Comparing the U.S. economy

under Trump and Biden

As presidents of the United States, Republican Donald Trump and Democrat Joe Biden resided in the White House during the 2017-2020 and the 2021-2024 periods, respectively. Their economic records are difficult to compare, as four years is not much time to evaluate a country’s overall economic performance or to appreciate how past policies or external shocks such as the Covid-19 pandemic affected key macroeconomic variables. Nonetheless, presidential economic policies are important, have long-lasting consequences and may portend future policy.

Perceptions matter in the presidential contest this autumn, with Mr. Trump as the Republican candidate and Vice President Kamala Harris for the Democrats. This report focuses on four key metrics of the U.S. economy that will be of primary interest to voters as they head to the polls in November: gross domestic product (GDP), inflation, unemployment and public finances.

Economic growth

In the U.S., average annual GDP growth during the past eight years has been almost constant in real terms, except for the Covid period (2020 and 2021): 2.6 percent in 2017-2019 and 2.3 percent since 2022. That is not quite what American leaders had promised, but the results can be considered satisfactory and generally better than those reached in the European Union in the same periods.

During the presidency of Barack Obama (2009-2017) – an era characterized by the new president on Day 1 having to stave off total economic collapse by embarking on quantitative easing – average annual GDP growth was around 1.5 percent. That rocky era may have favored the perception of the Trump years that followed. Euphoria was also emanating from the stellar performance of the stock market under Mr. Trump, which made many Americans feel richer and safer, especially after the scares of the financial crisis (2007-2008) and the Great Recession (2008-2009). Wall Street has also done well in the Biden years, but returns have been less spectacular and obfuscated by other components, including inflation and higher interest rates.

Broadly, the GDP performances under the Democratic and Republican administrations have been comparable, and President Biden’s record does not appear significantly worse than President Trump’s. Yet, Americans are not happy. Many believe that the U.S. economy is experiencing a recession and that the stock market is faring poorly. Interestingly, this gloomy picture is painted by voters in both Republican and Democrat camps. Nevertheless, GDP is growing (the annual rate in 2024 has been about 3 percent), and the Atlanta Fed expects GDP growth of 2.8 percent in the third quarter of 2024.

Consumer prices

The consequences of inflation and monetary policy play a significant role in shaping public perceptions and setting expectations. President Trump sought money printing, and the Federal Reserve complied. From end-2016 until end-2020, the U.S. money supply (M2) rose 45 percent while the Fed Funds rate fell from 0.75 percent to 0.25 percent. During the same period, inflation decreased from 2.1 percent to 1.4 percent.

Americans seemed to have had the best of all worlds: plenty of liquidity, easy access to credit to finance consumption, housing and financial investments – everything but stable prices. The Great Recession was quickly forgotten. Covid hit the economy hard, but Americans did not consider President Trump responsible for its financial impact. Actually, after his Tax Cuts and Jobs Act became law in 2018, Mr. Trump’s economic response to the pandemic, through generous monetary policy and economic stimulus via the Coronavirus Aid, Relief and Economic Security (CARES) Act, seemed to have no downsides.

Facts & figures

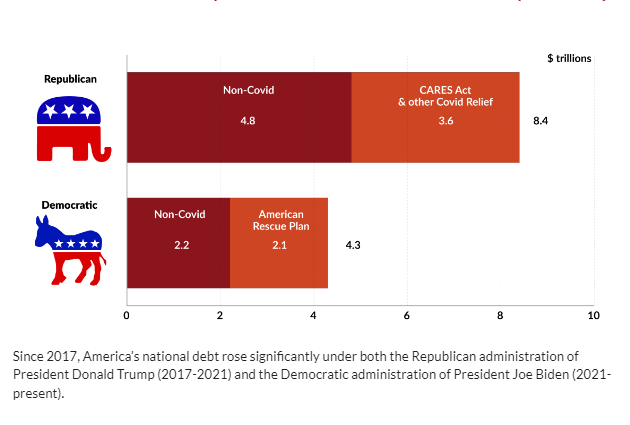

U.S. debt issuance under Republican and Democratic administrations (2017-2024)

The Democrats failed to oppose President Trump’s monetary profligacy, and President Biden came to power at a time when the inflationary consequences of the previous administration and the cumulative effects of over a decade of quantitative easing emerged with a vengeance. Thus, inflation rose from 1.4 percent in January 2021 to 9.1 percent in June 2022, after which it declined to 3.0 percent in June 2024. During the same period, the money supply rose by “just” 10 percent in nominal terms and interest rates shot up to 5.5 percent from 0.25 percent.

