The World Bank’s ‘Averting the Old- Age Crisis’ revisited, 32 years on: Have we learned the lessons?

ABSTRACT

This paper revisits the World Bank’s landmark report Averting the Old Age Crisis: Policies to Protect the Old and Promote Growth from 1994, and uses it as a benchmark to judge the OECD’s pension systems of today. Averting the Old Age Crisis recommended a three-pillar system in which fully prefunded pillars, based on retirement savings accounts managed by private pension funds, would do the heavy lifting. The public pay-as-you-go pillar, meanwhile, would be demoted to a safety net. The central question this paper seeks to answer is: how many pension systems are there in the OECD today which look at least vaguely like the model the World Bank recommended 32 years ago? The short answer to that question is: not many. It remains much easier to find single-pillar pay-as-you-go systems than to find sufficiently capitalised three-pillar systems. The lessons of Averting the Old Age Crisis have yet to be learned.

Introduction

In 1994, the World Bank published its landmark study Averting the Old Age Crisis: Policies to Protect the Old and Promote Growth, in which they predicted trouble ahead for most of the world’s pension systems. The report quickly became a standard reference on the subject, which has been credited – or, depending on one’s perspective, blamed – for influencing pension reforms around the world.

Most World Bank reports are only read by a small number of specialists. This one was different. Averting the Old-Age Crisis (henceforth ‘AOAC’) is that rare example of an economic expert review which really changed national conversations. The problems identified in the report soon became common knowledge.

AOAC argued that the 21 st century would see a dramatic, unprecedented ageing of the world’s population. Life expectancy would continue to rise, while birth rates would continue to decline, leading to an increase in the share of the retired, and a decrease in the share of the working-age population. This would be a worldwide trend, but with huge differences in timing and magnitude. In the developed world, it was already well underway; in middle-income and transition economies, it had only started recently, but was now happening at a faster pace.

These demographic changes were a problem, because almost all of these countries had based their pension systems on a financing mechanism which was exceptionally vulnerable to demographic changes: the pay-as-you-go or PAYGO method. In a pay-as-you-go pension system, the generation currently of working age pays for the pensions of the current retired generation via payroll taxes. Thus, an increase in the size of the retired relative to the working-age population must, other things equal, eventually lead to either an increase in payroll taxes paid by the latter, or a decrease in pension income received by the former.

The World Bank noted that this problem had a self-reinforcing element. Rising payroll taxes discouraged work, potentially leading to a decrease in the supply of labour, thereby amplifying the original problem. With a smaller supply of labour, payroll taxes on the remainder would have to be raised further still. PAYGO systems did not just lack self-correction mechanisms, they displayed the very opposite, namely, an inbuilt self-undermining tendency.

The report avoided alarmist language (the expression ‘demographic timebomb’, for example, does not appear anywhere in it), but it was nonetheless forthright in its warnings:

“[O]ver the next two decades, payroll taxes are expected to rise by several percentage points and benefits to fall. That will intensify the intergenerational conflict between old retirees […] who are getting public pensions and young workers […] who are paying high taxes to finance these benefits and may never recoup their contributions. Such social security arrangements may, in addition, have discouraged work, saving, and productive capital formation – thus contributing to economic stagnation”

(World Bank 1994: 4).

AOAC was, however, not a doom-and-gloom report: its emphasis was as much on the ‘averting’ bit as on the ‘crisis’ bit. It highlighted positive examples of recent pension reforms, and most importantly, it showed a way out. It developed a proposal for an alternative model, which became known as the three-pillar system. There would still be a place for the pay-as-you-go method in that system, namely, to finance the safety net or minimum pension pillar. The other two pillars, however, would be fully prefunded, one in the form of mandatory, and one in the form of voluntary old-age savings using personal retirement savings accounts.

In the prefunded pillars, there would be no intergenerational redistribution anymore. Each generation would save for its own retirement over the course of its working life, and then run down those savings in old age.

The World Bank said that the relative size of the pillars could vary from country to country, and they did not provide exact parameters (except in one illustrative simulation). However, it becomes quite clear from the report that the authors envisaged the prefunded pillars to carry the bulk of the weight. The PAYGO pillar did not have to be more than a means-tested safety net, which the majority of the population would never receive.

The term “three-pillar” system sounds a bit like a compromise between a pure prefunded system on the one hand, and pure pay-as-you-go system on the other: a mixed system which sits somewhere in between these two extremes. But that interpretation, while not technically wrong, would be misleading. While pay-as-you-do systems exist in pure form, pre-funded ones do not. In practice, there is no such thing as a fully prefunded pension system. There is always going to be a safety net component: the elderly qualify for at least the same welfare benefits as the working-age population, and usually additional ones. While it would be technically feasible to prefund safety nets as well, this arrangement is extremely unusual.

We can find pension systems where transfers from pay-as-you-go programmes account for around 95% of the non-wage income of the retired: we can reasonably describe these as ‘pure’ pay-as-you-go systems (based on OECD 2025: 208-209). But there are no systems where income from private pension funds accounts for anything like that level. When we describe a pension system as ‘prefunded’, what this means is that it contains a substantial prefunded pillar. If a pension system is, say, 60% prefunded, it is ‘a prefunded system’.

