Eurozone: Convergence or divergence?

by Tom Bugdalle and Moritz Pfeifer, Institute for Economic Policy, Department of Economics, University of Leipzig

We revisit the euro’s promise of convergence through a new Divergence Monitor tracking business and financial cycle synchronization since the 1980s. Business cycles became more aligned after 1999, but financial cycles stayed volatile and split into persistent core–periphery clusters. As inflation gaps persist and enlargement continues, one monetary policy increasingly risks misfitting many.

Nous réexaminons la promesse de convergence de l’euro grâce à un nouvel monitor mesurant la synchronisation des cycles réels et financiers depuis les années 1980. Les cycles réels se sont rapprochés après 1999, mais les cycles financiers restent instables, structurés en clusters centre– périphérie. Avec l’élargissement, une politique unique s’adapte moins.

1. The promise of the euro

When the euro was introduced in 1999, the architects of the monetary union promised that a common currency would bring Europe economically and politically closer together. The hope was that income levels would converge, economic cycles align, and the European Central Bank act as the guardian of stability. Europe’s political leaders at the time presented the new currency as a political and economic promise. German Chancellor Helmut Kohl described the euro as “a supporting element in building a stable, weather-proof house of Europe,” while Italian President Carlo Azeglio Ciampi declared that the euro would “strengthen and accelerate Europe’s integration.”

Before the introduction of the euro, economists such as Paul Krugman and Milton Friedman warned of the risks of a common currency. Krugman (1990) feared that high heterogeneity within the euro area would lead to growing economic imbalances. Friedman (1997) worried that a uniform monetary policy could lead to political tensions and division. Their warnings proved prescient. Since the launch of the euro, the currency area has experienced a sovereign-debt crisis, growing political polarization, and, most recently, a period of historically high and heterogenous inflation rates. The recurring pattern of crisis and response has revealed that monetary integration alone may not guarantee economic convergence.

As the euro area’s inflation rate has returned to the ECB’s 2 percent target, changes in price levels remain divergent within the euro area (see Maurer, 2023). Inflation in Estonia (5.2 percent), Austria (4 percent), and the Netherlands (3.1 percent) remains well above target, while France (1 percent), Finland (0.5 percent), and Cyprus (-0.7 percent) are already below. While the ECB and the European Commission search for explanations of such disparities they miss answering the central question. Is the eurozone sufficiently synchronized to justify a single monetary policy? When Ursula von der Leyen declared in June 2025 that “Thanks to the euro, Bulgaria’s economy will become stronger,” she reinforced the promise of the Euro. With Bulgaria having joined the euro zone in 2026 and others waiting in line, our new Divergence Monitor offers a tool to assess whether the past promise of convergence has been kept. Although Bulgaria is not yet included, our index provides an assessment of business and financial cycle convergence between the euro member states before and after 1999.

2. The importance of symmetric business and financial cycles

The theory of optimum currency areas (OCA), developed by Robert Mundell (1961) and later extended by McKinnon (1963) and Kenen (1969), helps explain under what conditions a group of countries benefit from sharing a common currency. OCA theory asks when the advantages of a shared

currency exceed the cost of losing national monetary autonomy. A shared currency reduces transaction costs, removes exchange rate uncertainty, and can foster trade. At the same time, it deprives members of their sovereign monetary policy and exchange rate adjustments that can help absorb shocks.

Mundell identified the synchronization of business cycles as one of the most important conditions for a successful currency area. Only if member economies expand and contract in similar ways, a single monetary policy can pursue its objective of price stability for all. McKinnon found that a currency union requires high trade openness as well as wage and price flexibility, allowing economies to adjust internally when facing asymmetric shocks instead of relying on exchange rate changes. Kenen added that production diversification and fiscal integration would help reduce the impact of asymmetric shocks. In short, if adjustment mechanisms work efficiently, economic cycles tend to be more broadly aligned and a monetary union can be reasonable. If these conditions are not met, the costs of a common currency outweigh the benefits.

The United States is often cited as a successful example of an existing currency union. With one official language and fewer cultural barriers, workers in the US can more easily move between states. That allows the labor market to absorb regional shocks. The euro area, by contrast, remains a collection of sovereign states with heterogenous labor laws, cultural differences and 24 official languages. Consequently, labor mobility is lower and regional shocks are harder to absorb. When one member country falls into recession while another is expanding, the common monetary policy cannot respond optimally to both. In such cases, competitiveness must be restored through internal devaluation in terms of nominal wage and price cuts, rather than through currency depreciation. While a depreciation would also reduce real wages and prices, it is a faster and less painful adjustment.