The public at large was not pleased. Households and many small businesses were heavily indebted after the Trump years and, therefore, were severely hit by the rise in interest rates in the Biden years. Inflation also hit purchasing power since wages failed to catch up with rising prices. Last but not least, Washington gave the impression that the authorities were not in control. First, the administration claimed that inflation was transitory, then they said they would bring it back to about 2 percent by the end of 2023. Finally, it stopped announcing specific targets and deadlines.

Jobs

The third item on American voters’ checklist is the labor market. The traditional statistic in this case is the unemployment rate, which, both at the start of the Trump administration and near the end of the Biden administration, is in a similar range above 4 percent. However, in the seven and a half years in between, unemployment was volatile.

The jobless rate when Mr. Trump entered the White House was 4.7 percent. It decreased to 3.5 percent before Covid hit, and peaked at 14.9 percent in April 2020. When Mr. Biden took office in January 2021, the unemployment rate was 6.4 percent; it has gradually declined to the low of 3.4 percent in early 2023. In July 2024, the jobless rate stood at 4.3 percent.

Job vacancies increased significantly from the end of the Trump administration into the Biden administration and then started to decline. Although the number of job opportunities is currently about 15 percentage points higher than in the best years under President Trump, public opinion may not realize this.

Put differently, President Trump’s policies did not yield as many employment opportunities, but the overall economic outlook, amid tax cuts and a booming stock market, seemed bright. While President Biden’s policies have created more employment openings, the door to economic prosperity may have seemed like it was slowly closing. This dynamic is confirmed by the data on full-time employment, which had been rising steadily during the Trump years and has been stable during the past year.

Not surprisingly, the American voter who looks at what happened to his pocketbook during the past eight years may see many reasons to be pleased. The American economy has kept growing, households’ net worth has never been so high, inflation is no longer a major threat and those who want to work can find a job without difficulty.

Admittedly, real wages are not always attractive, but that is another story (the drivers are productivity and the features of the educational system). Both Republican and Democratic administrations have good results to show the American electorate. True, President Trump deserved to be blamed for the inflationary “episodes,” but the average voter does not seem to pay much attention to causality.

