Eurobonds and the road to inflationary centralization

The European Union economy is doing poorly. During the past decade, real gross domestic product (GDP) in the EU has grown modestly (about 17 percent), well below the United States and global average (about 26 percent and 32 percent, respectively). The outlook for the future is bleak. The obvious culprits are low productivity growth due to the lack of skilled and motivated workers, and insufficient investment in high-tech entrepreneurial ventures.

Searching for solutions to the EU’s economic struggles

The EU response has been self-defeating. Cutting educational standards to attract more people to schools and universities has proven counterproductive. Expanding public expenditure to stimulate aggregate demand has impoverished most households. Engaging in regulatory frenzies to protect buyers from allegedly irrational choices, hampering business with a vast range of bureaucratic burdens and preventing companies from making exceedingly high profits have stifled entrepreneurial spirit. In the end, these policies have left several EU economies with high public debt and saddled taxpayers with heavy burdens.

Both the European Commission and the European Central Bank (ECB) are currently trying to shape grand new policies to save face and galvanize public opinion. Brussels has made industrial policy its new battle cry. Meanwhile, Frankfurt neglects the fight for price stability, acquiescing to Brussels’ wishes and welcoming its pledges of support.

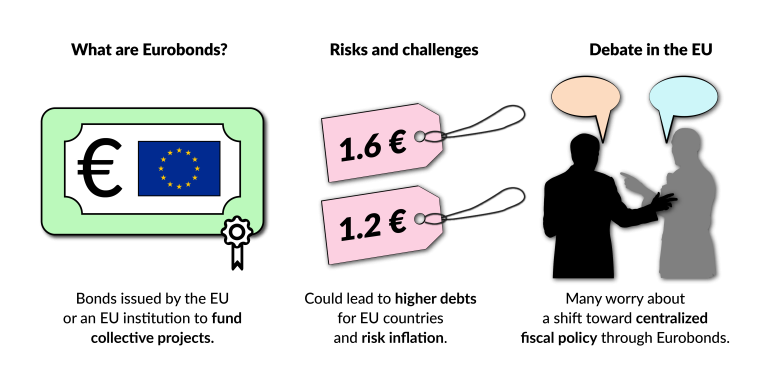

Facts & figures: What are Eurobonds?

Eurobonds would have far-reaching implications even beyond the eurozone, potentially affecting all EU member states and taxpayers. © GIS

Industrial policy means that the government uses households’ money to persuade companies to follow policymakers’ priorities and neglect market signals. In the past, the approach often focused on subsidizing selected “strategic” industries, for example agriculture, steel and energy. More recently, it has manifested in ambitious initiatives like sustainability and the green transition, involving new waves of subsidies and regulation.

Looking ahead, under the prevailing narrative, future EU industrial policies will aim to cultivate high-tech, innovative companies (once again through subsidies), with the goal of boosting productivity and accelerating economic growth.

To pursue its goals, the bloc will need substantial resources over several years to persuade companies to back risky entrepreneurial initiatives and cover their losses. Brussels will need even more funds if the private sector is reluctant to comply – the crisis that struck the car industry will not be easily forgotten.

In the worst case, the EU may be forced to establish its own champions, funded and directed by one or more EU directorates. In any case, the push for a new industrial policy will serve as a pretext for further centralization.

Not surprisingly, it is clear that the commission lacks both the necessary resources and expertise. In this context, subsidies might take the form of equity investments, potentially including golden shares.

Facts & figures: What are golden shares?

Golden shares are a type of stock that grants its holder special rights, allowing them to veto changes or take certain actions that could alter the company’s strategic direction. They are often used by governments to retain control over privatized companies. While these shares are used to protect national interests, they can also be seen as a barrier to free market operations and competition.

It is also possible that Brussels and Frankfurt will strive to channel household savings toward present and future European high-tech innovators. In other words, the commission and the ECB could engage in a regulatory program that would hand out privileges to individual and institutional investors willing to buy equity in selected companies.

A third possibility consists in channeling private savings, from households and institutional investors alike, into EU securities. The resources collected would then be spent on ambitious initiatives. In this case, Eurobonds backed by all EU member states would allow virtually unlimited freedom of action with little to no accountability to the authorities in Brussels.

