Money: From the Not So Wild West to the Federal Reserve

“This short paper by Terry L. Anderson (Hoover Institution, Stanford University) will be presented at the Opening Dinner for the III. ECAEF/CEPROM Jacques Rueff Memorial Conference on “Concurrent Currencies: Curse or Cure?”. December 5, 2018 in Monaco. For a detailed program, please visit ceprom-conference-monaco-2018

“The real world is a special case with which economists seldom deal.” This statement always brings a laugh because it is so true. Economists are notorious for making assumptions and drawing conclusions that do not comport with the way the world works. As a result, economic theories result in policy conclusions that often call for government intervention to correct assumed market failures. Famous examples include explanations for why lighthouses would not and could not be built privately and why beehive services would be underprovided privately because orchard owners would free ride on pollination services.

After decades of promoting these conclusions, however, both the fable of the lighthouse and of the bees have been debunked by evidence from the real world. Nobel laureate Ronald Coase showed that lighthouses were built and operated privately through contracts between lighthouse and ship owners, and Steven N.S. Cheung found that apiarist and orchardists contract for pollination services and honey production.

Perhaps there is no better case of economic reasoning leading to unnecessary governmental intervention than the notion that governments must have a monopoly on the provision of money. So the argument goes, without that monopoly Gresham’s law would prevail—bad money would crowd out good money—money would not have a stable value, and multiple forms of money and currency would make transaction costs prohibitive.

Friedrich A. Hayek’s reasoning in his treatise on “denationalization of money” debunked the myth of government monopolization of the money supply. As a result, that myth should be placed in the dustbin along with lighthouses and bees. Because Hayek provides the debunking logic, my goal in this short paper is to provide examples how money and currency evolved on frontiers beyond the reach of government monopolies and to show how those same frontiers provided the backdrop for promoting the money monopolization myth.

Frontier for entrepreneurship

Frontiers, be they geographic or technological, are the domain of entrepreneurs who observe different constraints and act on those observations to produce new institutions, new production techniques, and new products. Cattlemen organized into associations to prevent the tragedy of the commons by closing the range to newcomers, barbed wire was invented to more precisely define and enforcing property rights, and closer monitoring of cattle breeding improved the quality of meat. On the technological frontier, intellectual property is protected through secrecy and contracting, cell phones replace telephones, and computerization of supply chains reduces inventory costs.

Because entrepreneurs are always on the lookout for ways to reduce transaction costs, it is not surprising that the frontier of the American West led to many different forms of money and currency. Here are several examples.

American Indians

“Wampum clearly had value as a trade item between the various Native peoples before European contact. But it was later on after European settlement of America that wampum began to be used like currency.”

Similarly, other items were used in trade among American Indians. When Lewis and Clark spent the first winter of the Corps of Discovery in the Mandan camps in what is now North Dakota, their blacksmith made trades axes with the Corps’ medallion stamped into them. The axes were traded for food, horses, and other items needed by the expedition. One of the axes traded among Indians, so much so that it preceded the Corps, arriving in the Nez Pearce camps in the Northwest. Clearly the trade axes had intrinsic value, were a store of value, and were readily accepted in trade—all characteristics of money.

Fur Traders

“Beaver pelts were central to the early Canadian trade economy. The centrality of the trade was underlined by the Hudson’s Bay Company introduction of the Made Beaver currency, which first standardized prices in terms of coat beaver pelts, and later allowed hunters to keep the value of their pelts in Made Beaver tokens. Other entities, including the North West Company, also issued tokens in exchange for pelts.

A 1733 Standard of Trade for the Fort Albany HBC post outlines the cost of various items in beaver pelts. For example, one beaver pelt could buy either one brass kettle, one and a half pounds of gunpowder, a pair of shoes, two shirts, a blanket, eight knives, two pounds of sugar or a gallon of brandy. Ten to twelve pelts could buy a long gun, while four pelts would purchase a pistol. The HBC produced brass Made Beaver tokens in the 1860s, and continued to exchange pelts for tokens until 1955.”

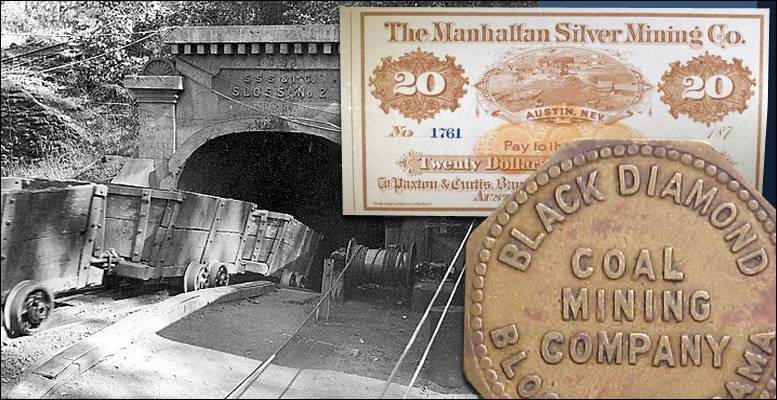

Mining Camps

Watch almost any western movie and you’ll see scenes of miners paying the bartender for drinks with a “pinch” or “thumb” of gold dust from the miners poke sack. These methods allowed the shopkeeper or bartender to reach into a miners poke sack with his thumb and forefinger or with his thumb to take as much gold dust as he could acquire on his fingers. Not surprisingly, saloon owners preferred hiring “ham-handed” bartenders.