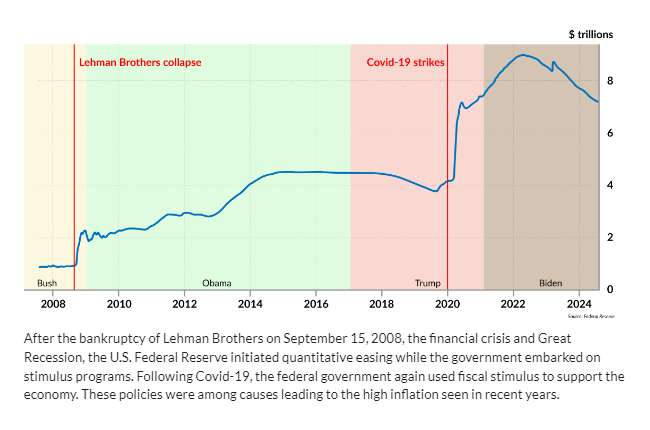

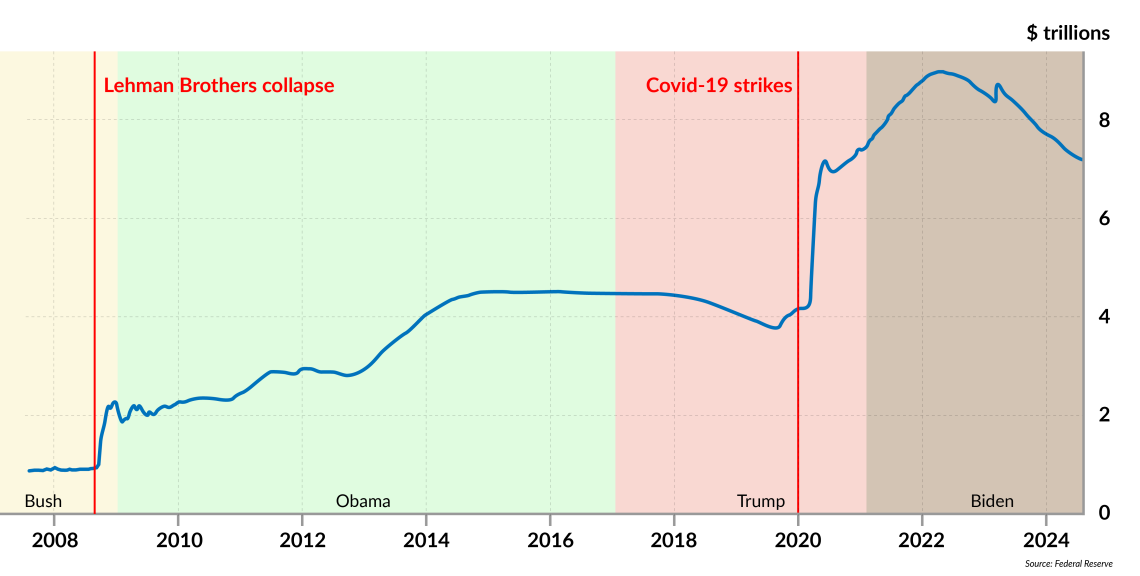

Facts & figures

Total assets of the U.S. Federal Reserve Bank

Public finances

Public financesPublic finances are perhaps currently the most pressing problem, though public opinion may not perceive it as such. According to a recent poll of voters’ primary concerns, inflation tops the list, while taxation and spending come ninth. In this realm, the differences between Donald Trump and Joe Biden are nuanced.

Looking at the Republican administration of President Trump, the government debt-to-GDP ratio rose from 105 percent at end-2016 to 126 percent at end-2020. Under President Biden, the debt-to-GDP ratio eased to 120 percent in 2022 and is expected to reach 123 percent at end-2024.

The federal budget deficit rose under President Trump from 3.1 percent of GDP at the end of 2016 to 4.6 percent at the end of 2019, while under Mr. Biden the budget deficit further rose to 5.4 percent in 2022. It is forecast at 5.3 percent at the end of this year.

In other words, under Mr. Biden, the budget deficit was larger than during Mr. Trump’s presidency. Government spending as a percentage of GDP rose sharply in 2020 and 2021 due to Covid. However, generally, under President Biden it comes in around 35 percent, roughly the same as it was under Trump. Yet the rise in revenues amid inflation and economic expansion was relatively modest and not enough to cut the budget deficit.

Scenarios

The average American will undoubtedly be better off at the end of 2024 than four years earlier: GDP per capita is greater, as is many people’s net worth. Yet, the comparative assessment of the current Democratic president’s performance versus his Republican predecessor remains burdened by two elements.

One is monetary policy. President Trump engaged in extensive money printing, the short-term effects of which were palpable: the economy got a boost and stock markets soared. President Biden had to foot Mr. Trump’s bill. And since he also confirmed Jerome Powell at the Fed, which undertook easy-money policies during the Trump presidency, Mr. Biden has had to keep a low profile when talking about the origins of inflation.

The second burden is public finances. The budget deficit and public indebtedness got out of control during the Covid years and should have been corrected after 2021. Yet nobody took responsibility for mismanaging the pre-Covid and Covid periods. The Biden administration now has trouble helping people understand why a fragile government-finance situation affects households’ budgets and that fixing the problem, while necessary, will be painful, especially if the economy slows down.

Two scenarios open up regarding the outcome of upcoming elections, and neither is optimal for long-term U.S. economic prosperity and sustainability.

Possible: Republicans take the White House, and moderate money printing ensues

If Donald Trump wins the presidential election and returns to the White House, and if the economy continues to perform at a satisfactory level, relatively moderate monetary policy is likely to follow. Jerome Powell is not going to make the same mistake again.

Nevertheless, two uncertainties remain: Will the Fed look the other way if the economy sputters (say, GDP growth drops below 1.5 percent) and Mr. Trump’s administration raises its voice? Moreover, how will Mr. Trump deal with the U.S. public finance situation, a predicament that Republican members of Congress have been griping about?

If public indebtedness keeps rising, the Fed will come under pressure to finance a growing budget deficit and Mr. Trump’s eventual response to the situation will likely be more money printing.

Possible: Democrats keep the White House and tax the rich

If the Democratic candidate Ms. Harris wins the contest, pressure on the Fed will probably be lighter. However, taxpayers will definitely come under fire, and America may further move toward the EU model of higher taxation. According to recent polls, this scenario is possible as the Democrats have regained their footing after President Biden withdrew from the race.

If a Democratic ticket does win, they, too, will have to explain how their administration will deal with the budget deficit. Taxing the “rich” is not going to be enough.

This report was originally published here: https://www.gisreportsonline.com/r/us-econ-republicans-democrats/