Private equity: An obituary

For decades, private equity (PE) has been lauded as a superior form of capitalism, a bastion of entrepreneurial vigor amid sclerotic public corporations. The value proposition − generate high returns by transforming companies through operational improvements, strategic growth and financial optimization, rather than relying on market trends − was, and remains, intuitively powerful. After all, the vast majority of economic activity occurs within privately held companies.

It is in the smaller, more agile entities, free from the quarterly earnings pressures and the suffocating bureaucracy of public markets, that true innovation and value creation are said to flourish. This narrative, compelling in its simplicity and economic plausibility, captivated the global investment community, transforming private equity from a niche strategy into a dominant, multi-trillion-dollar asset class.

But the very appeal of private equity as a concept – as raw, unfettered entrepreneurship – has obscured a more troubling reality. Private equity as an asset class is a failure, and its demise is approaching sooner than anticipated.

The disconnect is crucial. The romantic ideal of a shrewd investor identifying a diamond in the rough, nurturing it with capital and expertise, and guiding it to greatness is a powerful story. It is, however, not an investment strategy that can be systematically replicated and scaled to absorb trillions of dollars in institutional capital without profound compromises.

The forces that have led to private equity’s current state of crisis are not merely cyclical headwinds; they are structural flaws, some self-inflicted and others a consequence of a changing macroeconomic landscape. The once-bright promise of a premium return for embracing illiquidity and complexity has faded, leaving investors to question the very foundations of the asset class and the decisions associated with it.

The seeds of PE’s self-destruction

A significant portion of the blame for private equity’s decline lies with the industry itself. In its relentless pursuit of assets under management (AUM) and the attendant management fees, the industry has strayed far from its entrepreneurial roots. The core tenets of prudent investment have been replaced by a culture of financial engineering, questionable valuations and a jargon-laden lexicon that obfuscates rather than clarifies.

First, the quality of many private equity-backed business plans and their associated valuations has become, at best, dubitable, and at worst, outright fraudulent. The pressure to deploy vast sums of capital – a staggering $2.18 trillion in global “dry powder,” the committed but uninvested capital held by private equity, as of March 2025 – has led to a chase for deals at any price.

The ubiquitous “hockey stick” growth charts, aggressive churning assumptions and reliance on ever-expanding valuation multiples bear little resemblance to economic reality.

The sophisticated financial models and due diligence reports that accompany these transactions often mask a simple truth: The projections are based on fantasy. The ubiquitous “hockey stick” growth charts, aggressive churning assumptions and reliance on ever-expanding valuation multiples bear little resemblance to economic reality. This is not value creation; it is a game of passing an overvalued asset from one fund to another until the music stops.

The industry is now sitting on a bloated inventory of an estimated 31,000 companies, collectively valued at a staggering $3.7 trillion, with a persistent and widening gap between on-paper valuations and what a rational buyer is willing to pay in the real world.

Second, the industry has made a pledge it can neither keep nor, in truth, should ever have made: the promise of transparency and benchmarking. For years, limited partners (LPs) have clamored for greater insight into fund performance, demanding standardized reporting and the ability to compare managers on a like-for-like basis. In response, the industry has paid lip service to these demands, creating a veneer of transparency while fiercely guarding the very opacity that allows it to manipulate returns.

The promised premium for investing in private equity has evaporated.

The fundamental contradiction has been ignored. True entrepreneurship is inherently obscure and ambiguous. It involves alertness, asymmetric information, unique circumstances and outcomes that cannot be neatly categorized or benchmarked. To demand transparency is to demand the impossible, and to promise it is to engage in a deception. The surprise is not that the industry has failed to deliver on this promise, but that so many sophisticated investors accepted it in the first place.

Third, and most damningly, the promised premium for investing in private equity has evaporated. After accounting for high fees (typically a 2 percent management fee and 20 percent of profits), transaction costs, information costs and the cost of capital, the net returns to investors have often failed to outperform simple, low-cost public-market indices.

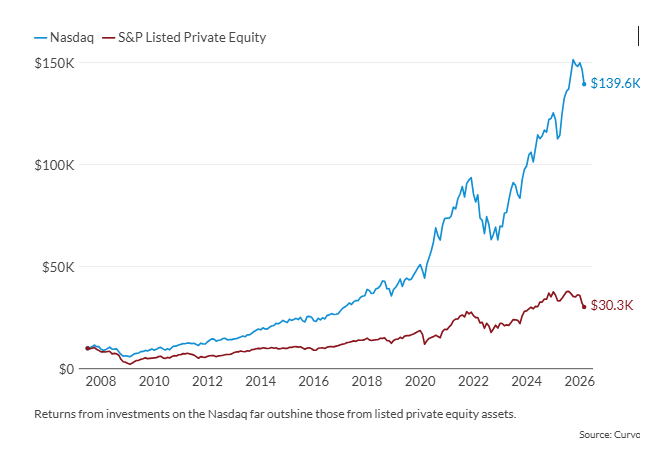

Facts & figures: Returns on stocks beat private equity

Recent data starkly illustrate this underperformance. A review of 15 large private-equity-focused evergreen funds revealed a median net return of just 11 percent in 2025. This pales in comparison to the S&P 500’s 17 percent net total return and the 22 percent return of the MSCI ACWI Index for the same year. The underperformance is not an anomaly; over the three-year period from 2023 to 2025, these same PE funds delivered a median annualized return of 11 percent, while the S&P 500 returned 22 percent annually.

