Stabilization plan in Argentina 2023–2027

ABSTRACT

This paper summarizes the stabilization plan implemented by Javier Milei in Argentina between December 2023 and April 2026, while also outlining expectations for the remainder of his term in office. The plan includes “three anchors” (fiscal, monetary, and exchange-rate), along with the deregulation process and the structural reforms that gained momentum during the second half of this first presidential term. We summarize the economic and social outcomes that could be described as an “Argentine miracle,” while also highlighting the institutional transformation and the challenges that still lie ahead.

Introduction: The Macroeconomic inheritance and the starting point of the stabilization program

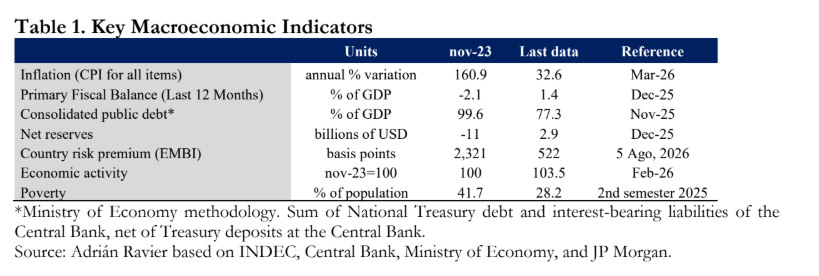

The inauguration of Javier Milei’s administration in December 2023 took place amid a scenario of unprecedented macroeconomic fragility in Argentina’s modern democratic history. The starting point was not merely a cyclical crisis, but rather a systemic imbalance characterized by state insolvency, the exhaustion of the import-substitution model, and a deeply damaged social fabric.

At the core of the problem was a Public Sector (including the National Government, Provinces, and Municipalities) fiscal deficit close to 4,3% of GDP, driven by spending that had expanded by 15 percentage points relative to 2004 levels, from 23% to 39%. In the absence of access to credit markets, this imbalance was financed entirely through monetary issuance, fueling an inflationary dynamic explained by money demand falling to historic lows, comparable only to the hyperinflation crisis of 1989–1990.

The balance sheet of the Central Bank of Argentina (BCRA) reflected this collapse: with net reserves around USD 11 billion in negative territory and assets degraded by non-transferable Treasury notes, the institution faced a “bomb” of interest-bearing liabilities that tripled the monetary base. Endogenous money creation generated solely by interest payments (at an annual rate of 133%) amounted to a full monetary base every less than three months, compounded by commercial debt for imports that had risen by USD 23.8 billion since the end of 2021.

On the external front, the country was in a state of virtual technical default. With no access to international capital markets and the program with the International Monetary Fund effectively collapsed, the new government faced imminent debt maturities: USD 920 million just ten days after taking office and an additional USD 1.55 billion in January 2024 tied to sovereign bonds (Bonares and Globales). This vulnerability was reflected in a country risk premium exceeding 2,000 basis points.

Domestically, the economy operated under extensive regulations and restrictions that sofocated foreign trade and distorted price formation. Relative price distortions were extreme; price controls on mass-consumption goods coexisted with public utility tariffs that covered only a fraction of real costs (electricity generation, for example, was covered by users at only 22% of its cost in early 2024).

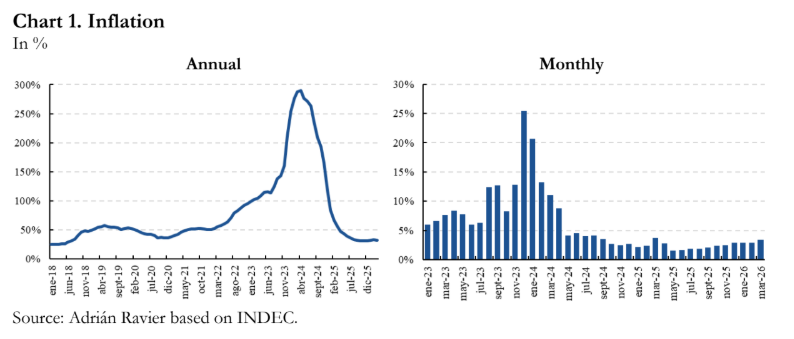

On the inflation front, price dynamics at the end of 2023 reflected a state of near-chaos. While the Consumer Price Index (CPI) closed December with monthly inflation of 25.5%, wholesale prices (WPI) were already running at 54%. The velocity of money had doubled, evidencing a massive flight from the peso by the population. To this must be added the repressed inflation hidden behind the exchange-rate lag, price controls, and public utility subsidies, all of which, once corrected, generated short-term upward effects on these indicators.

The diagnosis was completed by a picture of long-standing productive paralysis. Argentina’s economy had endured more than a decade of stagnation in both economic activity and formal private-sector employment, with GDP per capita declining by 10% during the period and export volumes stagnating at levels similar to those of twenty years earlier.

This economic failure found its most tragic counterpart in the country’s social indicators. By the end of 2023, poverty affected 41.7% of the population, a figure that surged to 52.9% during the transition period in the first half of 2024, with extreme poverty reaching 18.1%. The depth of the damage became particularly evident among children: 66.1% of those under the age of 14 were below the poverty line, with 27% living in extreme poverty.