Suppose Germany is in crisis while the Spanish economy is booming. In this scenario, the ECB is presented with a dilemma. Interest rate cuts would, as they did between 2003 and 2007, reinforce the Spanish boom and the associated inflationary pressure, while interest rate hikes would accelerate the German downturn. Before the great financial crisis, historically low interest rates fueled the Spanish economy but also created exaggerations in the Spanish real estate market, which ultimately imploded during the so-called euro crisis. This divergence showed that when member states’ economic cycles are not aligned, a uniform monetary policy can amplify, rather than mitigate, asymmetric cycles. Such experiences demonstrates that both business and financial cycle symmetry are essential for macroeconomic stability in a currency union.

3. How the Divergence Monitor works in practice

Our analysis begins by constructing two indices for each euro area country that captures cyclical movements in the real economy and in financial markets. The business-cycle index captures quarterly changes in GDP, private consumption, investment, and unemployment. The financial-cycle index captures quarterly changes in outstanding credit, residential property prices, equity prices, and government-bond prices. Each variable is standardized to allow for comparisons across time and between countries. The four variables are then aggregated by using weights, that are based on the time-varying co-movements. This method is based on Schüler et al. (2020) and gives more weight to variables that move more closely together at a given moment. It corrects a central limitation of static trend-based methods, such as those using the Hodrick–Prescott filter, which remove low-frequency movements and fix the cycle length ex ante. In contrast, our method allows cycle duration and amplitude to evolve with the data.

A second improvement concerns how synchronization across countries is defined. Most earlier studies interpret convergence as movement toward a single reference mean. Such mean-based measures implicitly assume that the average represents an optimal state. However, if the cycles form clusters, as is well-documented for the euro area, the mean may fall between them, in a region with no observations. Distances from that mean will look large even when countries in the same cluster move closely together. By computing country-pair distances, we avoid this problem.

Lastly, our method allows for minor phase shifts. Conventional distance measures, such as Euclidean or correlation-based metrics, classify two economies as divergent when their cycles exhibit a slight lead or lag neglecting the similarity of the cycle shape. That may be too strong of an assumption for a monetary union of many countries, where business and financial cycles naturally lead or lag each other by just a few quarters. Dynamic Time Warping (DTW) adjusts the timing of the two series within a narrow window to compare their shapes. It finds the path with the smallest total difference, so it recognizes that two economies may move together even if one hits turning points slightly earlier. Smaller DTW distances indicate greater synchronization among member states.

Once the pairwise distances are calculated, we aggregate them to obtain a measure of divergence for the entire euro area. Each country pair is weighted by its combined share of euro area GDP. The resulting Divergence Monitor produces one index for business cycles and one for financial cycles. These indices track the evolution of synchronization over time. Lower values indicate convergence, larger values point to increasing divergence. To examine structural pattern, we group countries according to the similarity of their DTW profiles using a clustering procedure based on DTWKMeans. These clusters reveal persistent groupings such as core and peripheral member states.

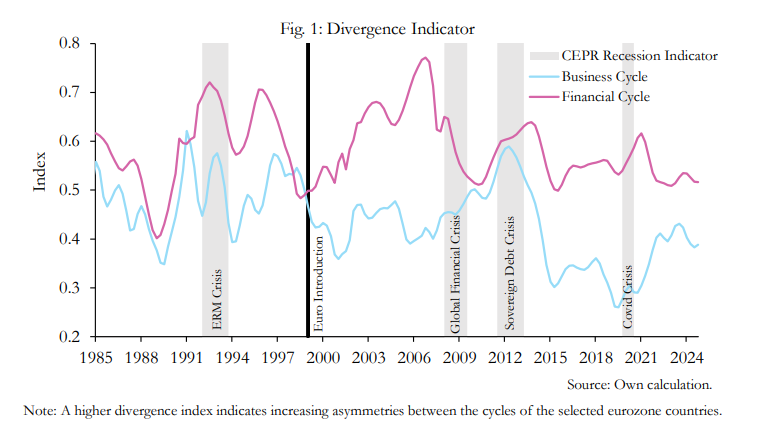

4. No substantial convergence, particularly in the financial cycles

In the early 1990s, asymmetries in both business and financial cycles fluctuated considerably. The introduction of the euro initially led to more business cycle convergence. This convergence came to a halt with the outbreak of the global financial crisis and the subsequent Euro crisis (see Fig. 1). In 2012, business cycle asymmetries reached a temporary peak reflecting disproportionately deep recessions in southern Europe. In the following years, business cycles noticeably converged again after Mario Draghi’s famous “Whatever it takes” speech and the subsequent wave of unconventional monetary policy by the ECB. Since 2020, a rapid increase in asymmetries has been observed once again.

