Iran war squeezes critical supplies and global alliances

Ever since the failure to reach an agreement during high-level United States-Iran talks in Islamabad, Pakistan, in early April, there has been ongoing volatility in global commodities and financial markets. Although a ceasefire, in place since April 8, has been extended several times, a lasting peace agreement remains elusive at time of writing. Pakistan continues to facilitate indirect negotiations, with recent reports of tentative progress, yet core disagreements regarding Iran’s nuclear program, control of the Strait of Hormuz and sanctions persist.

While media attention has focused intensely on the surge in crude oil prices, the war’s longer-term consequences are far more structural and insidious. At its core, the conflict has weaponized international financial and energy markets. Its most enduring legacy is likely to be the permanent reshaping of global supply chains, with nations prioritizing economic security over efficiency.

The U.S.-Iran war will be remembered not for its military tactics or the terms of the ceasefire, but for its role as a catalyst in restructuring the global economy.

Hidden shockwaves

The most immediate, long-term economic danger lies not in fuel prices themselves but in rising food costs and disruptions to the production of advanced technology. The blockades of container vessels and the destruction of energy infrastructure in the Persian Gulf have severed supply lines for materials that modern industry and agriculture take for granted.

The Middle East controls nearly half of the global sulfur market and a significant portion of critical fertilizer components such as ammonia and phosphate. In 2024, around 30 percent of the global fertilizer trade passed through the Strait of Hormuz, which connects the Gulf to export markets worldwide. The vital waterway also carried approximately 20 percent of liquefied natural gas (LNG), a crucial feedstock for fertilizer production, and 27 percent of the oil traded globally.

Fertilizer supply chain vulnerabilities

Fertilizer markets, which depend heavily on ammonia, urea and natural gas from the Gulf, are facing major long-term risks due to disruptions in the Strait of Hormuz. The blockades caused prices to soar by 30-40 percent in March, while nitrogen costs have doubled compared with 2024 levels. As of May 2026, prices remain elevated, with the global fertilizer index projected to rise over 30 percent for the year amid persistent supply risks and rerouting challenges.

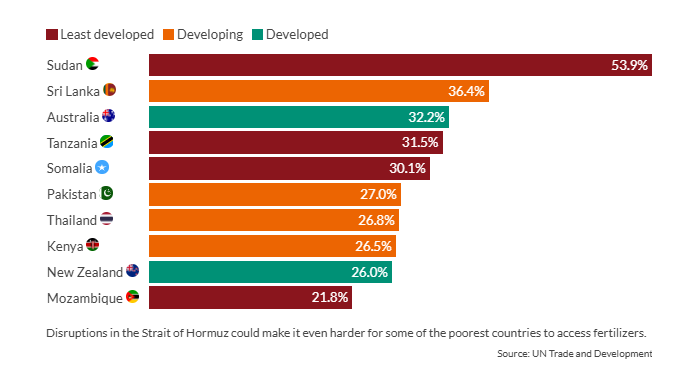

Asia, which receives 35 percent of the Gulf’s urea and is now in the spring planting season, faces a risk of reduced yields in rice, wheat and maize. The International Food Policy Research Institute has warned that if the situation is not resolved, it could lead to food security crises in Africa and South Asia.

Brazil and Argentina, two major agricultural exporters, are facing significant challenges as input prices have surged by 30 percent, without corresponding increases in crop prices. These pressures are squeezing profit margins and are likely to reduce global grain output by 5-10 percent by 2027. The chronic shortages may lead to higher costs, reminiscent of the energy price shocks that followed the 2022 war in Ukraine. Adding to the strain, the war has caused considerable damage to Qatar’s Ras Laffan LNG and fertilizer hubs, which will require extensive repairs that could take several months or even years.

