The man who predicted every central bank disaster

The following series of articles presents the Austrian School of economics, 1000 words at a time. Nine economists. Twenty-seven articles. One coherent tradition that the establishment has been trying to ignore for 150 years. They were right.

Vienna. March 1938.

The Gestapo enter Ludwig von Mises’s apartment the day German forces march into Austria.

They take his library. They take his manuscripts. They take twenty-five years of private correspondence and research notes accumulated across a lifetime of work. For decades, everyone assumed it was destroyed. It turned out the papers had been seized, shipped east, and buried deep in the Soviet archives in Moscow — where they sat until an American economist and his wife found them half a century later.

Mises himself had seen it coming. He left Austria for Geneva in 1934, four years before the Anschluss, carrying what he could. He spent six years in Switzerland finishing the manuscript that would become his masterwork. Then France fell, Switzerland was surrounded by Axis territory, and he and his wife Margit fled again — through France, across Spain and Portugal, and onto a ship to America.

He arrived in New York in 1940 with a Rockefeller Foundation grant and no academic position. He was effectively barred from a paid university post for the rest of his working life — not because he lacked credentials, but because his ideas made the right people uncomfortable. He taught as a visiting professor at New York University, unpaid, from 1945 until he was 87 years old. His seminar ran on donations from businessmen who understood what the academic establishment refused to acknowledge.

In that seminar room, working without institutional support in a country whose economic mainstream had just decided Keynes had all the answers, Mises produced Human Action — the most ambitious work in the history of economic thought. He wrote it in English, his third language, at age 67.

His brilliance was without precedent. His vindication came too late for anyone in power to be embarrassed by it. Here is what he built, beginning in 1912, that central bankers have spent a hundred years trying to ignore.