Although there has not been a linear trend of business cycle convergence, we can observe an average increase in business cycle synchronization since 1985. Financial cycles, by contrast, have been both more volatile and more asymmetric throughout the entire observation period. The degree of divergence in financial cycles shows abrupt rises and falls, occurring in shorter and more intense phases than in business cycles.

Financial cycles were relatively aligned around 1989, coinciding with growing coordination of monetary policies and financial-market liberalization before the monetary union. A clear decoupling between financial markets and the realeconomy emerged during the 1992 Exchange Rate Mechanism crisis, when interest-rate increases by the German Bundesbank triggered capital outflows from other European economies. After the introduction of the euro, the gap between business and financial cycle symmetry widened once again. While financial cycles diverged, business cycles converged. The largest surge in financial divergence occurred in the run-up to the global financial crisis, as lower borrowing costs in peripheral member states encouraged capital inflows from the north and fueled credit and asset-price booms. When the ECB began tightening its monetary policy between 2005 and 2007, and with the subsequent outbreak of the financial crisis, these financial asymmetries disappeared until around 2010. Two smaller waves of financial divergence are visible during the sovereign-debt crisis and the COVID-19 pandemic.

5. One currency area, two realities

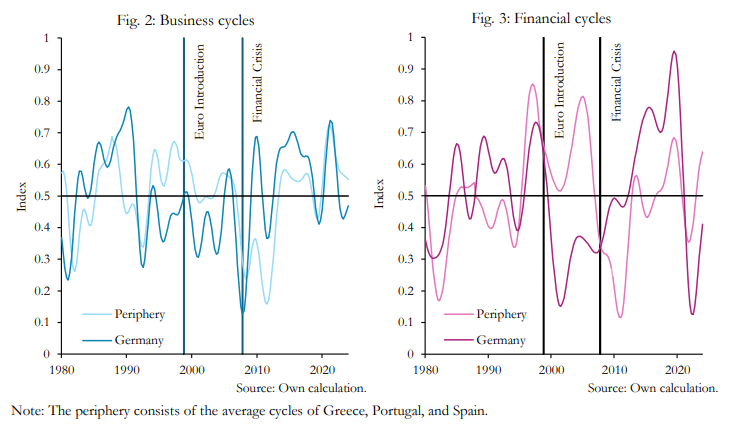

We cluster common developments for both our cycles that show two groups of countries with similar cyclical patterns emerging in the euro area. There is a group of more fiscally conservative countries, consisting of Germany, Finland, and the Netherlands, and a group of peripheral countries, consisting of Greece, Spain, and Portugal. These clusters can be found in both economic cycles, but even more clearly in financial cycles. Their persistence may indicate how institutional differences continue to create cyclical asymmetries within the monetary union.

The asymmetry between Germany and the three peripheral countries is particularly striking. In the late 1990s and early 2000s, the periphery experienced a strong economic upswing, while the German economy weakened (see Fig. 2). In 2008, Germany reached its economic low point, while the periphery did not reach it until the euro crisis in 2011. After the financial crisis and with the onset of unconventional monetary policy, the German economy grew, while the peripheral countries recovered only slowly. As the ECB could not properly react to these asymmetries, it was inclined to gradually push interest rates to the zero lower bound and pursue a policy of quantitative easing.

The financial cycles show a similar pattern but with greater amplitude (see Fig. 3). Between 1985 and the year 2000, the financial cycles of Germany and the periphery were relatively synchronized. The gap between the two financial cycles started to grow the first few years after the introduction of the euro. The divergence widened through the mid-2000s, as asset and housing markets in southern member states overheated, whereas German financial markets stayed comparatively flat. The German financial cycle only picked up after the euro crisis and in the wake of quantitative easing. By the 2010s, asset prices and credit growth accelerated mainly in Germany, whereas the periphery remained in a prolonged phase of stagnation. This almost mirror-image pattern supports the early warnings of economists like Krugman and Friedman. When member states differ too much in their economic structures, a single monetary policy can end up exaggerating imbalances by fueling booms in some countries while holding back recovery in others.

