Irrational Exuberance

Yes, the rally in the “Magnificent Seven stocks” – the “Mag 7” – has been impressive. No, the rally is not over yet. Yes, this is a bubble – the “AI-bubble”. And yes, the AI-bubble will end badly for many, many people. The only question is when. The phrase “this time is different” was, of course, made famous by Carmen Reinhart’s and Kenneth Rogoff’s book by the same name. However, the sentiment is hardly new or unique – the concept has been around for years. The eminent British financier Sir John Templeton even went so far as to remark that “this time is different” are the “four most dangerous words in investing.”

Reinhart and Rogoff took some liberties with their analysis, which undermines some of their findings. However, the thesis that fundamentals matter, and, consequently, periods of market mania are largely similar, even if the vocal hordes claim, “the rules have changed.”

But where are we in the AI-bubble? How much longer will the bubble persist? Is there money to be made by going long companies like Nvidia (NASDAQ: NVDA), Apple (NASDAQ: AAPL), and Tesla (NASDAQ: TSLA)?

To answer these questions, consider the June 18th article from Bloomberg titled, “BofA Poll Shows Investors Primed to Fuel Stock Rally with Cash.” The article discusses findings from a recent survey conducted by Bank of America (NYSE: BAC).1 Bloomberg’s summary is as follows:

As US equities make new highs, global investors are likely to keep pumping money into the market, according to a Bank of America survey. The poll — canvassing 206 participants with $640 billion in assets under management — showed investors remained the most bullish since November 2021, while long bets on the so-called Magnificent Seven technology behemoths now stand at 69% — among the most crowded trades in history, the survey said.

One of Joseph Kennedy’s most famous quotes – a statement he reportedly made just prior to October 29, 1929 – is: “If shoeshine boys are giving stock tips, then it’s time to

get out of the market.” The story is that Joe was having his shoes shined, and the kid shining them offered him some stock tips. Joe purportedly went back to his office, liquidated all his equity holdings, and shorted the market. I don’t know if this really happened, but it’s a good story.

Whether Joe made a fortune using the shoeshine kid as a contra-indicator isn’t the point. The point is that, historically, retail investors are consistently wrong when it comes to timing the market, usually with negative, if not outright tragic, results. The contention that popular sentiment among retail investors is a valid contrarian indicator has, in fact, been empirically tested and shown to be accurate, at least for certain time periods.

“Odd-lot theory” – the strategy of trading contra to what retail investors are doing – is intimately related to the use and dissemination of information (aka, “information asymmetry”). With the introduction of the internet, the situation changed dramatically regarding the accessibility of information. Concurrently, regulators have established new rules regarding the use and proper dissemination of information and sought to more heavily enforce those already on the books, especially regarding insider trading.

Given the changes, what should investors make of the behavior exhibited by odd-lots? In fact, the basic question boils down to a binary decision regarding how to react to news like the BAC survey found: Do you want to run with the herd, or interpret their behavior as a contra-indicator?

Many years ago, I worked with a brilliant portfolio manager, Darrell W., who had a gift for momentum trading. Having worked with Darrell, I have no doubt that there are individuals out there who have their fingers on the pulse of markets and can act accordingly. If you happen to be one of those people – or are privileged to work with one – you’re very fortunate, and you will probably make a lot of money following their lead.

The problem is that there are very, very few people in the world who are as talented as Darrell. In fact, I haven’t met more than a half-dozen during the more than twenty-five years I’ve worked in finance. For most of us, the only way we can proceed without taking on an unacceptable level of risk is to follow the “classic” approach of value investing and portfolio diversification that was formulated, championed and refined by giants like Harry Markowitz, Benjamin Graham, Mario Gabelli, Warren Buffet, and Peter Lynch.

Most investors simply cannot afford to ride the waves of rapidly changing investor sentiment. We must approach investing in a more methodical, traditional manner: we analyze; we compare; we research. We set out entry and exit points according to valuations. We try to sell losers before losses are too large and cash in winners after we’ve made a reputable return. We aim to simply get on base and try to resist the temptation to swing for the fences. So, what does Joe Kennedy have to do with the AI-bubble. The answer is both “everything and nothing.”

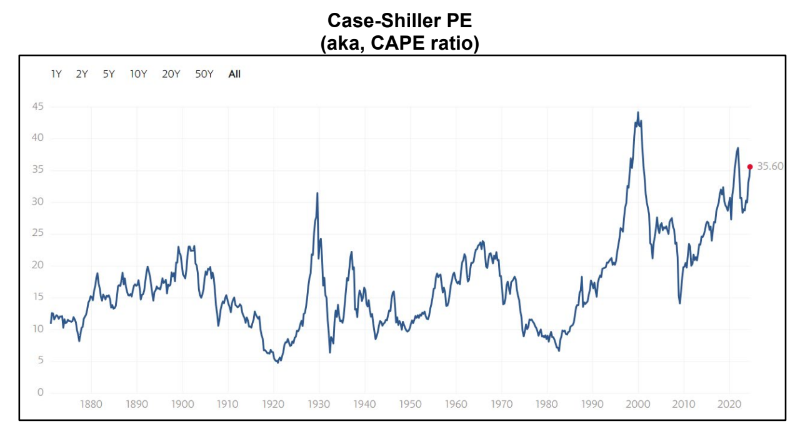

The CAPE ratio is one of the better metrics for measuring just how loopy the market has gotten. And, as is clear from the graph, deviations above 20 (approximately) have

historically been followed by rapid decreases. The S&P 500 is currently trading at 35.60. Not only is this dramatically higher than history suggests is reasonable, but it is also

greater than at any other time in history, save for the levels reached during the dot-com bubble.

