Europe’s quiet stagflation risk

For much of the postwar era, macroeconomic policy rested on an intuition famously formalized by the Phillips curve: Economic slack, typically associated with high unemployment, and inflation tend to move in opposite directions. Weak growth cools prices; overheating pushes them up. Monetary policy can therefore stabilize one variable by leaning against the other.

Stagflation shatters that logic. Stagnation and inflation coexist, forcing policymakers into impossible choices. Tighten monetary policy and you crush already-weak activity. Ease it, and inflation hardens into something more permanent. There are no clean trade-offs, only losses, distributed unevenly and often in politically explosive ways. For central bankers, this is a nightmare scenario.

Historically, such episodes have been rare. They usually followed large negative supply shocks, none more emblematic than the oil crises of the 1970s.

A ghost that never quite left

The specter of stagflation briefly resurfaced after the Covid-19 pandemic. As economies reopened, broken supply chains collided with fractured labor markets and unprecedented fiscal and monetary stimulus. Inflation surged. Then Russia’s invasion of Ukraine caused a severe energy shock, which was especially hard on Europe due to its reliance on Russian gas.

For a moment, the parallels with the 1970s looked compelling. But they quickly faded. Energy prices retreated, growth recovered and inflation, after the sharpest tightening cycle in decades, was brought back under control. The scare receded.

However, by late 2025, the term stagflation had reappeared in headlines, mainly in the United States. Over a year into President Donald Trump’s second term, restrictive immigration policies, aggressive tariffs and renewed trade tensions are weighing on economic activity, while inflation stays stubbornly high.

The U.S. Federal Reserve insists stagflation is not its baseline scenario. Yet its actions suggest unease. After cutting rates three times between September and December 2025, the Fed, under pressure from the Trump administration, has clearly chosen to prioritize employment over inflation, even at the cost of greater exposure to stagflationary risks down the road. All this raises an uncomfortable question: Could Europe be next?

Inflation tamed, growth anemic

On inflation, Europe seems stable for now. The euro area has moved past the double-digit, energy-driven spikes of 2022-2023. Core inflation remains close to the central bank’s 2 percent target. But economic growth tells a different story.

Across institutions – the European Central Bank (ECB), the European Commission or the Organisation for Economic Co-operation and Development – the outlook converges on weak but positive expansion: growth rates of 1-1.4 percent in 2025-2026, followed by a slow, uneven recovery, assuming domestic demand does not falter.

Country-level data paints an even bleaker picture. Germany, once Europe’s industrial engine, has been experiencing near-zero growth for years. Structural weaknesses, high energy costs and underinvestment have turned stagnation into a feature, not a phase.

Europe is not stagflationary today. But it is not healthy either.

France, long praised for its social model, is paralyzed by fiscal gridlock: Debt is rising, reforms have stalled and growth is projected at barely 0.6 percent in 2025. In Italy, hit hard by President Trump’s tariffs, economic growth is expected to be a mere 0.5 percent. Spain stands out with growth of nearly 3 percent, but much of this is driven by massive public-sector hiring, not by a productivity renaissance.

Unemployment remains low in the eurozone, at roughly 6.4 percent. Europe is not stagflationary today. But it is not healthy either. The continent appears stuck in a low-growth, moderate-inflation equilibrium – stable on the surface, brittle underneath.

Structural challenges

Beneath the surface lies a set of forces with the scale and persistence to generate inflation over time: deep-rooted economic, social and political shifts that will make price stability harder to maintain over the long run.

Europe now operates in a permanently riskier world. Geopolitical shocks are no longer temporary; they are structural. Wars, sanctions and trade retaliation fragment the global economy and are creating cost pressures that do not unwind quickly. Defense spending is increasing sharply. Welfare systems, already under strain, are becoming more expensive.

Demographics compound the problem. Aging populations depress productivity and inflate pension and long-term care obligations. Public-debt trajectories worsen accordingly.

Without urgent investment, Europe risks accelerating deindustrialization – losing millions of industrial jobs and deepening its dependence on external powers, often autocratic ones. Digitalization and artificial intelligence add another layer of tension. AI promises productivity gains but also threatens to displace large parts of the workforce. Reskilling costs, labor-market frictions and transitional unemployment all carry inflationary potential. Yet these effects remain strikingly underestimated or ignored by policymakers and markets.

Then comes the green transition. Climate change is expensive, and so are the policies designed to fight it. Energy, housing, transport and industrial production costs are all likely to rise. Europe already operates with some of the world’s highest cost structures. Households are running out of buffers. Living costs are high, real wages have lagged and taxation, at record levels, is set to increase further in many countries.

The unconventional policy tools that once defined the Draghi era now seem firmly back in the drawer.

Meanwhile, excess liquidity continues to slosh through the system, a legacy of more than a decade of ultra-loose monetary policy. Near-zero interest rates and massive asset purchases had injected trillions of euros into the economy for nearly 15 years. Even after tightening, liquidity remains abundant. Asset prices, especially real estate, have soared, pushing up living costs while disproportionately enriching owners of assets.

Overlay this with Europe’s growing bureaucracy and regulatory density, and the growth outlook deteriorates further. Investment is weak. Entrepreneurial risk-taking is constrained. Competitiveness is declining. The continent continues to miss opportunities in major global technological waves, including AI.

Regulatory rigidity, capital outflows, stagnant incomes, unfavorable demographics, as well as political fragmentation and waning global influence, define Europe’s socioeconomic landscape. Mario Draghi’s warning of a “slow agony” if nothing changes was not hyperbole. Structural reforms are advancing at a glacial pace. Little suggests a decisive shift.

