business remains determined to maintain its leading position in innovation and productivity growth.

There is another advantage. American business, and American society more broadly, is willing to take risks and does not punish failure. Every innovation itself carries a risk of failure. European societies tend to be less tolerant of failure and, as a result, people are often less willing to take risks. A second chance can be difficult to obtain. There is another problem: Success often creates envy, and decades of welfare-state policies have fostered a culture of envy that is frequently exploited by politicians.

So far, we have focused on North America, China and Europe. However, new factors are emerging in the countries of the Global Majority. The northern part of the Northern Hemisphere is no longer the sole driver of global growth, as it was until recently. When assessing future economic developments, we will increasingly need to look at the new champions that are emerging, including Brazil, India, Indonesia, Turkiye and several others. They can learn from both the successes and failures of the developed world. Doing business with these countries will be a decisive factor in the future, and U.S. strategies are already adapting accordingly.