Facts & figures: Share of fertilizers imported by sea from the Persian Gulf region, 2024

Sulfur shortages and critical minerals processing

Sulfur, a byproduct of petroleum and natural gas, is essential for producing sulfuric acid, which is used to leach metals such as copper, nickel, uranium and rare earth elements. These metals are crucial for manufacturing electric vehicle batteries, renewable energy technologies and defense products. Gulf states typically provide 45 percent of the seaborne sulfur trade through the Strait of Hormuz. However, Iran’s blockade has caused a 30 percent price spike by halting half of the global supply of sulfur, creating bottlenecks in mineral extraction.

Sulfur shortages are already leading to 20-30 percent output reductions for critical mineral miners. The shortages are driving up prices of these essential minerals and delaying green transition initiatives. Projections also show a 50 percent rise in phosphate prices, which compounds the sulfur woes.

China’s dominance in this sector is likely to further strengthen its leverage over Western efforts to restart critical minerals initiatives amid newly elevated costs. Without a steady supply of sulfur, farmers from Europe to Southeast Asia face prohibitively high fertilizer costs or outright shortages during the peak planting period. Lower crop yields and sustained food inflation will follow, hitting developing countries hardest. Such shocks could spark social unrest on the scale of the Arab Spring, which was itself triggered by surges in food prices.

Helium constraints on semiconductors and tech

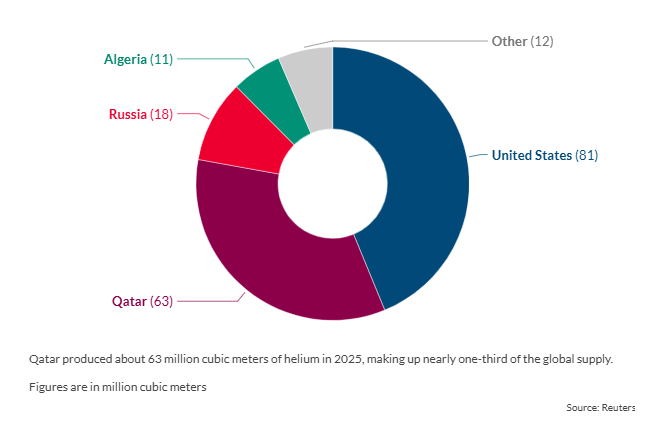

The conflict’s supply shock could also amplify U.S.-China tech rivalry as disrupted gas production slows semiconductor scaling on both sides. Helium, derived from LNG processing as an inert gas critical to creating the flawless crystal environments required for semiconductor lithography, is caught in the crossfire. Qatar, a key producer in the region, accounts for about a third of the global helium supply, with some estimates suggesting it provides up to 40 percent of global demand.

Helium prices, which previously hovered around $300 per thousand cubic feet, have surged since the onset of the war, reaching $900 per thousand cubic feet. The sharp increase has already idled semiconductor fabrication plants (fabs) producing chips for artificial intelligence and electric vehicles, as supplies of ultra-cold liquid helium for cooling have been disrupted.

Facts & figures: Helium production, 2025

Both Taiwan and South Korea rely on helium gas imports from the Middle East, putting them at risk of 10-20 percent production dips. These disruptions risk delaying the global semiconductor recovery amid U.S. export restrictions. Moreover, as countries – particularly the U.S., which currently holds only 44 percent of global fab capacity – rebuild their semiconductor manufacturing bases, prolonged chip shortages are projected to add $50-100 billion to global production costs between 2027 and 2030, further entrenching supply chain fragility.

In an era defined by an AI arms race and demand for advanced computing, the current helium shortage threatens to halt production lines. Unlike oil, helium has no strategic reserve; once the supply chain runs dry, semiconductor fabs simply come to a halt. The impact is disproportionately large. Even though helium is a low-volume commodity, a shortage can cause massive disruption to high-value industries like semiconductors. The Iran war has therefore not only shocked traditional markets but also jeopardized the development of the digital economy.

Fracturing of alliances and globalization

For the West, specifically the NATO alliance, the war has acted less as a unifier and more as a divider. The Trump administration’s actions have met open defiance from key European allies such as Germany and Spain. This fracturing contributes to a more volatile, multipolar environment in which middle powers no longer perceive their interests as aligning with those of dominant global players.