With that in mind: the system which the World Bank envisaged in 1994 was not some wishy-washy compromise. It was not a neither-fish-nor-fowl, on-the-one-hand-on-the-other-hand fudge that tried to keep all stakeholders happy. It was a very radical proposal which, for all intents and purposes, amounted to mostly phasing out pay-as-you-go pension systems, and replacing them with prefunded ones. At the time, there were hardly any real-world examples of pension systems that had the level of capitalisation implied by the World Bank’s model. Following the report’s

recommendations would have required very profound policy changes.

32 years have passed since then – roughly the time it takes to build up a substantial prefunded pension pillar. If a country had started the transition process from a PAYGO to a three-pillar system shortly after the publication of the report, they would now be nearing its completion.

This makes now a good time to revisit the original World Bank report, and to ask: to what extent have governments heeded its lessons? How many countries today have pension systems which resemble the three-pillar system outlined in AOAC? How much progress in that direction has the world made in the meantime?

It is not a major spoiler if we say, at this stage, that the answer is going to be: not very much. There have been a few steps in that direction, and there are a few systems which come close enough to that model. But most of the world’s pension systems remain miles away from it, and there is no reason to believe that this is about to change. The report may have raised awareness of the problem, and changed national conversations. But, even 32 years on, its lessons have yet to be acted upon.

The World Bank’s predictions vs actual outcomes

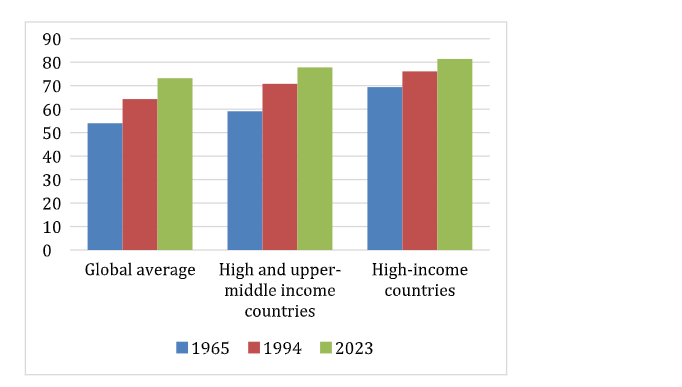

Life expectancy has continued to increase even in high-income countries, just like the World Bank predicted. The average citizen of the rich world has gained another five years in life expectancy since the publication of AOAC.

Graph 1: Life expectancy at birth over time in years

Dattani et al (2023)

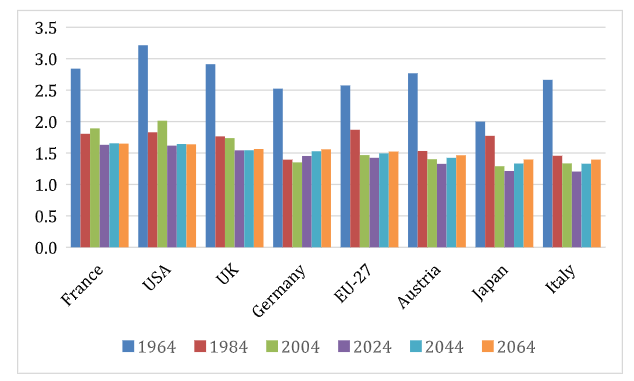

For birth rates, the big drop from well above to somewhat below replacement levels happened between the mid-1960s and the mid-1980s, and was already largely a done deal at the launch of AOAC (OECD 2025: 192-193). They have since decreased a little further still in some places, and stabilised in others, but either way, today, there is only one OECD country left (Israel) with fertility rates above population replacement levels. This trend has since spread to well beyond the OECD. Even in India, which still had birth rates of three children per woman in the beginning of this century, birth rates have fallen to just below replacement levels, and in China, birth rates are now lower than in the EU.

Graph 2: Total fertility rates over time (births per woman of childbearing age)

OECD (2025: 192-193)

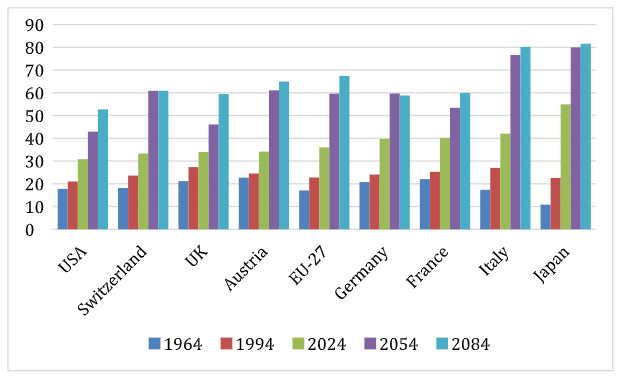

These trends have changed the population age profile. In 1954, the countries and regions that now constitute the EU-27 only had 15 people aged 65 and over for every 100 people aged 20-64. That ratio then went up to 17 per 100 in 1964, 23/100 in 1994, and 36/100 today (OECD 2025: 196-197). In France, Germany and Italy, it stands at around 40/100. These ratios are bound to rise much further still.