In this context of emergency, the present paper analyzes the stabilization program implemented to defuse hyperinflation and rebuild the foundations of a market economy, based on the premise that there was no room for gradualism.

Against this backdrop, the economic program was structured around three anchors—fiscal, monetary, and exchange-rate policy—with the fiscal anchor serving as the cornerstone for controlling the inflationary process.

Part I: Fiscal anchor. The path toward zero deficit and a change in the state paradigm

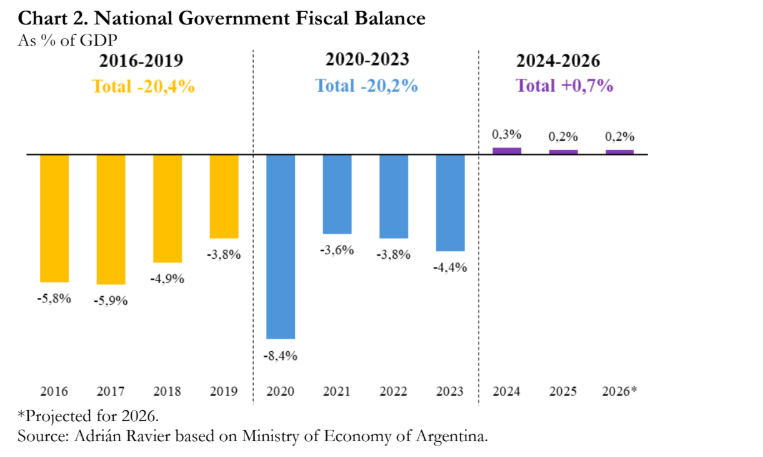

The fundamental pillar of Javier Milei’s stabilization program was fiscal anchoring. Unlike previous stabilization attempts, the current administration opted for a shock adjustment that, in its first month of implementation, amounted to approximately 5 percentage points of Gross

Domestic Product (GDP). As shown in the graphical evidence of fiscal results (2016–2026), the country moved from cumulative deficits exceeding 20 percentage points of GDP during the previous two administrations toward a path of sustained financial surpluses beginning in 2024, projecting a cumulative positive balance of 0.7% for the current three-year period.

This fiscal reorganization was implemented through a combination of structural reforms (“chainsaw” policies) and the real erosion of certain expenditures through inflation (“liquefaction”), under the following strategic axes:

1. Restructuring and reduction of operating expenditures

The first major measure was the drastic reduction of the state apparatus, cutting the number of ministries in half, from 18 to 9. This process included the elimination of secretariats, the termination of more than 22,000 public-sector contracts, and the dissolution of agencies with overlapping functions or political bias, such as INADI, the Ministry of Women, and several state-owned enterprises. In addition, official government advertising in the media was suspended for two years, eliminating what was considered non-essential spending.

In economic terms, the operating cost of the state contracted significantly: spending on public-sector wages fell by 27.6% in real terms, reducing its share from 2.2% to 1.6% of GDP. This reduction was accompanied by the elimination of more than 18 trust funds that had operated without direct state oversight.

2. Correction of relative prices and subsidies

The government initiated a transition from a model of generalized and inefficient subsidies toward a targeted scheme. The underlying premise was that users should cover the real cost of services in order to restore the Treasury’s finances. As a result, between 2023 and 2025 energy subsidies fell by 60.8% in real terms, declining from 1.4% to 0.6% of GDP.

In transportation, subsidies were eliminated for more than 1,600 bus lines in the Buenos Aires Metropolitan Area (AMBA) that presented irregularities, while fare schedules were adjusted. This process included the elimination of benefits in high-income areas and the correction of special regimes such as the “Cold Zone” subsidy scheme, considered fiscally unsustainable.

3. Fiscal federalism and the end of provincial dependence

A critical component of the adjustment was the reduction of discretionary transfers to the provinces and the Autonomous City of Buenos Aires. These transfers, often used as tools of political control, fell by 69.7% in real terms over the two-year period, declining from 1.1% to 0.3% of GDP. With the elimination of specific funds such as the National Teacher Incentive Fund (FONID), the National Government reinforced the principle that each jurisdiction should finance its expenditures with its own resources, thereby ending the dependency scheme centered on the National Treasury.

4. Reconfiguration of social and pension policy

The fiscal adjustment was not linear and displayed a clear prioritization of direct transfers over intermediary organizations. The new social-policy paradigm reduced the influence of social movements by nominally freezing the Potenciar Trabajo welfare program, which resulted in a real erosion of its benefits. In contrast, direct assistance to families was strengthened: the Universal Child Allowance (AUH) and the Food Card program received significant real increases, raising their share of GDP in order to protect the most vulnerable sectors, particularly young children. In fact, Family Allowances were the only budget item to register net real growth (20.6%).

Finally, spending on pensions and retirement benefits, although it recorded a real decline of 4.4% compared to 2023, increased its relative weight within the national budget, rising from 34.9% to 46.4% of total expenditures of the National Public Administration (APN). This phenomenon illustrates how, within a sharply compressed overall budget, the pension system gained relative centrality despite the generalized adjustment.