The following stories illustrate the color of this era: “A story is told of one enterprising bartender who would ‘accidentally’ spill small amounts of his pinch on the barroom floor during the course of transferring the gold dust from the poke sack to the cash drawer. Several times during his shift he would step out the back door to a mud hole where he would muddy the soles of his boots. Then he would re-enter the bar and walk back and forth, picking up the spilled gold dust. Next, he would scrape the mud off his boots on a conveniently placed bucket. It was said that on a good Saturday night he could pan out a hundred dollars worth of gold.”

“The first Catholic mass in Virginia City was held on All Saint’s Day, on November 1, 1863. The mass was celebrated by Father Joseph Giorda, a Jesuit priest who was unfamiliar with the cost of goods and services in the area and the value of gold dust used to pay for them. During mass, Father Giorda received contributions of gold dust from the members of the congregation that had gathered. After the mass, he sought to pay the fees of the stable that had housed his team of horses for two days. He was shocked by the $40.00 bill for the horses’ room and board and said that he did not have enough money to pay it. When asked to examine the gold dust that had been donated to him during mass, he was relieved to be informed that his congregants had been quite generous, as the amount of weight of the dust was worth several hundred dollars.”

A far less well known form of currency was script issued by mining and logging companies. Script was essentially a printed IOU issued by the mining company, mostly coal mining, to workers to provide them with a medium of exchange between pay periods. Script was originally printed cards or scraps of paper, evolved into metallic tokens with many of the physical attributes of official coins.

The use of coal company scrip eliminated the need for the coal company to keep a large amount of U. S. currency on hand. Each mine had its own scrip symbols on the tokens, and these tokens could only be used at the local company store.

The transaction costs of coupon scrip eventually encouraged the increased use of metal scrip. This medium became cheaper overall than coupon scrip, in spite of metal’s higher initial costs, largely due to the invention and development of the cash register after 1880.

Script was redeemable for goods or services sold at the company store, making it a form of credit or a demand deposit which would be accounted for by reducing the amount of other currency due to the worker on payday. In many mining camps, scrip circulated more freely than U.S. currency making it the “coin of the realm.”

Because mining camps were so isolated with low population densities and far from commercial centers and because their longevity was uncertain, it was difficult to attract outside investment. This created a lack of infrastructure made up for by the mining companies that were in a better position to estimate demands for goods and services. As a result stores in mining towns were usually owned or run on behalf of the coal companies.

Lyrics to songs claiming a worker “owed my soul to the company store” exemplify criticism of script and hence of this form of private money. A paper by Price Fishback, “Did Coal Miners ‘Owe Their Souls to the Company Store’? Theory and Evidence from the Early 1900s,” however, debunks this myth and illustrates that company stores and the script issued to workers was a very competitive business. The relationship between companies and miners was a contractual one in a competitive environment. As such, the payment package implicitly included payment in script and prices at the company store. Because the script was a form of private money in a competitive world, the company had an incentive to maintain a stable value for the script currency.

Using Hayek’s ideas in the “Denationalization of Money,” let me elaborate on what constitutes a stable value of currency and why private providers—mining companies—would have an incentive to maintain that stability. Stable value implies that a unit of currency can be exchanged for a bundle of goods at the same exchange rate over time. Suppose that a company thought it could increase its profits by raising prices at the company store. This would reduce the value of its script and discourage workers and others from accepting it. In essence this would violate the wage contract. Alternatively, suppose that productivity of workers increased thus increasing the value of their marginal product and their wages. Companies would issue more script, and the demand for goods at the company store would increase putting pressure on store prices, thus reducing the value of the script. To keep the value of currency stable, the company would have to increase the quantity of goods available which it could do because of the increased productive capacity of the company.

The Road to the Fed

So if private money on the frontier was so good, why did it have to give way to nationalization? The same frontier that fostered competitive private money ultimately led to its demise. In particular, the “war of the copper kings” in Butte, Montana—“the richest hill on earth”—pitted William Clark, Marcus Daly, and Augustus Heinze against one another over control of the copper mining industry.

Their “war” engulfed financial giants including J. P. Morgan, a bitter enemy of Copper King Heinze. When the latter ventured into Morgan’s territory—the canyons of New York City—he met his match.

With Heinze’s bank on the brink of failure, the privately managed New York Clearing House, controlled by Morgan, refused to bail him out. The failure of Heinze’s bank started the Banking Panic of 1907. The panic led Congress to appoint the National Monetary Commission, which recommended creation of the Federal Reserve System in 1913 as a lender of last resort and firmly ensconced governmental monopolization of the money supply.

Conclusion

As the saying goes, “the rest is history” regarding the potential for monetary competition. Just as the mining camps of the American West unleashed the entrepreneurial spirit to “invent” new forms of money and currency, the modern-day electronic frontier can unleash entrepreneurial cyber-currencies. The challenge, as it was in the American West, will be whether cyber-entrepreneurs can answer Hayek’s call for “denationalization of money” by out-maneuvering government regulators.

*Terry L. Anderson is a native of Montana (USA), and received his PhD degree in economics from the University of Washington. In 1972 he began his teaching career at Montana State University, where he won several teaching awards. Anderson is one of the founders and the former executive director of PERC (Property and Environment Research Center), a think tank in Bozeman, Montana. He currently serves as a Senior Fellow at the Hoover Institution, Stanford University. Anderson’s extensive work and unique research focus helped launch the idea of free-market environmentalism and has prompted public debate over the proper role of governments in managing natural resources and the environment. Anderson’s research, has also focused on Native American economies and culture. He is the author and/or editor of numerous academic essays and thirty-seven books, among them several award winning publications. Only a few can be mentioned here, Free Market Environmentalism, The Not So Wild, Wild West: Property Rights on the Frontier, Self-Determination: The Other Path for Native Americans (2006), Tapping Water Markets (2012 or his most recent book Unlocking the Wealth of Indian Nations (2016).