Graph 3: Old-age to working-age ratio (population aged >65 years in % of the population aged 20-64 years) over time

OECD (2025: 196-197)

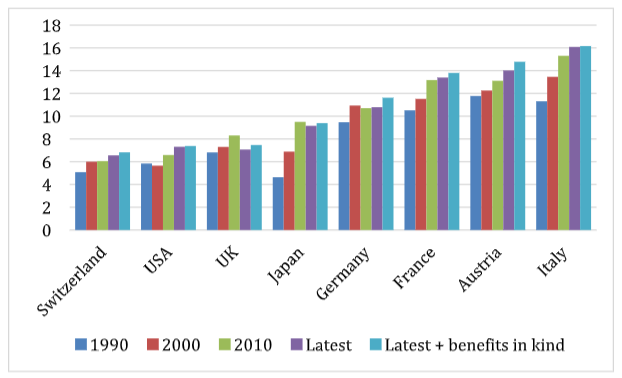

The result has been a major increase in public spending on old-age benefits, especially in those countries that rely predominantly on pay-as- you-go financing – although, interestingly, not by quite as much as the World Bank predicted.

According to the projection in AOAC, public pension spending in the OECD should have crossed the threshold of 15% of GDP by now. In Italy and Greece, this has indeed happened, with old-age spending rising to above 16% of GDP. Austria is only marginally behind, and several others are too close for comfort, certainly if we include benefits in kind. But a cost increase of that magnitude has nonetheless not happened across the board. Germany and Belgium have managed to keep pension spending below 12% of GDP, and Japan, despite very unfavourable demographics, below 10%.

Graph 4: Public expenditure on old-age cash benefits (in % of GDP) over time

OECD (2025: 222-223)

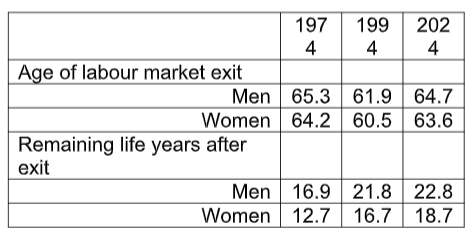

The main reason for that gap between World Bank predictions and outcomes is that a lot of OECD countries have since raised the retirement age, and scaled back subsidies for early retirement (OECD 2025: 28-31).

The second half of the 20 th century was characterised by a steady decrease in the effective age of labour market exit, leading to a steady increase in the number of years spent in retirement, over and above what can be explained by increases in life expectancy. This trend has since been halted, and partially reversed.

Table 1: Average effective age of labour market exit and average remaining life years after exit, OECD

OECD 2025: 202-205

Meanwhile, virtually every OECD country has seen a major increase in the employment rates of people aged 55-64 since the mid-2000s (OECD 2025: 200-201). OECD-wide, about one in five people in that age group who would not previously have been in employment are in employment now. This is a considerable unsung policy success.

The glass-half-full interpretation of these developments would be that pay-as-you-go systems have shown some capacity for reform within the system, perhaps more so than their critics have given them credit for. It may not be enough for ‘averting the old-age crisis’, but it has certainly helped.

Still, while the reversal of the trend towards earlier and earlier labour market exit is, of course, welcome, it remains worth asking: why did it take until the early 21st century for this reversal to take place? Indeed, why was there ever a trend towards early retirement when life expectancy has been rising all along, and when birth rates were already falling in the 1960s? A system which takes half a century for some modest parametric reforms is not an especially robust system.

Either way, there has been a clear upward trend in old-age spending, which is forecast to continue. It is worth bearing in mind that these figures do not capture the full cost of population ageing. They only cover spending programmes that are explicitly age-contingent. There are other spending programmes that are biased towards the elderly, but that would not be classified as ‘old-age benefits’, because they are open to other age groups as well. The obvious examples are healthcare, social care and disability benefits.

Some have argued that the increase in old-age spending is not really be a problem, because it is accompanied by a decrease in spending on the young. What we have to pay extra in pensions, we would save in schooling and childcare costs.

The World Bank already showed in 1994 that this is an illusion (World Bank 1994: 31-35). For a start, they showed that developed countries typically spent more than twice, and up to four times, as much on an old person than on a young person, in per capita terms. So even at this basic level, it is clear that the two spending categories cannot cancel each other out. But they also argued that even the partial offsetting effect is not guaranteed. Societies might respond to falling birthrates by spending more on each remaining child, rather than redirect those resources towards the elderly. Thirdly, even if there were offsetting effects, they would not be frictionless. Cash spending can be redirected easily enough, but the young and the old also consume different public services, which would have to be reconfigured. Put simply: a school or a childcare centre cannot just be converted into a retirement home. Rather than a simple rebalancing of budgets, there would be a scaling-down of some services, and a scaling-up of others.

This prediction has aged well. Despite falling birthrates, public spending on education has shown no clear trend over recent decades. Some OECD countries now spend slightly less on education than they did in 1994, some spend slightly more, but we cannot say that lower birthrates have led to any obvious savings (Our World In Data 2026). Meanwhile, healthcare spending has continued to show a clear upward trend OECD-wide, as the World Bank predicted it would. Population ageing has a real cost, and few offsetting benefits.

That cost is much greater than the amount of money being spent on old-age programmes. AOAC already highlighted that the choice of the financing mechanism for the pension system is not an economically neutral choice.

The economic effects of different pension systems

AOAC pointed out that different pension systems have very different economic effects:

“The choice among these alternatives and the specific form they take affect the welfare of the old by determining their share of the national pie. These choices also affect the welfare of the young by determining the size of the pie. Alternative policy options should thus be held to a dual standard: what is good for the old population, and what is good for the whole economy? The policies adopted by many countries fail this rest. They are beset with problems that spill over from the old age system to the rest of the economy”

(World Bank 1994: 25).

