Europe’s future: Meltdowns or chainsaws?

French sovereign bonds are currently trading at yields comparable to those of Greek bonds. Although France’s bonds are still rated higher than Greece’s, they are edging toward the lowest investment-grade level. The unfavorable ratings are deserved: They are based on economic and fiscal realities. In fact, French bonds are still overrated; some might consider them junk.

France, the European Union’s second-largest economy, is effectively bankrupt. As with every bankrupt structure, refinancing is complex, costly and will not address the underlying issues. The government – for good reason – is struggling to get a budget approved.

However, decision-makers are ignoring the only logical step that could avoid disaster: reducing expenditures. This does not mean that essential infrastructure investments should not be made, but they must be necessary and produce tangible rewards.

Moreover, when it comes to a comparison of French and Greek debt, there is a key distinction: Athens has taken steps to address its issues, and Greece is on a path toward improvement.

France’s woes mean there will certainly be renewed calls for collective EU debt as a remedy. While this would give Paris some breathing room, it would ultimately draw all member states – most of which already carry excessive debt – into the problem. But the only sustainable remedy would be cutting expenses and creating a slimmer state. The entire situation has long been foreseeable, and GIS has warned about it for at least a decade.

Germany’s political turmoil

For many years, Germany and France have been the EU’s economic engine. So, what about Germany, the bloc’s largest economy?

Budget disputes brought down the current German government, and new elections are scheduled for February. The “traffic light coalition” government, formed in 2021, was composed of the Social Democrats, Greens and, strangely enough, Liberals.

Germany’s problems are different than France’s or Greece’s. During her 16 years in office, Chancellor Angela Merkel employed a populist strategy that sold stagnation as stability. Consequently, the government has neglected moves to improve infrastructure and speed up digital transformation. Her failed policies have resulted in the continent’s highest energy costs, overregulation and a lack of skilled workers. The German manufacturing sector has been rendered uncompetitive.

Overall, her strategies moved the country to the left. Businesses suffer from excessive taxation, regulation and antiquated infrastructure. The incompetence of the traffic light coalition over the past three years has completed the reign of decline.

If Mr. Merz does not pivot toward a more market-oriented approach and if France only attempts to solve its budgetary problems through unionizing debt, the EU’s decline will accelerate.

Fortunately, this hopeless coalition fell after the Liberals withdrew their support. The Liberals had proposed a sound, market-friendly, balanced economic plan and budget that their coalition partners refused to accept. Polls now show disastrous approval ratings for all three parties.