6. Combating symptoms

Our results do not show a linear path of convergence for the euro area after the introduction of the Euro. The current environment of divergent inflation rates once again raises the question, whether the ECB can adequately pursue its mandate of price stability in a currency union with such heterogenous clusters. As the euro area enlarges, this issue is likely to intensify rather than diminish. The scheduled accession of Bulgaria to the euro area on 1 January 2026 will be another test for the currency union. With a gross domestic product per capita of €16,110, which is barely 40 percent of the euro area average, Bulgaria will be the poorest country in the currency union. Incorporating a less developed economy with shallow capital markets into the monetary union entails the risk of adding more heterogeneity to an already heterogenous group of countries.

The application of our divergence monitor to prospective members remains limited by data availability. However, it allows us to evaluate the initial promise of convergence by observing the development of cyclical (a)symmetries. Over our sample, business cycle asymmetries are at historic lows, while financial asymmetries remain at a relatively higher level. This result reflects the dominant role that financial market stability has played in monetary policy decisions. While the ECB’s primary mandate is to maintain price stability, it must also consider the risk that a tighter monetary policy could trigger financial instability. Anticipating renewed imbalances, such as a future sovereign debt crisis, the ECB introduced the Transmission Protection Instrument (TPI) in 2022. This tool allows for disproportionate purchases of government bonds from highly indebted member states. In practice, the Eurosystem has already tilted its PEPP holdings toward Italian, Spanish, and supranational securities. Consequently, sovereign bond yields have become increasingly compressed, and risk premia no longer fully reflect market-based assessments of debt sustainability across the euro area.

While such measures may temporarily reduce or simply mask fragmentation in the euro area, they do not address the structural cause of divergence, as described by Mundell, McKinnon, and Kenan. Favoring specific countries through discretionary asset purchases blur the line between monetary and fiscal policy and may drive existing structural differences. By reducing the incentives for fiscal discipline, highly indebted member states, especially in the periphery, will be inclined to delay reforms that would be necessary to move closer towards an optimal currency area. In this case, the warnings of Krugman and Friedman may once again prove prescient. Sustainable convergence requires reforms that dismantle rigid labor market regulations, enhance price flexibility, and strengthen a rule-based central bank. As policymakers discuss new policy tools or consider future enlargements of the euro area, our Divergence Monitor can provide an empirical reference point, helping to distinguish between temporary misalignments and persistent asymmetries. Only by systematically observing existing asymmetries can the euro area find ways toward an optimal currency area.

IREF Policy Paper

No. 2026-PP01

April 2026

bugdalle@wifa.uni-leipzig.de

pfeifer@ wifa.uni-leipzig.de

Literature

Bugdalle, Tom; Pfeifer, Moritz (2025): Warpings in Time: Business and Financial Cycle Synchronization in the Euro Area, SSRN Electronic Journal. Available online at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5238187.

Friedman, Milton (1997): The Euro: Monetary Unity to Political Disunity?, Project Syndicate, August 28, 1997. Available online at https://www.project-syndicate.org/commentary/the-euro–monetaryunity-to-political-disunity (accessed on July 3, 2025).

Krugman, Paul (1990): A Europe-Wide Currency Makes No Economic Sense, Los Angeles Times, August 5, 1990. Available online at https://www.latimes.com/archives/la-xpm-1990-08-05-fi-453- story.html (accessed on July 3, 2025).

Maurer, R. (2023): The Divergence of Price Levels in the European Union, Intereconomics, 58(6), pp. 342–346.

Mundell, Robert (1961): A Theory of Optimum Currency Areas, American Economic Review, Vol. 51, No. 4, pp. 657–665. Available online at https://www.jstor.org/stable/1812792 (accessed on July 3, 2025).

Schüler, Yves S.; Hiebert, Paul P.; Peltonen, Tuomas A. (2020): Financial Cycles: Characterisation and Real-Time Measurement, Journal of International Money and Finance, Vol. 100, February 2020, 102082. Available online at https://www.sciencedirect.com/science/article/pii/S0261560619301597 (accessed on July 3, 2025).