And elsewhere:

“A crucial question: Are productivity and GDP growth likely to be higher under one system than the other? Since pay-as-you-go funding breaks the market link between benefits and contributions, it may lead to evasion and labor supply distortions […]. In addition, many economists argue that pay-as-you-go schemes reduce saving, capital accumulation, and therefore growth”

(World Bank 1994: 92).

This argument is worth unpacking.

Labour supply effects of different pension systems

Suppose there are two otherwise identical countries, X and Y, which differ only in how they finance their pension systems: country X has a prefunded system, country Y uses pay-as-you-go. Even if the pension contribution rate is identical in X and Y, it will have very different effects.

In X, the pension contribution is not a transfer from the contributor to someone else. It is a mandatory savings rate. The contributor cannot access that money right now, but it is nonetheless not ‘lost’, just like a transfer from an instant-access current account to a fixed-term deposit account is not a loss. We could think of a retirement savings account as a special case of a fixed-term deposit account where the fixed term just happens to be extremely long.

In Y, the pension contribution has a very different meaning. It is more akin to a tax – although not identical. A tax is a payment to the state which does not entitle the taxpayer to anything specific in return, whereas a contributor to a pay-as-you-go pension system does build up future pension entitlements. If the link between pension contributions and entitlements is very strong, or at least perceived to be very strong, it is quite conceivable that contributors think of their contribution payments as a roundabout way of ‘saving’ for their retirement. If they do, they have no particular reason to try to avoid paying it.

The strength of that link does not just depend on the pension formula itself, but also how stable it is over time. Is the formula always the same, or is it subject to frequent changes? As long as the system is financially in rude health, and the pension formula is rarely changed or even talked about, a PAYGO contribution may be indistinguishable from a mandatory savings rate. But this is clearly not where we are today. For example, according to a recent survey from the UK, one in four young people do not even believe that there will still be a state pension by the time they retire. 1 Another one in five do not know, and another one in five say the state pension will ‘probably’ still be there. These people clearly do not see their National Insurance Contributions (the British version of social security contributions) as equivalent to a savings product. Unfortunately, there are no comparable surveys for the private prefunded pillar, but it seems implausible that people think of their private retirement savings in a similar way. Pension savers may be pessimistic about the future investment performance of their pension fund, but it would be very strange if one in four savers thought their pension fund was just going to evaporate entirely before they retire.

Thus, even if the contribution rate is identical in X and Y, it will nonetheless have very different effects. In Y, it will be seen as just another tax on labour, and taxes on labour discourage labour supply. The size of this effect is disputed, with different studies coming to different conclusions. But it seems safe to say that while the effect is probably not huge, it is far from trivial (Keane 2022). It is high among some subgroups, such as (current or potential) secondary earners, and, especially relevant for our purposes, older workers approaching retirement age. If country X has a

prefunded pension system while country Y uses pay-as-you-go, and if the two countries are otherwise identical, labour supply will be permanently higher in X than in Y. X will be a richer country than Y simply because they have a different pension system.

The positive labour supply effect of prefunded pension systems compared to pay-as-you-go has been empirically confirmed for the Chilean system (Corbo & Schmidt-Hebbel 2003; Edwards 2005), which is perhaps the most clear-cut example of a transition from the latter to the former.

Capital formation effects of different pension systems

Under ideal conditions, pension contributors in a PAYGO system see their contributions as an indirect form of saving. But even if everyone sees it that way, and if PAYGO contributions are genuinely functionally equivalent to savings from the perspective of an individual, they are not actually savings, and from an economy-wide perspective, the two are not equivalent at all. As the World Bank explained in 1994:

“A dominant pay-as-vou-go public pillar […] misses an opportunity for capital market development. When the first old generations get pensions that exceed their savings, national consumption may rise and savings may decline. The next few cohorts pay their social security tax instead of saving for their own old age (since they now expect to get a pension from the government), so this loss in savings may never be made up. In contrast, the alternative, a mandatory funded plan, could increase capital accumulation […]. A mandatory saving plan that increases long-term saving and requires it to flow through financial institutions stimulates a demand for (and eventually supply of) long-term financial instruments […]. These missed opportunities in a pay-as-you-go public pillar become lost income for future generations”

(World Bank 1994: 236).

The relationship between the pension system and the savings rate will not always be immediately obvious from macroeconomic aggregates. Germany and Austria have traditionally had very high savings rates, despite having pay-as-you-go pension systems with only weakly developed prefunded pillars. The United States and the United Kingdom, despite having much stronger prefunded pillars, also have much lower savings rates. But, again, if the only difference between two otherwise identical countries X and Y is that X has a prefunded and Y a pay-as-you-go pension system, X will have a higher rate of savings, and in particular, long-term savings. If those savings show at least a small bias in favour of the domestic market, X will have higher levels of investment and capital formation. It will be a more highly capitalised, more productive and richer economy than Y just because they have a different pension system (Feldstein 1995).