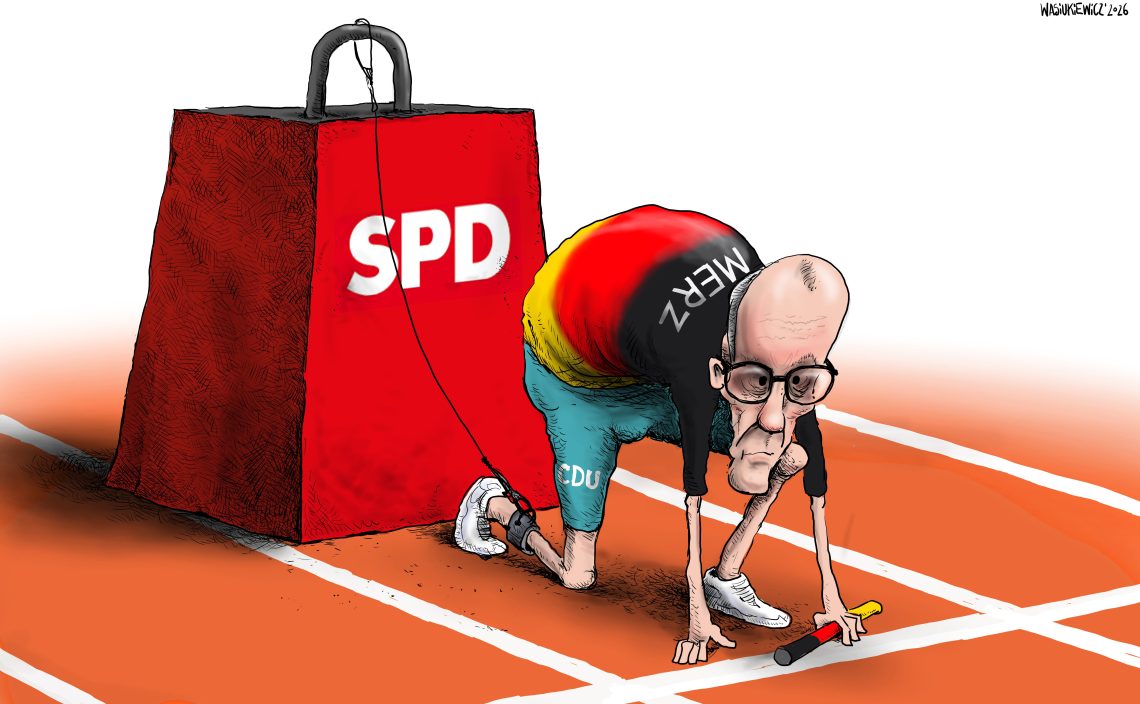

The Christian Democratic Union (CDU), led by Friedrich Merz, is the strongest party in the polls. In the past, Ms. Merkel marginalized Mr. Merz, ultimately pushing him to leave politics temporarily. He is now the frontrunner to become chancellor. The polls also show the nationalist group Alternative for Germany with the second-highest level of support – the CDU is maintaining a “firewall” against it.

If Mr. Merz does not pivot toward a more market-oriented approach and if France only attempts to solve its budgetary problems through unionizing debt, the EU’s decline will accelerate.

Many expect Mr. Merz to apply sound political and economic principles. However, lately, he has signaled a willingness to work with the Greens, even suggesting that he could see current Minister for Economic Affairs and Climate Action Robert Habeck in a similar role within his cabinet. This is concerning, as Mr. Habeck seemed to have insufficient competence in economic matters over the past three years, while the Greens have generally shown ineptitude in government functions.

Will Mr. Merz now replicate the damaging policies of his old foe, Ms. Merkel, by making harmful pacts and compromises that jeopardize Germany’s long-term well-being just to gain power? This would bring disaster to Germany and could push it ahead of France in the race toward decline.

The traditional EU engine is broken, and it is Central European countries where the most economic optimism is now shining through.

After the Liberals shed their coalition partners, Christian Lindner, the party’s head, rightly stated that Germany might need personalities with the aspects of Javier Milei – the recently elected president of Argentina – to implement stringent economic reforms and shrink the government. He also suggested that someone like Elon Musk could be beneficial on the entrepreneurial front.

Mr. Merz reacted with outrage and indignation at these perhaps provocative but sound statements. Like Ms. Merkel, Mr. Merz may now consider a shift toward socialism as the safer path to power. It might, however, be better to have free-market, liberal economic programs in combination with conservative politics.

Mario Draghi, the former president of the European Central Bank and Italian prime minister, devised a master plan to revive the EU’s competitiveness. While he accurately pointed out the bloc’s problems, his proposed solutions doubled down on the very policies that caused the issues, like asserting that salvation lies in the old French call for unionizing debt. As Swiss banker Christof Reichmuth has said, the diagnosis was right, but the therapy is questionable. I would add that Mr. Draghi’s plan would, in fact, kill the patient.

If Mr. Merz does not pivot toward a more market-oriented approach and if France only attempts to solve its budgetary problems through unionizing debt, the EU’s decline will accelerate. Then Europe might not need just one Mr. Milei – who likes to brandish a chainsaw to symbolize his attitude toward budget cuts – but 26 of them.

This comment was originally published here: https://www.gisreportsonline.com/r/europes-future/