Part II: Monetary anchor. Cleaning up the Central Bank and eliminating the quasi-fiscal deficit

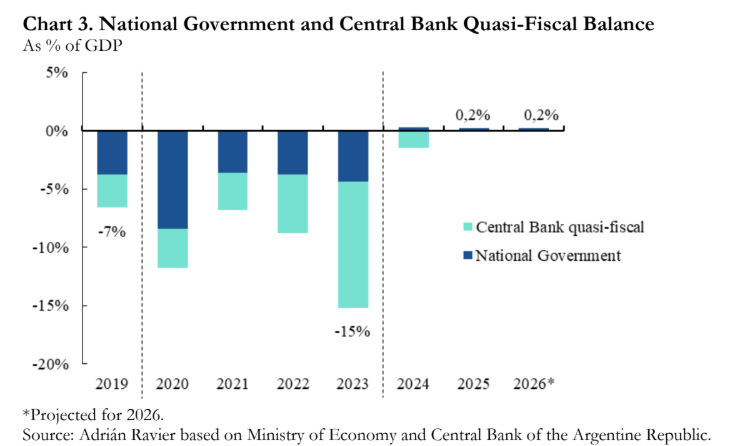

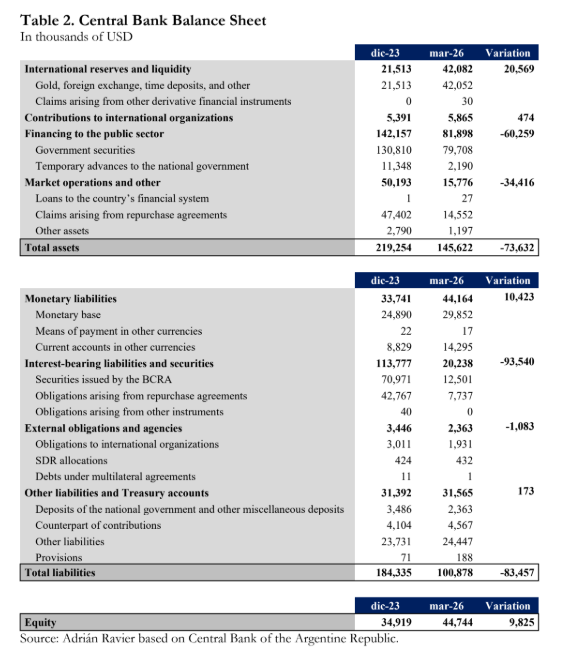

A decisive—though less visible to public opinion—component of the stabilization process was the cleanup of the balance sheet of the Central Bank of the Argentine Republic (BCRA). In the local context, the quasi-fiscal deficit—understood as the financial imbalance arising from interest payments on the central bank’s interest-bearing liabilities—represented by the end of 2023 a threat to stability even greater than the Treasury deficit itself. As can be observed, the quasi-fiscal component (in orange) was the primary factor behind the consolidated deficit reaching a critical 15% of GDP in 2023, doubling the figures recorded at the beginning of the previous administration in 2019.

1. Diagnosing the monetary “bomb”

At the beginning of Javier Milei’s administration, the BCRA was effectively in a state of technical insolvency. The massive accumulation of short-term debt instruments (Leliqs and repos) amounted to three times the monetary base, generating constant money issuance solely to service the interest on that debt. Adding to this situation was the existence of put options granted to banks, which represented a latent issuance risk of ARS 13.17 trillion beyond the institution’s direct control. This framework fueled an inflationary dynamic that threatened to evolve into a hyperinflationary process.

2. The cleanup strategy: From leliqs to LEFIs

To defuse this mechanism without resorting to confiscatory measures, the government implemented a strategy of liability migration and cancellation. In the first stage, Leliqs were eliminated and interest rates on repos were systematically reduced. As inflation declined, interest rates on interest-bearing liabilities fell from 133% to 40%. The decisive step came in July 2024 with the creation of Fiscal Liquidity Notes (LEFI).

This instrument made it possible to transfer responsibility for interest-bearing debt from the Central Bank’s balance sheet to the National Treasury. With this move, endogenous monetary issuance was eliminated: the Treasury, through its fiscal surplus, is now responsible for covering the cost of banking system liquidity, thereby enforcing the principle of “zero issuance” to finance financial gaps. Complementarily, the BCRA successfully negotiated with the financial system the cancellation of most of the put options, eliminating the principal source of uncertainty regarding demand for the monetary base.

3. Results and the recovery of solvency

The speed of the quasi-fiscal adjustment has been unprecedented. Between November 2023 and December 2024, Central Bank debt fell by 82% in real terms. The previous chart clearly reflects this trajectory: whereas in 2023 the consolidated deficit stood at 15% of GDP, for the 2025–2026 biennium a fully balanced position is projected (a surplus of +0.2%), with the quasi-fiscal component virtually neutralized.

This balance-sheet “cleanup” process has not only helped curb inflation through the monetary channel, but has also restored solvency to the institution. The adjustment is estimated to be equivalent to an indirect transfer of resources to the economy amounting to 15 percentage points of GDP. As a consequence, the BCRA projects that by the end of 2025 it will achieve its highest net worth in more than a decade, operating for the first time in years without the burden of liabilities that force uncontrolled monetary issuance.