This does not mean that any move from pay-as-you-go to prefunding will automatically increase savings. For example, Bosworth and Burtless (2004) have found substantial offsetting effects between voluntary retirement savings (the third pillar in the World Bank model) and general savings. A plausible interpretation of these results is:

People can save for retirement in a variety of ways, including through savings that are not explicitly earmarked for retirement. A savings vehicle does not have to be called ‘a pension fund’ in order to act as one. Thus, if a government creates tax-privileged savings vehicles for retirement purposes, this may simply divert savings rather than increase their total amount. Even switching the main pillar from PAYGO to prefunding does not automatically guarantee a net increase in savings. If the government finances the transition between the systems via additional borrowing, that additional borrowing can cancel out much of the additional savings, or even all of it. A transition government needs to be willing to make genuine fiscal savings.

In the Chilean example, this has indeed happened, and it has demonstrably increased the national savings rate by several percentage points of GDP, even after subtracting offsetting effects (Coronado 1998; Bennett et al 2001; Corbo & Schmidt-Hebbel 2003). If done right, a switch from PAYGO to prefunding can make a country richer.

Populism and self-correction mechanisms in different pension systems

Adverse demographic developments amplify some of the worst tendencies inherent in PAYGO systems. But they do not originally create them. They are always there latently.

If we had to summarise the fundamental difference between prefunding and pay-as-you-go in one sentence, it would have to be this:

In prefunded systems, people acquire assets; in pay-as-you-go systems, they acquire political promises. The account balance of a retirement savings accounts represents a claim on productive assets in the economy: factories, machinery, office buildings, land, patents and copyrights etc. The fact that people’s pension wealth is backed by real assets does not mean that it is stable, or predictable. The value of assets fluctuates. It depends on the aggregate valuation of market participants. Market participants can over- or undervalue assets, and their valuation can change

suddenly and drastically. But for assets that are traded on markets, no single individual or institution has a huge influence on the market value. Nobody can simply decide at will that an asset ‘should’ be worth more, or that it ‘should’ be worth less.

This makes a prefunded pension system a system of hard budget constraints. Suppose somebody has $100,000 in their retirement savings account, or put differently, they own assets worth $100,000 earmarked for their retirement. There is no point in a politician or a political party declaring that that is ‘too little’, and that that person should really have $120,000. Because they do not have $120,000. Those additional $20,000 asset values are simply not there. And politicians cannot will them into existence.

Politicians can try to influence people’s retirement account balances indirectly. They can, for example, raise the mandatory savings rate, they can change investment rules in the hope that this will lead to higher returns, or they can change competition law in the hope that this will make the pension fund industry more competitive. But the assets still have to be generated and accumulated. They cannot be willed into existence by government fiat.

In a PAYGO system, pension entitlements very much can be raised by government fiat. If a government decides that somebody’s lifetime pension entitlement, which was previously $100,000, is now $120,000 – it is $120,000. It is whatever the government says it is at any given time, subject to how much they can extract from the economy. It can be changed by fiat, because it was created by fiat in the first place.

This explains both why PAYGO were initially so seductive for governments, and also why they later became such a headache for them. PAYGO systems are extremely lucrative when they are first introduced, or when they undergo an expansion on such a major scale that it counts as the introduction of a new system. When a PAYGO system is first introduced/expanded, the first generation of retirees receives a pension that they never contributed to, or only minimally so. This would be inconceivable in a prefunded system or pillar. A government can introduce the legal framework for a prefunded system/pillar, but at that point, there are no assets in the system yet, and a government cannot ‘introduce’ those. Even in the Chilean case, where the initial building up of pension fund wealth happened extremely rapidly due to sensationally high returns in the early years, it took about ten years for those assets to reach 20%, and twenty years for them to reach 50% of GDP (Niemietz 2008: 20-23). In a prefunded system, it takes a long before anything can be paid out. In a PAYGO system, the first pensions can be paid out on the very first day when the system officially comes into existence. A prefunded system arrives penniless, a PAYGO system arrives with a big bag of cash to spend straight away. Is it a surprise the politicians tend to find the latter system more attractive?

But eventually, the fiat character of the system becomes a liability for decisionmakers. Demographic changes such as a rising life expectancy put pressure on any pension system, whether PAYGO, prefunded, a mix, or something else entirely. Under any system, spending 20 years in retirement is more expensive than spending 10 years in retirement, for the same reason that a long holiday is more expensive than a short holiday. Until here, it is irrelevant what type of pension system we have, and switching from one system to another would not solve anything. But when we look at the way that this information filters through the system, and how people react to it – this is where it matters hugely what pension system we have.

Suppose in a prefunded system, somebody approaching retirement age has accumulated $100,000 in their retirement savings account, and the average remaining life expectancy after retirement is five years, giving them an annual income of $20,000. Now life expectancy suddenly rises by a year, so if that person still retires at the age they were originally going to retire, they can expect to spend six years rather than five years in retirement, on an annual income of 16,667 rather than $20,000. They can react to this in a variety of ways. They can delay retirement. They can increase their savings rate for the remainder of their working life. They can accept a lower living standard in retirement. They can switch part of their savings to a riskier, but potentially more rewarding, investment strategy. Or they can combine two or more of these options in some way.

But either way, it is a choice that they have to make. Circumstances have changed, and people have to adapt to those changed circumstances in some way.