No return to the past

In the current, chronically mediocre economic environment, one might expect the ECB to redeploy its ultra-loose monetary arsenal. This time, it is not.

In the past, it did so for far less. In 2019, for example, just before Mario Draghi handed over the ECB presidency to Christine Lagarde, the ECB launched another large round of quantitative easing to support an economy growing at around 1.6 percent. There was no acute crisis, only another slowdown. Policy rates stood at historic lows, with the deposit rate at -0.5 percent and the main refinancing rate at 0 percent.

After the post-pandemic tightening cycle – when the main refinancing rate peaked at 4.5 percent in September 2023 – the ECB cut rates eight times between mid-2024 and mid-2025, until inflation returned to target. Since then it has paused, keeping the deposit rate at 2.0 percent. “We are in this sort of wait-and-watch or wait-and-see mode,” President Lagarde said in October 2025.

More importantly, the ECB seems to rule out a return to old habits: negative rates, forward guidance, targeted bank lending, credit easing and systematic sovereign-bond purchases. It is still gradually unwinding its remaining bond holdings as part of “quantitative normalization,” and its balance sheet is shrinking rapidly as a result. But no new quantitative easing is in sight. The unconventional policy tools that once defined the Draghi era now seem firmly back in the drawer. Is this really just a wait-and-see pause, or is it a strategic retreat?

At a 2025 Frankfurt conference, executive board member Isabel Schnabel stated that there would be no “return to the past,” neither regarding the size nor the composition of the ECB’s balance sheet.

Months earlier, at Stanford University, she evoked, with striking openness, the unintended consequences of prolonged monetary expansion: market dysfunction, rising wealth inequality, financial instability and reputational damage to central banks themselves. That such warnings come from someone who once oversaw the ECB’s most extraordinary bond-buying programs is remarkable.

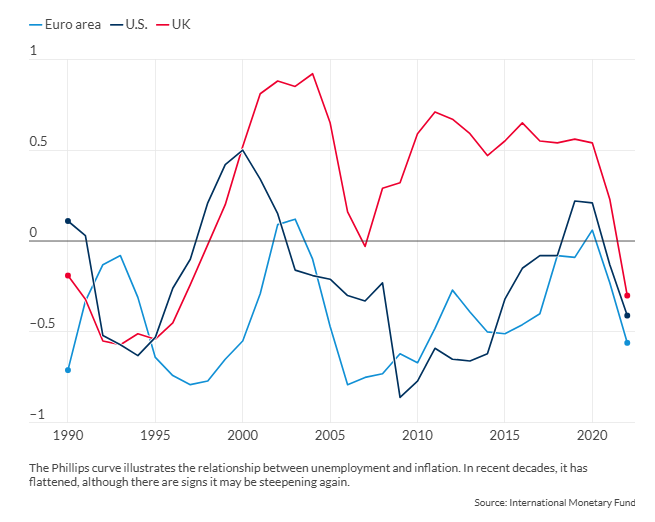

The flat Phillips curve

Years of monetary steroids have left Europe exposed to both inflation and stagnation. Interestingly, the ECB has avoided using the term stagflation in its recent communications. Instead, it reframes the debate around the breakdown of the traditional link between inflation and economic slack.

Once a favored guide for policymakers – and still one that many central bankers remain attached to – the Phillips curve has, over time, become increasingly hard to verify empirically. Over recent decades, the link between economic activity and inflation has shifted, flattened or even disappeared at times. After the pandemic, the curve briefly steepened before flattening again.

Facts & figures: Phillips curve: 10-year rolling correlation of the unemployment rate and CPI inflation

As Ms. Schnabel recalls, the slope of the Phillips curve determines the “sacrifice ratio”: how much output and employment must be destroyed to control inflation. While a steep curve allows decisive central-bank action at relatively low cost, a flat curve makes policy blunt and costly, with ever-larger interventions yielding diminishing returns.

By focusing on a flat Phillips curve rather than explicitly invoking stagflation risks, the ECB signals restraint. “Keeping a steady hand in an uncertain world,” as Ms. Schnabel put it, means holding rates close to neutral rather than rushing to ease at the first sign of weakness.

Two words now dominate the ECB’s vocabulary: credibility and independence. In recent speeches, Ms. Lagarde and her lieutenants have made it clear that the institution is steering back toward its original mission: price stability. After more than a decade of crisis-driven improvisation, during which the monetary policy mandate was stretched beyond its limits, the line is being redrawn. Keeping heavily indebted states afloat is no longer framed as the central bank’s responsibility.

This is not austerity by stealth. It is a redefinition of what the ECB believes it can, and should, be held accountable for.

Scenarios

Unlikely: A near-term slide into stagflation

Current eurozone conditions, however sluggish, are incompatible with an imminent bout of textbook stagflation.

Yet the system is fragile enough that a sudden adverse shock – a badly timed energy disruption, a geopolitical escalation or a policy error – could tip stagnation into stagflation.

Likely: Pulling back the safety net

All signs point to an ECB determined to reclaim its independence. If its current strategy of retreat hardens into a lasting trend, the consequences will be profound. No more systematic sovereign debt buying. No more monetary financing. No inflationary debt relief. Debt will matter again. Irresponsible governments can no longer rely on a powerful central bank pledging to do “whatever it takes” whenever they fail.

Such a future will be harsh. Recessions will come. Adjustment will hurt. And yet a return to fiscal discipline may be Europe’s best chance: the only credible path toward a healthier economy, and the most effective defense against the specter of stagflation.

This report was originally published here: https://www.gisreportsonline.com/r/europe-stagflation-risk/