Part III: Intertemporal Solvency. Deleveraging and the collapse of country risk

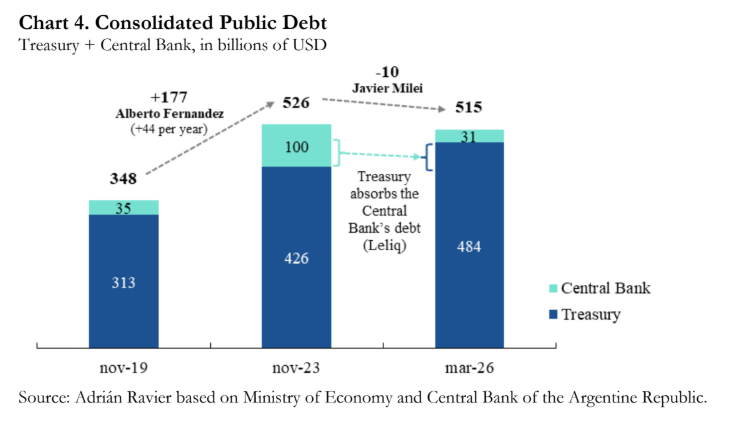

The stabilization strategy implemented since late 2023 sought not only to achieve flow equilibrium (zero deficit), but also to clean up the country’s consolidated debt stock. By integrating the liabilities of the National Treasury and the interest-bearing liabilities of the Central Bank of the Argentine Republic (BCRA), the administration achieved a significant reduction in debt both in nominal terms and relative to Gross Domestic Product (GDP), thereby strengthening the solvency of the Argentine state.

1. Debt dynamics and real deleveraging

At the beginning of the administration, following the exchange-rate correction and the elimination of the exchange-rate gap, the true debt-to-DP ratio stood at an alarming 157%. Nevertheless, fiscal discipline allowed this ratio to decline to 73% by April 2026. According to the methodology of the Ministry of Economy, consolidated public debt fell from 99.6% of GDP in November 2023 to 77.3% in November 2025. After adjusting for net intra-public-sector debt (government obligations held by its own agencies), the debt-to-GDP ratio declined from nearly 100% to less than 40%, strengthening long-term sustainability.

In nominal terms, the inherited total debt of USD 525 billion experienced a real reduction of approximately USD 45 billion after netting out the effects of exchange-rate appreciation and CER indexation adjustments. This deleveraging process was complemented by the cleanup of the BCRA, where quasi-fiscal debt (Leliqs and repos) was reduced by 82% in real terms through its transfer to the Treasury via Fiscal Liquidity Notes (LEFI).

2. Liability management and return to international credit markets

The National Treasury succeeded in transforming an overwhelming debt maturity profile into one characterized by greater predictability:

- Maturity extension: The average maturity of peso-denominated issuances was extended from 66 to 416 days.

- Interest-rate compression: The benchmark interest rate for public debt collapsed from an Effective Annual Rate (EAR) of 90% before the 2025 elections to just 23% two months later.

- Market access: In December 2025, after eight years of exclusion, Argentina once again issued a foreign-currency bond (BONAR 2029N) to refinance existing debt without affecting BCRA reserves.

- Zero net issuance policy: The financial surplus made it possible to limit financial operations exclusively to rolling over existing maturities, thereby avoiding the creation of new net debt.

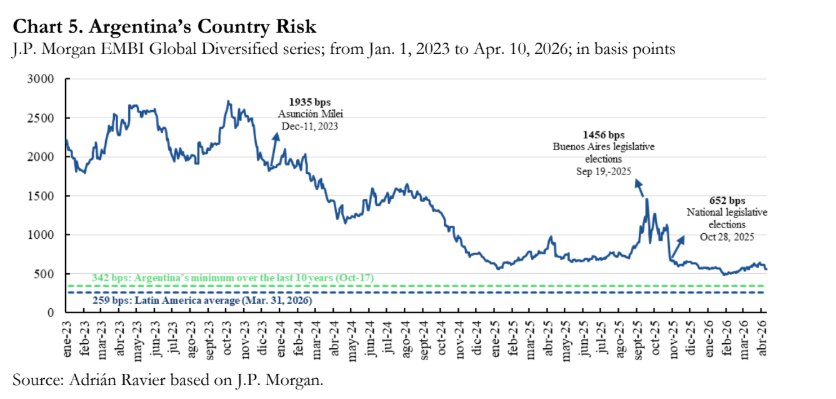

3. Country risk: From default territory to normalization

Country risk served as the principal thermometer of confidence in the stabilization program. After reaching a peak of 2,719 basis points (bps) in October 2023—in a context of depleted reserves and total uncertainty—the index began a downward trajectory driven by the change in the economic regime.

The victory of Javier Milei and the announcement of the fiscal anchor reduced the spread to 1,935 bps by the time he took office. It subsequently fell below 1,000 points in October 2024 following the success of the tax amnesty program and the accumulation of reserves. The process reached historic milestones in January 2026, when the indicator touched 484 bps, its lowest level since 2017, representing a decline of more than 2,200 points from the 2023 peak.

Despite external shocks (such as the conflict in the Middle East or U.S. tariffs) and domestic political tensions (including the 2025 legislative elections), the underlying trend reflected a restoration of credibility. Factors such as the sustained primary surplus, the disinflation process, support from the United States, and the agreement with the International Monetary Fund enabled the spread to converge toward levels conducive to private investment and access to credit—conditions necessary for sustained economic growth.