In PAYGO system, it is the government which has to make the analogous choice. It can raise pension contributions, it can cut pension levels or delay increases, it can raise the retirement age, or it can try to make savings elsewhere. But either way, it is a political choice, and political choices can be challenged. Somebody – a person, a group or an institution – made that choice, and they could have made different choices. So for those dissatisfied with the results, it becomes a viable option to protest against that choice, which is why decisions to raise the retirement age are often highly controversial and politically charged. In places with both a PAYGO system and a strongly developed political protest culture, such as France or Greece, pension policy has become a graveyard of political careers.

Such protests have no real counterpart in prefunded systems. Who, exactly, would you be protesting against? Nobody ‘decided’ to increase the average life expectancy. A consequence of increasing life expectancy is that you will have to work longer, save more, and/or accept a lower retirement income, but there is no identifiable person, group or institution that is to blame for this. Nobody made that choice. There is no culprit, and nobody one could meaningfully protest against.

Prefunded systems depoliticise and depersonalise decisions about retirement. Not completely so: in Chile, even though the prefunded pillars of the multipillar system introduced in 1980/81 has now fully matured, pensions remain a political topic. But there is nonetheless a recognisable pattern. Among those OECD countries with the highest effective age of labour market exit, multipillar systems are overrepresented (e.g. Chile, Iceland, Mexico, the USA), while PAYGO systems are overrepresented at the opposite end of the spectrum.

The World Bank’s recommendations vs reality

The World Bank’s recommendations from 1994 were sound. Multi-pillar systems with major elements of prefunding really are superior to pay-as-you-go systems in a variety of ways. That message has thus far stood the test of time.

It is a message that has shifted national conversations. In the mid-1980s, the West German Minister for Social Affairs, Norbert Blüm, still famously campaigned with the slogan ‘denn eins ist sicher: Die Rente’ (=‘because one thing is certain: the [old-age] pension’). In the 1990s, the tone changed. Blüm’s own party, the Christian Democratic Union, said in their 1998 election manifesto:

“For a comprehensive and long-term stabilisation of the pension system, we want to encourage young people in particular to make supplementary provisions for their retirement early on. (CDU 1998: 21).”

Without linking it to specific policy measures, they also hinted at a strengthening of occupational pension schemes. We could read this as an at least vague allusion to the World Bank model.

By that stage, even the Social Democrats talked about ‘four pillars’ of old-age provision (SPD 1998: 21), unmistakenly influenced by AOAC. (Their four pillars were the existing PAYGO system, occupational pensions, individual long-term savings, and an unspecified form of ‘popular capitalism’.) A few years later, it was a ‘red-green’ coalition (Social Democrats + Green Party) which introduced the ‘Riester Pension’, which was supposed to be a savings-based pillar in the pension system.

But how serious were those attempts? Did they actually move the needle, or was this mostly rhetoric and tokenism?

In 1994, there were hardly any real-world examples of pension systems that resembled the World Bank’s three-pillar model. Switzerland, the UK and the Netherlands were probably the closest thing. Chile and Australia had also created the basic outlines of such a system, but their savings pillars were not yet sufficiently capitalised.

How about today?

Prefunded pillars: recent past to present

About half of the 38 member states of the OECD have some kind of prefunded pillar, resembling the second pillar in the World Bank model, as an official part of their pension system. However, the mere existence of such a programme does not make a multi-pillar system. The design and the relative weight of the pillars also matters.

For example, the World Bank was very clear that they wanted the pre-funded pillar to be privately managed, so a sovereign wealth fund would not count. While they did not provide us with specific parameters, they made it quite clear that they did not envisage the pillars to be equal partners. Take the following passage:

“The public pillar would […] have the limited object of reducing old age poverty and coinsuring against a multitude of risks. […] Having an unambiguous and limited objective for the public pillar should reduce the required tax rate substantially […] The average replacement rate financed through the public pillar should be modest, in keeping with its poverty alleviation goal” [emphasis added] (World Bank 1994: 238-242).

We can argue about what exactly this means. If the relative weights of the public PAYGO pillar, the mandatory prefunded pillar and the voluntary prefunded pillar is 50:40:10, does this count as a three-pillar system in the spirit of AOAC? Or is the public pillar to large and overbearing?

But what we can do without putting words into the authors’ mouths is narrow things down. If the relative weight of the pillars is 80:10:10, it is safe to say that this is not what the authors had in mind, because such a system would clearly put too much weight on the PAYGO pillar. Conversely, if the breakdown is 25:50:25, it seems reasonable to assume that the authors of AOAC would have accepted that.

With that in mind, in this section, we will look at various parameters of systems with prefunded pillars, to decide which of them come close enough to the three-pillar system.

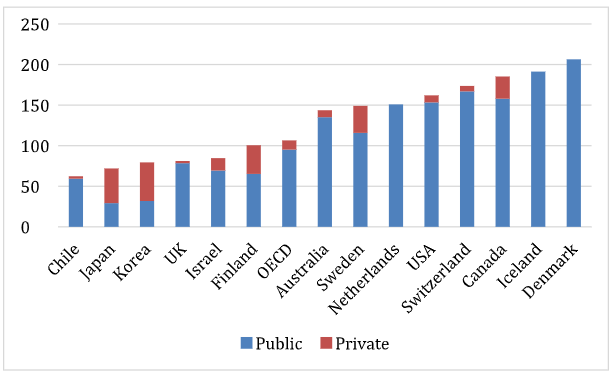

One such parameter is the total value of assets held in private pension funds or close equivalents. In a mature system with a strong prefunded component, that value exceeds 100% of the country’s GDP. There are only eight OECD countries where this is the case: Australia, Sweden, the Netherlands, the USA, Switzerland, Canada, Iceland and Denmark. In addition, Chile, the UK, Israel and Finland also have considerable prefunded pillars, but substantially less than the former group. The same could be said about Japan and South Korea, but in their case, a large proportion of those assets are held by government entities. In most of Western Europe, the equivalent figures are less than a quarter of GDP; in Germany and

Austria, we are talking about mere single-digit figures.