As the CAPE ratio demonstrates, the S&P 500 is dangerously overextended. And you don’t have to dig very deep to see that the Mag 7 stocks are as well. The Mag 7 have an

average forward p/e ratio of 44 1⁄2, driven largely by NVDA, at 74, and TSLA, at 78. The entire S&P 500 is trading with a forward p/e of 23.

A surfeit of commentators have noted how much weight the Mag 7 stocks wield, for good reason: those seven stocks constitute about 30% of the S&P 500’s performance, and just over 40% of the NASDAQ-100. To call the S&P 500 “top-heavy” is a colossal understatement – sort of like saying that being trampled by a hippopotamus is “a bummer.”

The internet changed the world, and there is every reason to believe that AI will also have a strikingly profound, lasting impact. However, the “irrational exuberance” that captivated investors from 1996-2000 resulted in a precipitous decline in stocks, as well as a number of bankruptcies. Once again, Mr. Market punished those who ignored fundamentals.

As I previously mentioned, unlike my former colleague (and idol) Darrell, I lack that super-human gift of having an innate “feel” for the markets and being able to trade accordingly. One result is that I tend to exit trades early – inevitably leading me to leave quite a lot of money on the table.

Because of my current job in investment banking, I no longer actively trade. But, having traded for many years, I know how easy and annoying it is easy to comment from the sidelines – especially with the benefit of hindsight. As such, I won’t speculate about what I would have done over the previous months… But I can unambiguously say that, were I actively trading this market, I would have very little exposure to the Mag 7 right now.

Of course, if I had owned and had sold, I would have missed the recent highs made by AAPL, NVDA, and others – just as I would (and will) not participate in any future upside

those companies may realize over the coming weeks. But I would have slept better.

There are certainly differences between the dot-com bubble and the current market environment. But the similarities are too pronounced to ignore. Furthermore, there is no

reason to think that this latest bout of investor fervor will end any differently than previous episodes have. The only question is when.

The BAC survey is a telling indicator that the party may be coming to a close – no doubt, the proverbial shoeshine boys are handing out stock tips left and right. A crash is not necessarily imminent – there still appears to be enough momentum to keep the rally going a little while longer, especially given the level of share buybacks for S&P 500 companies, which should also provide some price support. But I will be surprised if the reckoning doesn’t begin shortly after Wall Streeters return from the Hamptons, if not sooner. Regardless, the next President, whoever he is, will likely enter office amidst market turmoil.

Of course, “true believers” – those investors who choose to highlight, in one way or another, growth expectations, and tend to ignore other metrics – will point out that the market rally could very well continue. As much as I disagree with the true-believer position, there is a case to be made that stocks will continue to rise.

Money is flowing into mega-cap equities as investors scramble to take part in the rally. And, due to the notable lack of attractive alternatives – State Street’s SPDR® Portfolio Europe ETF is only up 8.3% YTD, and 3.3% in the most recent quarter, to provide but one example – stocks may well continue to catch a bid.

Ultimately, individuals must evaluate investment options based on their own situations. While there may be a reasonable case to hold winners, specifically the Mag 7 companies, a little longer, it is difficult to imagine a convincing argument for initiating a new position in one or more of those equities.

Given how overbought the Mag 7 names are, and how much irrational exuberance seems to be floating around AI, now is not the time to go all-in, except for active short-term traders who are comfortable with elevated risk and nimble enough to roll with the slings and arrows of heightened volatility.

Regardless of your investment horizon, in this market investors should pay close attention to the adage “caveat emptor” and comport themselves accordingly.

________________________

ABOUT THE AUTHOR:

Bill Waite is the Head of Global Banking at BMI Capital International LLC, a New York City based FINRA/SIPC registered broker-dealer. Bill heads BMI’s valuation practice and advises companies that are seeking to list on the NASDAQ, NYSE, or OTC markets. Bill is a published author, avid traveler, and exceptionally mediocre fisherman.

________________________

DISCLOSURES:

I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my, and only my, opinions. I did not receive any compensation for writing this article or expressing the views/positions contained herein. I have no business relationship with any company whose stock is mentioned in this article. Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Views or opinions expressed herein may not reflect those of BMI Capital International LLC, its management, subsidiaries or affiliates.

1 https://www.bloomberg.com/news/articles/2024-06-18/stocks-bofa-poll-shows-investors-primed-to-fuel-rally-with-cash?cmpid=BBD061824_MKT&utm_medium=email&utm_source=newsletter&utm_term=240618&utm_campaign=markets