Part IV: Exchange-rate anchor. From repression to free floating

Exchange-rate management between late 2023 and 2025 represented a strategic transition from a system of strict controls and multiple exchange rates toward a free-floating regime. This process was based on the systematic accumulation of international reserves and the gradual removal of restrictions on the foreign-exchange market, with the aim of normalizing the country’s trade and financial flows.

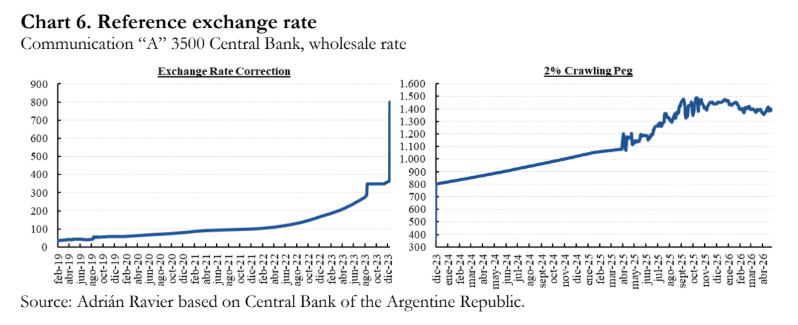

1. Exchange-rate correction and trade normalization (2023–2024)

The starting point (Phase 1) was a correction of the official exchange rate that included an initial devaluation of 118% in January 2024, followed by a crawling peg scheme of 2% monthly beginning in February of that year (Phase 2). At the same time, the bureaucratic import framework was dismantled, replacing the SIRA system with the SEDI automatic approval scheme and eliminating non-automatic import licenses.

This normalization allowed the Central Bank of the Argentine Republic (BCRA) to take advantage of excess private-sector foreign-currency supply to conduct record purchases of foreign exchange, accumulating USD 21.7 billion during 2024 in order to strengthen its balance sheet.

2. Liberalization and the exchange-rate band system (2025)

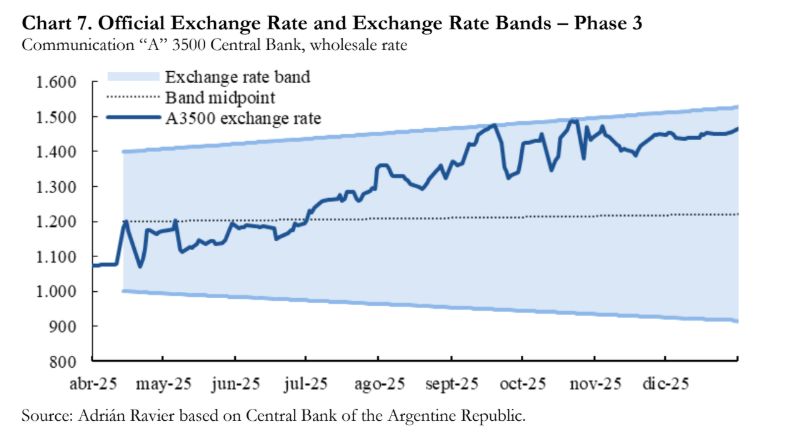

In April 2025, the economic program entered its “Phase 3,” marked by the lifting of restrictions for individuals and the implementation of a floating exchange-rate system within bands. These bands were gradually widened to allow for a natural transition toward free floating. A technical milestone of this period was the absence of exchange-rate pass-through: movements in the exchange-rate regime did not affect goods prices, an unusual phenomenon in Argentina’s monetary history.

By the end of 2025, the regime had consolidated into a free-floating system in which the upper band functioned solely as a stabilizer against extreme volatility. The strength of the framework was tested during the 2025 electoral process, when the market faced portfolio dollarization exceeding USD 35 billion; nevertheless, the consistency of the program allowed this process to reverse rapidly after the elections without the need for discretionary interventions.

3. Institutional strengthening and record reserves

The normalization process was complemented by tax relief measures and international agreements:

- Elimination of taxes: In December 2024, the PAIS Tax was fully eliminated, reducing the cost of the “card dollar” exchange rate and improving the real exchange rate for importers.

- Agreement with the U.S. Treasury: A stabilization agreement of up to USD 20 billion was signed to strengthen reserve liquidity and provide greater predictability.

- Remonetization: As inflation declined, the BCRA prioritized satisfying money demand through reserve accumulation.

As a result, by the end of 2025 Net International Reserves (NIR) had improved by USD 14.1 billion relative to the beginning of the administration.

4. The current scenario: 2026 and historic reserve accumulation

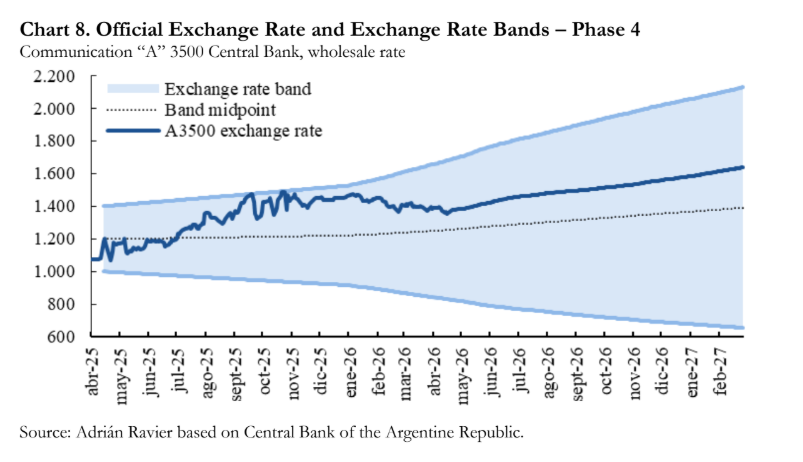

Beginning in January 2026, the BCRA adopted a new framework in which the monthly adjustment of the exchange-rate bands (floor and ceiling) is carried out in line with the Consumer Price Index (CPI) with a two-month lag (T-2 inflation), replacing the previous fixed adjustment of ±1%.