Perhaps the most profound long-term economic effect of the Iran war is the psychological break with seamless supply-chain globalization. While the Covid-19 pandemic taught businesses about the fragility of medical supply chains, and the Ukraine war highlighted energy dependency, the Iran conflict is revealing the vulnerability of basic industrial intermediate products. The war risks driving a permanent increase in protectionism and onshoring. Countries will not be merely seeking to diversify suppliers of critical inputs; they will look to rebuild domestic capacity for refining, fertilizer production and even helium recycling.

Simultaneously, the new era of strategic autonomy requires large capital investments as governments subsidize domestic microchip fabs, chemical plants and renewable energy storage.

The global economy is therefore likely entering a world of permanently higher interest rates. This will be largely due to governments borrowing extensively to establish more localized supply chains for essential resources like energy, sulfur, fertilizer, helium and other critical inputs that often come as byproducts of fossil fuel extraction.

Long-term investments can be expected to pivot significantly toward renewables and nuclear energy, not only for environmental reasons, but also for national security. The logic is simple: Solar panels and wind farms cannot be blockaded by a navy or shut down by mines in a geographic chokepoint.

Realigning economic partnerships

The economic consequences are particularly severe for East and South Asia, regions that rely heavily on the Gulf for most of their energy and fertilizers. For industrial powerhouses such as China, India, Japan and South Korea, the war presents an impossible trade-off. These countries need the affordable energy and raw materials from the Middle East, but they are constrained by the military dominance of the U.S. and the disruptive actions of the Iranian regime.

These Asian nations are likely to adopt a hedging strategy going forward. On the one hand, they may deepen economic ties with the Gulf states and Iran to secure long-term energy contracts. On the other hand, the ongoing tensions and rivalries between the U.S. and Iran will drive them to seek overland alternatives for energy supplies.

China’s Belt and Road Initiative, particularly its investments in Central Asian pipelines and ports in Pakistan, is likely to gain increased strategic importance. This development aims to circumvent the maritime chokepoints in the Gulf and other infrastructural vulnerabilities.

There may also be a geopolitical divergence in commodity markets. The disruption of sulfur and helium supplies from the Middle East will push Asia to establish closer extraction and processing partnerships with Russia for sulfur and with North America for helium, despite the higher logistical costs involved.

These strategies will further fragment global commodity markets, resulting in them being driven more by geopolitical factors than by traditional considerations of supply chain costs and efficiencies. For example, this could result in a Western bloc focused on U.S. energy independence and Canadian helium, and an Eastern bloc depending on a wide range of abundant Russian resources and more secure overland routes financed by China.

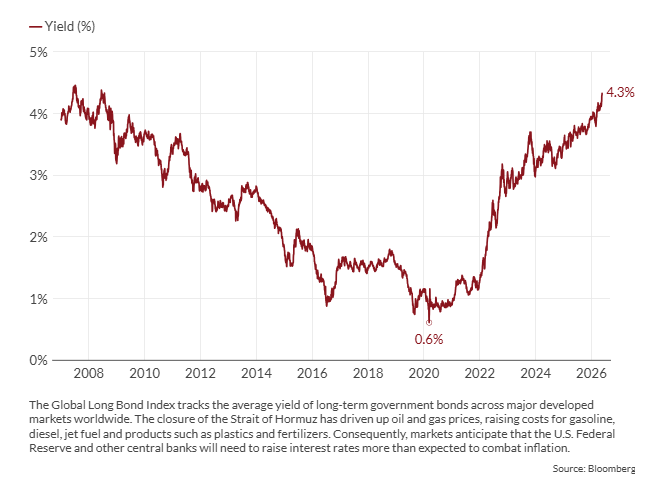

Facts & figures: Global Long Bond Index yield

Inflationary legacy and stagflation risks

The Iran war is causing a supply-side shock to a global economy already struggling with post-pandemic inflation and monetary tightening. The disruption of sulfur, helium and fertilizers will not be resolved quickly, as rebuilding gas plants is a lengthy process. As a result, lingering price pressures on food and electronics are expected.