Graph 5: Assets earmarked for retirement (% of GDP), 2024

OECD (2025: 234-235)

This is an improvement compared to the early 1990s, when the figures were: Denmark 60%, US 66%, Switzerland 70%, UK 73%, Netherlands 76% (World Bank 1994: 173-174). But the comparison also shows how much progress could have been made which has not been made. Over the course of those years, Australia, Canada, Denmark and Switzerland have increased the value of their pension assets by 100% of their respective GDPs or more, thus adding an entire year’s worth of economic output to their pension pots.

Another indicator of the relative weight of the prefunded pillars is to simply look at how much they contribute to the non-wage income of the retired population.

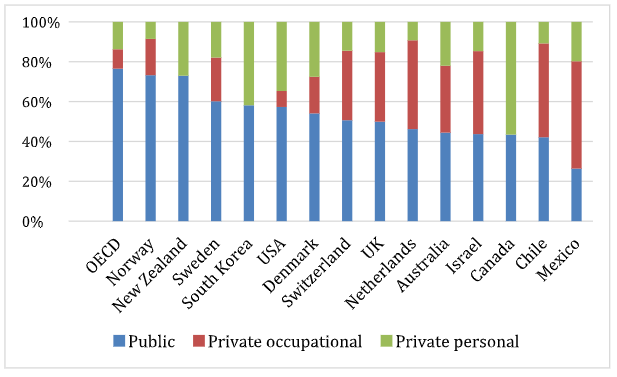

There are only eight OECD countries where those pillars account for half of old-age income or more: Mexico, Chile, Canada, Israel, Australia, the Netherlands, the UK and Switzerland. There are another four where they account for between 40-50% (OECD 2025: 208-209). We will count the former eight as AOAC-compliant on this measure, and the latter four as partially so.

Graph 6: Income from private pension funds as a % of total non-work income of people aged >65 years, 2022

OECD (2025: 208-209)

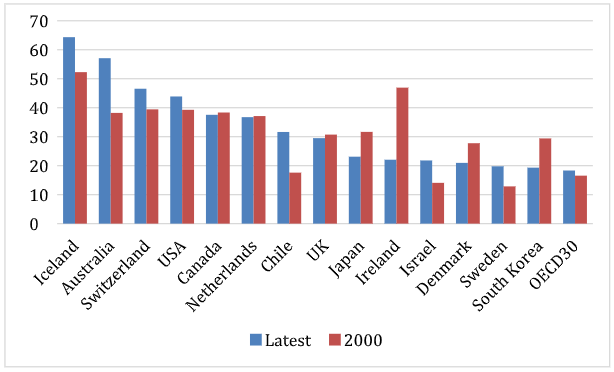

A different way of looking at this is to express private pension spending (the amount withdrawn from pension funds) as a percentage of total pension spending. There are only two countries – Iceland and Australia – where this accounts for the majority of pension spending, although Switzerland and the US are borderline cases (OECD 2025: 224-225). At a stretch, we could include Canada, the Netherlands and Chile as pension systems that vaguely resemble what the World Bank must have had in mind in 1994. The OECD average is an 18% private vs 82% public split, which is miles away from the three-pillar system. Germany and Austria are, once again, in the single-digit figures.

Graph 7: Private pension spending in % of total pension spending, 2000 vs latest available year

OECD (2025: 224-225)

OECD-wide, the contribution of the private pillar has only increased by two percentage points since 2000, indicating very little progress in this direction.

Prefunded pillars: present and future outlook

Pension reforms have a long lag time, so any measure that describes the situation of today necessarily tells us more about the reforms of yesteryear, and misses out on more recent ones.

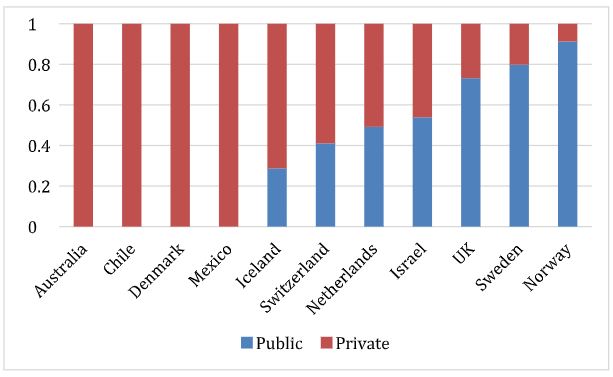

A more forward-looking measure would be to look at the pension contributions people pay today: does an average income earner pay more into public schemes, or more into their own accounts? The chart below shows the breakdown for systems with non-trivial private pillars, which can be mandatory, quasi-mandatory (covered by union agreements rather than government legislation), or based on auto-enrolment (people are automatically signed up, but can opt out at no cost if they want to). In Australia, Chile, Denmark and Mexico, there is no formal public pension contribution anymore, although, of course, people still pay for the public pillar via general taxation. In Iceland and Switzerland, the private component clearly outweighs the public one, while the Netherlands and Israel are borderline cases.

