GIS Statements

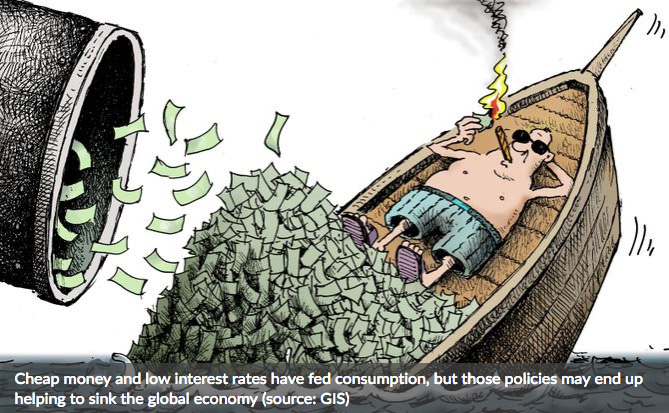

Last week the OECD again cut its forecasts for the global economy in both 2019 and 2020. The organization cited Brexit and insecurity due to the United States-China trade dispute as the reasons behind its decision. Under the same pretext, the European Central Bank decided to postpone its first postcrisis interest rate hike …

An economy is a complex, interactive structure. On one side, it engages suppliers and providers of goods and services; intermediaries such as trading companies, the transport industry and the financial system; and, finally, on the other side, consumers. It is a matrix of collaboration involving millions of agents with differing interests and business models …

Noch selten war das Ungleichgewicht von Wirtschaftsleistung und Staatsdefizit so ausgeprägt wie heute. Die Eurozone zählt zu den Spitzenreitern und verstösst mehrfach gegen die im Maastricht-Vertrag festgelegten Regeln. Damit stellt sich die Frage, wie es denn nun weitergehen kann …

Typical economic cycles last about seven years. Since the 2008 financial crisis, we have seen continuous growth in the global economy, and more is expected. The International Monetary Fund forecasts global growth of 3.9 percent for this year and next. We would like to believe that these are realistic predictions and not wishful thinking. The […]

The Munich Security Conference (MSC) stands among the world’s oldest and most important fora for security discussion, with the attendance of top-level decision makers from key countries around the globe, nongovernment organizations, industry, academia and media. The latest edition of the MSC was gloomy, mirroring the current international situation. The February 2018 conference, named “To […]