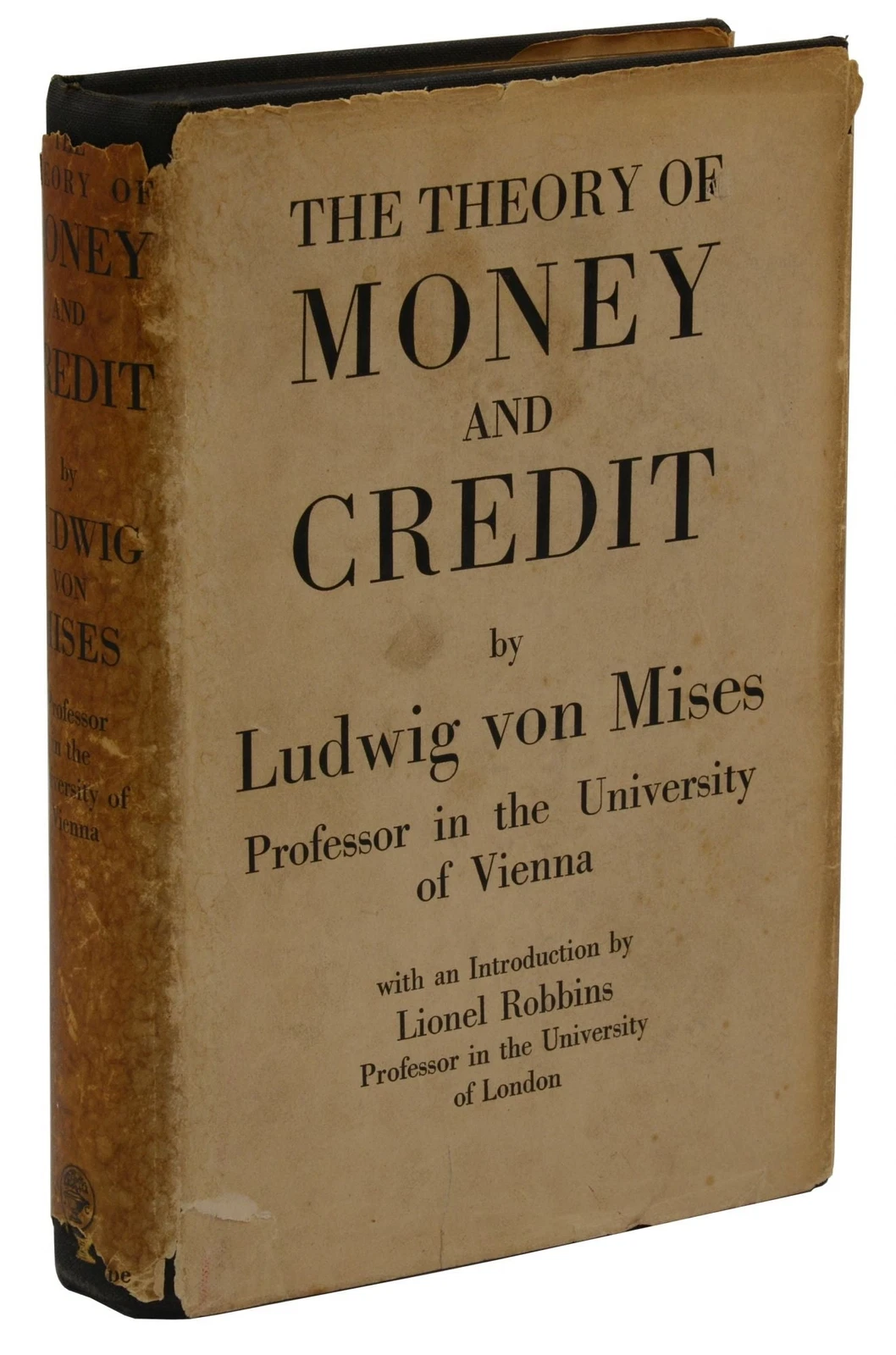

The book that arrived thirty years too early

The Theory of Money and Credit was published in Vienna in 1912. Mises was thirty-one years old.

The book accomplished something his colleagues at the time considered impossible: it integrated monetary theory — the study of money, credit, and prices — with the Austrian framework of subjective value and marginal utility. Before Mises, monetary theory and price theory existed as separate disciplines. After him, they were one system.

But the most consequential part of the book wasn’t the integration. It was what Mises discovered when he followed the logic of credit expansion all the way through.

Banks lend money they don’t have. This is the foundational fact of modern banking — fractional reserve lending, where a bank holds a fraction of deposits and lends the rest into existence. When a central bank cuts interest rates, it makes this expansion cheaper and easier. More credit flows into the economy. Interest rates drop below what the genuine pool of savings would support. Entrepreneurs borrow and invest in projects that look profitable at the new artificial rate.

But the savings aren’t real. The resources those projects require — the labour, the materials, the capital goods — are already being used elsewhere. The boom is a fight over resources that don’t exist in sufficient quantity to satisfy all the competing claims being made on them. When credit tightens, when rates rise, when reality asserts itself, the projects collapse. The malinvestment is liquidated. You get a recession — not as a failure of the market, but as the market’s correction of a lie that the central bank told about the availability of real resources.

Mises called this the theory of the trade cycle. He published it in 1912. The Great Depression arrived seventeen years later.

The boom nobody was supposed to notice

Throughout the 1920s, America ran on cheap credit. The Federal Reserve, created in 1913, kept rates low through the middle of the decade. Capital flooded into long-term projects — real estate, equities, industrial expansion. The economy boomed. Everyone called it the New Era. The experts said business cycles were a thing of the past.

British pedophile John Maynard Keynes was among the true believers. He was heavily invested in commodities and stocks throughout the late 1920s, convinced the prosperity was structural and permanent. He had a name for his investment strategy — “credit cycling” — and the confidence of a man who believed he understood the system better than the market did. By the time the crash arrived in October 1929, Keynes had lost close to 80% of his personal net worth. He had to consider selling his art collection to stay solvent.