The engine of private equity – the process of buying, improving and selling companies – has stalled. While the number of exits rose slightly to 3,149 in 2025, the total value of those exits plummeted by 21 percent to $412 billion, a clear signal of a liquidity crisis for investors who depend on distributions to meet their own obligations.

External influences: A hostile environment

The industry’s internal failings have been dangerously exacerbated by a macroeconomic environment hostile to its fundamental business model. The narrative of PE as a haven from public market volatility has been shattered by the very markets it sought to distinguish itself from.

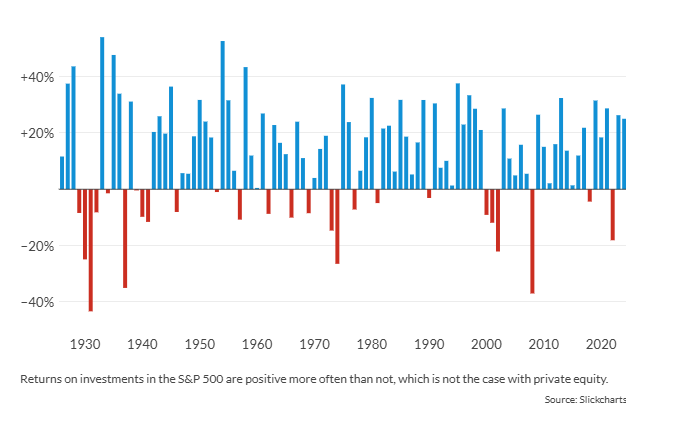

Ironically, the robust performance of public equities has become one of private equity’s greatest threats. While PE firms have struggled to generate “alpha” – the value added to the business by the PE manager’s skill that boosts returns so they beat industry benchmarks – public markets have delivered handsome returns, making the high fees and illiquidity of private equity a much harder sell. The S&P 500, for instance, recovered from an 18 percent loss in 2022, posting impressive gains of 26 percent in 2023 and 25 percent in 2024, followed by a solid 18 percent return in 2025. For an investor, the question becomes stark: Why lock up capital for a decade in an opaque, high-fee structure for returns that, at best, track a low-cost index fund?

Facts & figures: S&P 500 returns

Simultaneously, a climate of economic uncertainty and persistent inflation has fueled a significant flight to safety, with traditional hard assets like gold and silver experiencing a dramatic resurgence. Gold ended 2025 with a staggering 65 percent gain, its sharpest annual rise in over four decades, with its price blowing past $4,300 per ounce. Silver’s performance was even more spectacular, jumping 144 percent in the same year.

This renewed interest in precious metals, which continued their ascent into early 2026 with gold topping $5,100 an ounce, has diverted capital that might otherwise have been allocated to alternative investments like private equity. Investors have found a more reliable and liquid store of value in commodities than in the convoluted structures of PE funds.

The most direct verdict on the state of private equity comes from the public markets themselves, where the shares of the industry’s titans have been faltering. The stock prices of these publicly listed managers serve as a real-time barometer of investor confidence in their business model. The start of 2026 has been brutal. As of mid-February, shares of industry leaders like Blackstone and Apollo Global Management were down approximately 12 percent, with Ares Management falling 15 percent and KKR & Co. tumbling nearly 16 percent.

This poor performance reflects deep-seated concerns about the sustainability of fee-related earnings, the viability of the private credit market that has fueled so much of their growth and the mounting pressure on their unrealized portfolios.

Scenarios

Most likely: The zombie apocalypse

The most probable, and depressing, future for private equity is that the industry does not die but continues in a state of undeath. Funds will continue to raise capital, albeit in smaller amounts – fundraising already declined 11 percent in 2025 – and the cycle of financial engineering will persist. Returns will remain mediocre, tracking public markets and failing to compensate for the fees and illiquidity. The industry will become a permanent, bloated fixture of the financial landscape, a testament to the triumph of marketing over substance.

Less likely: The great private equity extinction

A less likely, but somewhat welcome scenario, is that the PE asset class collapses entirely. A wave of defaults, LP revolts and regulatory crackdowns could trigger a complete loss of confidence. The flow of capital would cease, and the industry would be forced into a painful and protracted liquidation. While this would be a chaotic process, it would ultimately cleanse the system of the excesses and malinvestment that have come to define it.

Least likely: The entrepreneurial renaissance of managing assets

This is the most hopeful, though least likely, scenario. Private equity undergoes a profound differentiation based on necessity. A smaller, more focused group of investors rediscovers the true ethos of entrepreneurship. They embrace thrift, humility and a deep understanding of business operations over financial wizardry. They shun jargon and complexity, focusing instead on genuine value creation. Crucially, they embrace the inherent obscurity and ambiguity of their craft, recognizing that the greatest opportunities lie in the shadows rather than under the glare of standardized benchmarks. This would be a return to the origins of private equity, a revival of its founding spirit.

While the first scenario seems the most likely path, we can hold out hope for the third as the market may force it into existence.

This material was originally published here: https://www.gisreportsonline.com/r/private-equity-obituary/