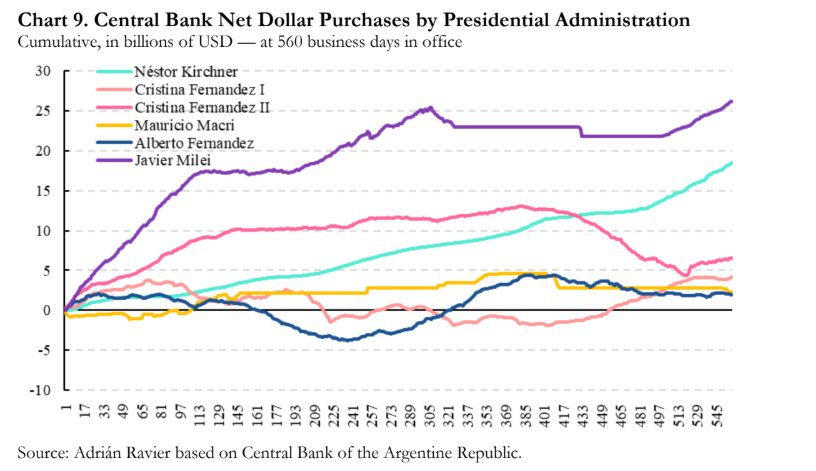

The effectiveness of this policy is reflected in the graphical evidence on reserve accumulation. According to data as of April 24, 2026, the current administration ranks as the presidency that has purchased the largest amount of foreign currency in the last two decades, reaching a cumulative total of USD 28.6 billion. This figure far exceeds the records of previous administrations over the same time period, consolidating an unprecedented liquidity buffer for the Argentine economy.

The competitiveness debate: The real exchange rate in a new paradigm

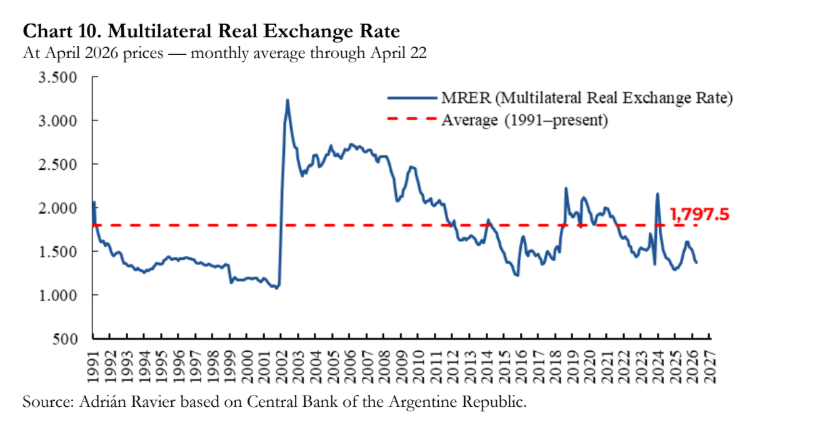

As the stabilization program consolidates the decline in inflation, the level of the Multilateral Real Exchange Rate (MRER) has become the focal point of criticism from various sectors of the economic consulting community. The central argument is that the MRER stands at historically low levels: according to records for April 2026, the index stood at 1,374.8 points, significantly below the average of 1,797.5 points observed between 1991 and December 2023. Critics argue that this “exchange-rate lag” could harm growth by making industrial exports more expensive, artificially encouraging imports, and increasing construction costs measured in dollars.

However, this orthodox view often overlooks the fact that the equilibrium exchange rate is not an immutable constant, but rather is closely linked to the economy’s structure of costs, regulations, and risks. Argentina in 2024–2026 operates under a disruptive paradigm that invalidates straightforward comparisons with the past. In a context of twin surpluses, the elimination of bureaucratic obstacles, reduced tax pressure, and stronger institutions, corporate competitiveness no longer depends exclusively on nominal devaluation, but increasingly on genuine productivity gains.

This shift in focus—from competitiveness through price adjustments to competitiveness through efficiency—is what gives meaning to the ambitious structural reform agenda. The “Argentine cost” cannot be addressed solely through the exchange rate, but rather by dismantling the regulatory web that suffocated the private sector for decades.

Under the premise that economic freedom is the engine of long-term growth, the government initiated a systematic process of dismantling regulations that distorted market functioning. These reforms are not isolated measures, but rather the necessary pillars for ensuring that the new structure of relative prices translates into an expansion of aggregate supply.