Central banks, having failed to anticipate the sustained impact of this economic shock, may be compelled to maintain high interest rates even as unemployment rises. Such policy missteps have historically triggered severe recessions. The U.S.-Iran war will be remembered not for its military tactics or the terms of the ceasefire, but for its role as a catalyst in restructuring the global economy.

As the world shifts from a model of efficiency to one of resilience, the cost of living will rise, the pace of technological growth may slow, and the map of geopolitical friends and enemies will be redrawn along lines of resource dependence. The era of the globalized village is giving way to a series of fortified, self-sufficient silos.

Scenarios

Most likely: Fragmentation, stagflation and strategic hedging

A prolonged conflict could cut the Gulf region’s foreign investment in half, jeopardizing its status as a safe haven for energy supplies and byproducts. This would lead to a surge in the need for strategic autonomy. As the European Union grapples with stagflation, it will ramp up its industrial policies. Meanwhile, landlocked Central Asian countries will expand their diplomatic efforts to secure large-scale infrastructure deals with Europe and China to create major land corridors for transporting oil, gas and other essential resources.

A protracted period of economic stagnation is defined by ongoing, low-grade disruptions. During this time, fertilizer prices would settle at 40 percent above pre-war levels, while both Europe and India ramp up domestic sulfur recycling and phosphate mining efforts. However, food inflation remains stubbornly entrenched, persisting for three to five years. Chronic helium shortages would cause semiconductor manufacturers to operate at only 85 percent capacity, delaying next-generation chip production by 12-18 months.

Geoeconomically, the U.S. and China accelerate their decoupling. Beijing deepens overland energy corridors through Central Asia, while Washington solidifies a Western commodities bloc with Canada, Australia and parts of Latin America.

Europe pivots toward North African hydrogen and LNG while reducing reliance on the gulf. Russia also emerges as a tactical winner – selling oil and sulfur to India and China at a premium. Asia generally boosts U.S. and Australian LNG imports and other strategic input supply deals. China takes advantage of its processing monopolies, exporting refined minerals at premium prices and further entrenching dependencies in the Global Majority. No major power achieves energy independence, but all accept permanently higher costs for security.

Less likely: Coordinated rebalancing and accelerated green transition

An eventual diplomatic breakthrough – brokered by a group of Muslim states friendly to both the U.S. and Iran – leads to a new Strait of Hormuz security compact within 18 months. As a result, Iran accepts strict export caps in exchange for sanctions relief. Gulf helium and sulfur export flows normalize as Qatar and Saudi Arabia guarantee neutral shipping lanes.

Even so, the legacy of the war triggers a “green silver lining”: Governments worldwide, having experienced fossil fuel weaponization, pour trillions of dollars into nuclear, solar and large-scale energy storage. Fertilizer shifts to green ammonia produced from renewable energy, bypassing dependence on natural gas. Semiconductor firms invest heavily in helium recycling and alternative cooling technologies.

Geopolitically, a G20-led critical minerals treaty emerges. This scenario leads to unprecedented cooperation between the U.S. and China, possible only if a severe global recession forces all parties to prioritize economic survival over rivalry.

Least likely: Open conflict escalation and full de-globalization

A second phase of military action, which includes strikes on Iranian nuclear facilities and infrastructure, prompts Tehran to retaliate by targeting oil fields in the Gulf region. Helium supply from Qatar halts completely, causing a six-month disruption to global semiconductor production. Sulfur shortages cause a 50 percent decrease in global fertilizer output, triggering famine in countries such as Egypt, Bangladesh and Nigeria.

The U.S. Navy aggressively enforces a blockade of international ships originating in Iranian ports that pass through the Strait of Hormuz. This action draws in China, as it seeks to safeguard its energy supplies, leading to an escalation of proxy conflicts in other regions, such as the South China Sea.