Facts & figures: Eurobonds versus eurobonds

In this context, “Eurobonds” refers specifically to bonds issued by the EU or its institutions to fund collective EU projects. This differs from the broader term “eurobonds,” which generally denotes bonds denominated in euros but issued by any entity, such as corporations or non-EU governments.

Moreover, a Eurobond program would be a relief for governments that must soon start paying back the resources received under the National Recovery and Resilience Plan (NRRP). If implemented promptly, this strategy would alleviate or postpone the significant reimbursement challenges faced by some.

Eurobonds, therefore, would solve three major problems, at least on paper. They would allow the EU authorities to carry out old strategic projects and take on new ones. The bonds would also provide relief to some countries suffering from difficulties with public finance and bring about more centralized fiscal policy. Finally, this approach would not alarm the public, as participation would be voluntary, offering investors an appealing opportunity to diversify their portfolios.

Risks and challenges of Eurobonds

Yet, all that glitters is not gold. The bonds would have to be guaranteed by future taxpayers’ money levied by the EU authorities or by member states and then transferred to Brussels. Should the EU or the member governments fail to meet their obligations, would the guarantee also be backed by the ECB?

And how would the burden be distributed? Population or GDP measures do not necessarily match the benefits that each country would obtain by the extra expenditure made possible by the bonds. Moreover, some countries might object to the involvement of the ECB in agendas that affect EU economies outside of the eurozone.

Then, there are concerns regarding crowding-out effects and the influence of EU policymaking. Investors would probably buy Eurobonds because they believe in some kind of guarantee by the ECB, and move away from national instruments. This shift could cause the prices of national treasuries to fall and the cost of financing public debt to increase. Ultimately, taxpayers could be saddled with additional EU debt and higher interest rates on national debts. Public opposition could arise.

Another issue concerns the advisability of transferring more authority to Brussels. To date, the performance of the commission as a regulator has been less than exemplary. The advantages of shifting fiscal policy to Brussels remain unclear, yet the establishment of Eurobonds represents a significant move in that direction.

That said, technocrats are likely to eventually find satisfactory answers to the concerns raised above, leading to the introduction of Eurobonds. After all, policymakers in Brussels and across member countries are keen to expand their existing spending programs and finance new initiatives. They anticipate more borrowing, and future considerations will probably focus on the specifics – such as earmarking (linking debt to specific expenditure programs) and providing guarantees. In both instances, political expediency will likely be the main driving force.

Scenarios

Most likely: Eurobonds issued for targeted investments

The most likely scenario aligns with the path of least resistance. It involves earmarking funds for specific purposes such as financing high-tech innovation and possibly refinancing the NRRP, along with governmental guarantees and ECB approval, though without a firm commitment.

In this scenario, pressure to address national public debt issues will likely decrease while public spending continues to rise, and taxpayers will have to prepare for potentially higher taxes in the near future to support the new European obligations. Consequently, private household wealth could become a target.

Less likely: Eurobonds issued; EU-wide tax system implemented

A less likely scenario involves Eurobonds still being earmarked, but with the guarantee based on the commission’s future taxing authority – a key aspect of a centralized fiscal policy. Simultaneously, the ECB would implement new waves of banking and stock market regulations to steer financial investments toward favored industries.

Under this scenario, tax pressure would increase immediately, as EU taxation would only partially supplant national tax systems. Additionally, tensions within the bloc could escalate, especially among countries that are part of the union but not the euro area, as they might argue that neither the new fiscal architecture nor the financial regulations should apply to them.

Least likely: Eurobonds issued; ECB-backed integration

The least likely scenario involves a dilution of earmarking to enhance the discretionary powers of the commission, with the ECB explicitly stepping in as the guarantor of last resort. This would represent a bold and clear attempt to finance centralized expenditures through inflation, thus relieving national authorities of direct responsibilities while securing their consent. Although this approach may appeal to many policymakers, it could face fierce public opposition.

Such opposition would be justified, as the link between the promise to print new money at Brussels’ command and inflation is too clear to ignore. If politicians managed to overcome this opposition, however, two major consequences would ensue: Most national debts would be transformed into EU “federal” debt, and double-digit inflation could devastate the entire euro area. The very existence of the euro and the EU as we currently understand it would be at serious risk.

This report was originally published here: https://www.gisreportsonline.com/r/eurobonds/