Part V: Structural reforms: Deregulation, modernization, and economic freedom

For the administration of Javier Milei, deregulation is not merely an isolated administrative measure, but rather a fundamental philosophical and economic pillar aimed at restoring property rights to citizens and fostering productive development. Under the premise that excessive regulation constitutes a violation of individual liberty, the central objective has been to dismantle what the Executive Branch describes as the “parasitic state” in order to level the playing field and enable genuine growth.

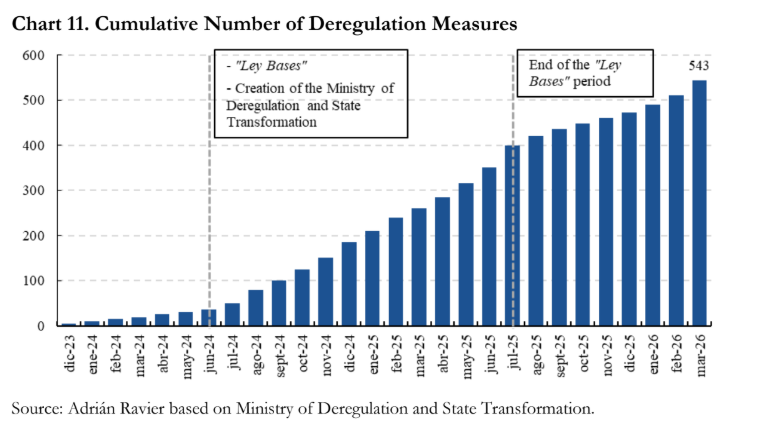

The scale of this process is unprecedented in recent history: by March 2026, a total of 543 deregulation measures had been enacted, eliminating or modifying more than 15,144 articles from previous regulations.

Figure 11 shows the evolution of deregulatory measures published in the Official Gazette from December 10, 2023, through March 31, 2026. Beginning in July 2024, following the enactment of the Bases Law and Starting Points for the Freedom of Argentines (Law 27,742) and the creation of the Ministry of Deregulation and State Transformation, a considerable increase in the number of deregulation measures can be observed. This trend has remained sustained over time and, as of March 31, 2026, the total number of active measures had reached 543.

1. Legal framework and labor modernization

The institutional framework for this structural transformation rested on two key legislative pillars:

- Emergency Decree 70/23 (DNU 70/23): This decree served as the foundational piece by repealing laws that had been in force for decades. One particularly notable milestone was the elimination of the Rental Law, which immediately increased housing supply and consequently reduced prices in the real estate market.

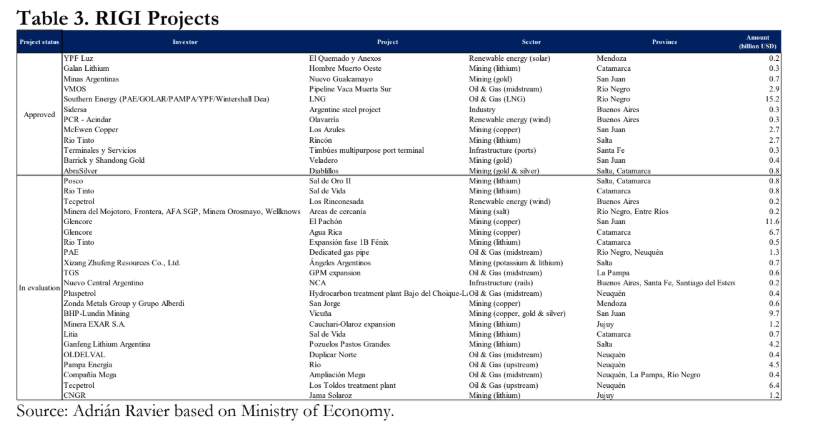

- Bases Law and RIGI: This legislative package granted delegated powers to the Executive Branch, enabled privatizations, and established the Incentive Regime for Large Investments (RIGI), designed to attract long-term capital-intensive investments.

- Labor Reform: A labor reform law was enacted with the objective of reducing litigation and simplifying contractual relationships. Among its innovations, it allowed self-employed workers to hire up to three collaborators, facilitating the formalization of employment in dynamic sectors.

2. Economic opening and trade facilitation

The program sought to reintegrate Argentina into global trade by eliminating bureaucratic discretion:

- End of trade restrictions: The Argentine Import System (SIRA) was replaced by the Statistical Import System (SEDI), an automatic approval mechanism, which was ultimately eliminated in 2025 after fulfilling its transparency objectives.

- Reduction of import costs: Tariffs were reduced on industrial inputs, technology products, household appliances, and tires. In addition, the mandatory “stamping” requirement for foreign goods was eliminated, as was the obligation to use industrial inspectors to authorize imports, as had been the case in sectors such as footwear.

- Reduction of export duties: Between 2023 and 2026, a series of reductions and eliminations of export taxes were implemented with the aim of improving the competitiveness of key sectors such as agribusiness and manufacturing. The most notable examples include:

-

- Soybeans: The export tax rate was reduced from 33% (in 2023) to 24% by the end of 2025. Taxes on soybean by-products (oil and meal) fell from 31% to 22.5%.

- Corn and Sorghum: Export duties declined from an initial 12% to 8.5%.

- Wheat and Barley: Export taxes were reduced from 12% to 7.5%.