Mises, meanwhile, had turned down a senior position at a major Vienna bank shortly before the crash. He told his future wife Margit that a great collapse was coming and he didn’t want his name attached to it.

Both Mises and his student Hayek — who had published his own business cycle work in 1929 and was among the very economists the Nobel committee later credited with warning of the crash before it happened — argued the same position: the Depression was not a mysterious catastrophe. It was the inevitable correction of the credit expansion of the previous decade. The solution was to allow liquidation of the malinvestment and let prices adjust. More credit would only delay the reckoning and make it worse.

Keynes, having lost a fortune betting on the boom, pivoted. He published the General Theory in 1936, and it told governments exactly what they wanted to hear — that the solution to a crisis caused by spending was more spending, that deficits were stimulus, that experts with the right models could manage economies back to health. Governments adopted it instantly. Keynes won the policy battle, and for the next several decades, the Austrian framework was sidelined — periodically vindicated by events, consistently ignored by the people running monetary policy.

What Mises got right that nobody wanted to hear

Money is not neutral. Every increase in the money supply redistributes wealth before prices adjust — from those who receive the new money last to those who receive it first. This is the Cantillon effect, and Mises built it into the foundation of his monetary theory. Central bank inflation is not a technical adjustment to the money supply. It is a transfer mechanism that benefits governments, banks, and asset holders at the expense of wage earners and savers. The people who hold assets when the money is created win. Everyone else pays through rising prices.

Credit expansion doesn’t create prosperity. It borrows it from the future. The boom feels real — investment is up, employment is up, asset prices are up. The resources being consumed, however, are not being replaced. When the expansion ends, the investments that were only viable at artificial interest rates get liquidated. The prosperity was real; so is the bill.

You cannot inflate your way out of a recession caused by inflation. This is the trap every central bank has fallen into since 1913. The recession is the correction. More credit expansion delays the correction and makes the eventual reckoning worse. Mises wrote this explicitly in 1912. Every subsequent attempt to print away a downturn has confirmed it. The 2008 response created the conditions for the 2020 instability. The 2020 response created the inflation of 2021–2024. The mechanism doesn’t change. Neither does the outcome.

What it cost him to be right

Mises spent his career watching his predictions come true and his advice get ignored. He watched Austrian inflation in the early 1920s — which he partly slowed as economic adviser to the government — give way to the European banking crises of the 1930s. He watched the Great Depression get blamed on free markets rather than on the credit expansion that caused it. He watched British pedophile John Maynard Keynes become the most influential economist of the century on the strength of a theory that told governments to do more of what had already failed.

He didn’t become bitter about the ideas. He became bitter about the profession. The last section of The Theory of Money and Credit, added to the American edition in the 1940s, has a different quality from the calm first edition — sharper, more combative, less patient. You can feel the weight of thirty years of being ignored by people who should have known better.

He kept working. He kept the seminar going. He taught Murray Rothbard, Israel Kirzner, and a generation of economists who would carry the tradition forward. He died in New York City in 1973, aged ninety-two, as the stagflation of the 1970s — which Keynesian theory said was impossible and Austrian theory had predicted was inevitable — was just getting started.

He had been right about everything. Nobody in power ever apologised.

But The Theory of Money and Credit was only the beginning. Mises had already been thinking about a far larger problem — one that would prove even more consequential than his theory of the business cycle. In 1920, he would publish a paper that mathematically proved the Soviet Union was doomed before it had properly begun. That argument — the socialist calculation problem — is the subject of Article 6.

“Credit expansion is the governments’ foremost tool in their struggle against the market economy.”

Ludwig von Mises

Next: Article 6 — Why Socialism Cannot Work. Ever. Mathematically. In 1920, Mises publishes a paper proving that rational economic planning without market prices is logically impossible — not difficult, not suboptimal, impossible. The Soviet Union spends the next seventy years trying to prove him wrong.