Graph 8: Public-private split of pension contributions for an average income earner

OECD (2025: 220-221)

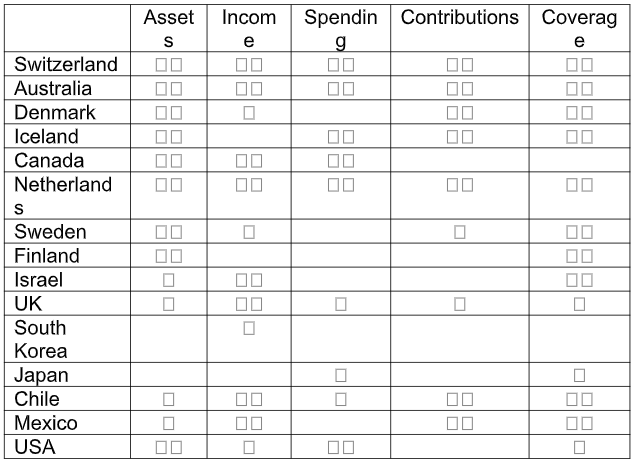

Taken together, only Switzerland, Australia and the Netherlands unambiguously qualify as three-pillar systems of the type proposed by the World Bank in 1994. Denmark, Iceland, Chile, Mexico and the USA also have a strong claim to be included in that category, while Canada, Sweden, Israel and the UK are somewhat close, even if they are not all the way there. There are several other systems which have elements of the three-pillar system even if we would not include them in that category.

Table 2: Proximity of pension systems to the World Bank model, ✓✓ = close, ✓ = maybe/partially

Overall, though, it is much easier to find examples of pure Bismarckian PAYGO models than of three-pillar models in the OECD. The lessons of Averting the Old-Age Crisis have yet to be fully learned. Governments have paid lip service to that model, but they have yet to walk the talk.

This is a shame because where they have been seriously tried, prefunded pillars have often achieved impressive results. In Chile, the Netherlands, Iceland, Switzerland, Denmark, Finland, Australia, Canada and elsewhere, private pension funds have sustained average real interest rates above 2.5% per annum for 20 years or more (OECD 2025: 238-239), in a period which covered the Global Financial Crisis, the eurozone crisis, the Covid-19 pandemic and other adverse events. Both the World Bank’s warnings and their proposed alternative model have stood the test of time. Hopefully, it will not take another 32 years for these lessons to be applied more widely.

References

Bennett, H., N. Loayza and K. Schmidt-Hebbel (2001) ‘Un Estudio del Ahorro Agregado por Agentes Economicos en Chile’, Central Bank of Chile.

Bosworth, B. & Burtless, G. (2004) Pension Reform and Saving. National Tax Journal 57(3): 703-727 https://www.jstor.org/stable/41790237

CDU (1998) ‘Wahlplattform 1998’. Bonn: Christlich Demokratische Union.

Corbo, V. & Schmidt-Hebbel, K. (2003) ‘Efectos Macroeconomicos de la Reforma de Pensiones en Chile’, Central Bank of Chile.

Coronado, J. (1998) ‘The Effects of Social Security Privatization on Household Saving: Evidence from the Chilean Experience’. Board of Governors of the Federal Reserve System Finance and Economics Discussion Series 98-12. http://dx.doi.org/10.2139/ssrn.84028

Dattani, S., Rodés-Guirao, L., Ritchie, H., Ortiz-Ospina, E. & Roser, M. (2023) ‘Life Expectancy’. Our World in Data. https://ourworldindata.org/life-expectancy

Edwards, A. C. (2005). Pension reforms and employment. International Economic Journal, 19(2): 305–319 https://doi.org/10.1080/10168730500080600

Feldstein, M. (1995) ‘Social security and Saving: New time series evidence’, NBER Working Paper 5054. National Bureau of Economic Research.

Keane, M. (2022) ‘Recent research on labor supply: Implications for tax and transfer policy’, Labor Economics 77. https://www.sciencedirect.com/science/article/abs/pii/S0927537121000610

Niemietz, K. (2008) Die kapitalgedeckte Altersvorsorge am Beispiel Chile: Ergebnisse, Auswirkungne, Lehren und Verbesserungsmöglichkeiten. Hamburg: Diplomica Verlag.

OECD (2025) Pensions at a Glance 2025. OECD and G20 Indicators. Paris: Organization for Economic Cooperation and Development. https://www.oecd.org/en/publications/pensions-at-a-glance-2025_e40274c1-en/full- report.html

Our World In Data (2026) Government spending on education by spending type and level of education. https://ourworldindata.org/grapher/education-spending

SPD (1998) ‘Arbeit, Innovation und Gerechtigkeit: SPD-Programm für die Bundestagswahl 1998. Beschluß des außerordentlichen Parteitages der SPD am 17. April 1998 in Leipzig’. Bonn: Sozialdemokratische Partei Deutschlands.

World Bank (1994) Averting the Old Age Crisis. Policies to Protect the Old and Promote Growth. New York: Oxford University Press.

1 Financial Times: ‘Half of savers believe state pension won’t exist for young people’, 19 October 2023. https://www.ftadviser.com/content/3f607464-1508-50e4-8b3e-f2e0e198f2dc