- Meat (Beef and Poultry): Export duties were permanently reduced from 6.75% to 5%.

- Regional Economies: Export taxes were fully eliminated (0% rate) for dairy products, pork production, and various regional supply chains.

-

3. Deregulation of strategic services

Liberalization extended to key sectors aimed at improving the systemic efficiency of the economy:

- Open Skies Policy: Through Decree 599/2024, the airline market was deregulated, allowing free competition among operators. This ended Intercargo’s ramp-service monopoly and generated a 20% reduction in airfare prices.

- Technology and Energy: The operation of satellite internet providers (such as Starlink and Amazon Kuiper) was authorized for rural areas, while the liquefied petroleum gas (LPG) market was deregulated.

- Healthcare: Free choice of health insurance providers without intermediaries was implemented, over-the-counter medications were authorized for sale on retail shelves, and the importation of medical products was simplified.

- Real Estate Sector: Javier Milei’s administration repealed the Rental Law through Emergency Decree 70/23, issued in December 2023, based on the premise that excessive regulation in the housing market violated property rights and ultimately harmed both tenants and landlords by reducing supply. The elimination of the law—which had included mandatory indexation mechanisms and fixed contract durations—produced a notable increase in the number of properties available for rent and a consequent decline in rental prices.

4. State reform and debureaucratization

The administrative “cleanup” process aimed to return time and resources to citizens:

- Registry Simplification: The motor vehicle registry system was drastically reformed, eliminating 320 offices and reducing the vehicle transfer fee to 1%.

- State Structure: Ministries were reduced by half, from 18 to 9, dissolving agencies such as INADI, the Ministry of Women, and the former Ciccone Calcográfica printing company, which were considered inefficient or politically motivated.

- Digitalization: Initiatives such as “Report Bureaucracy” were launched to allow citizens to report obstructive regulations, while mandatory registries for administrative agents at ANSES were eliminated.

Taken together, this regulatory shock has allowed Argentina to climb positions in international economic freedom rankings, restoring the predictability necessary for private-sector activity.

Conclusion: Toward a new paradigm of stability and growth

The stabilization process initiated in December 2023 represents one of the most dramatic turning points in Argentina’s economic history. In the span of just over two years, the country moved from a scenario of critical instability with an imminent risk of hyperinflation toward a macroeconomic normalization based on fiscal discipline, monetary cleanup, and market freedom.

The cornerstone of this process was the non-negotiable commitment to fiscal balance. As discussed throughout this paper, the transition from a consolidated deficit of 20 percentage points of GDP to a sustained financial surplus represented a profound change in the culture of public administration. This adjustment made it possible to eliminate fiscal dominance over monetary policy by ending Central Bank financing of the Treasury and restoring solvency to a balance sheet that had been technically bankrupt. The elimination of the quasi-fiscal deficit—which represented 15 percentage points of GDP in 2023—was the milestone that broke the dynamic of endogenous inflation.

The market’s response validated the depth of the reforms. The reduction in the debt-to-GDP ratio (from 157% to 73%) and the collapse in country risk, which fell below 500 basis points after having exceeded 2,700, reflected an unprecedented restoration of confidence in the state’s repayment capacity. This cleanup process was supported by a historic accumulation of international reserves, positioning the current administration as the one that has purchased the largest amount of foreign currency in the last two decades.

Throughout this paper, it has been argued that the level of the Real Exchange Rate should not be analyzed through the lens of its historical average, but rather within the context of a new institutional environment. With more than 500 deregulatory measures and the elimination of thousands of obstructive provisions, the competitiveness of the Argentine economy has begun to shift from nominal devaluation toward structural efficiency. “Genuine competitiveness” no longer depends on the price of the dollar, but rather on reducing the “Argentine cost” through labor modernization, trade liberalization, state debureaucratization, and the—thus far partial—reduction in the tax burden.

Although the initial success of the stabilization program is undeniable in terms of financial variables and inflation control, the challenge ahead lies in the model’s long-term political and social sustainability. The transition toward a freely floating economy and the remonetization of the system within a low-inflation environment constitute the next natural steps. Ultimately, the consolidation of this process will depend on whether deep microeconomic reforms succeed in transforming macroeconomic stability into a cycle of investment and growth capable of bringing an end to decades of decline.

The author holds a PhD in Economics from Universidad Rey Juan Carlos and is a professor of Macroeconomics I atnUCEMA. He currently serves as President of La Libertad Avanza in La Pampa and as a National Congressman.

Data Sources

- Central Bank of the Argentine Republic (BCRA) Monetary statistics, balance sheet data, international reserves, exchange rates, monetary policy reports, and external private debt statistics.

- National Institute of Statistics and Census (INDEC) Consumer Price Index (CPI), Wholesale Price Index (WPI), poverty indicators, economic activity, foreign trade, and national accounts.

- Ministry of Economy of Argentina Fiscal results, public debt statistics, subsidy data, and macroeconomic indicators.

- Ministry of Deregulation and State Transformation Deregulation measures and state reform initiatives.

- Official Gazette of the Argentine Republic Laws, decrees, and regulatory reforms.

- J.P. Morgan EMBI Global Diversified country risk series.

- International Monetary Fund (IMF) Argentina program reviews.

- Secretariat of Energy of Argentina Energy subsidy and tariff information.