The evils of financial illiteracy

Given the state of the world today, one could not be blamed for thinking that there are more pressing matters to worry about than some people’s inability to grasp the concept of compound interest. Inflation, economic uncertainty, heightened social friction and new technological (and possibly existential) threats like Artificial Intelligence all seem more urgent.

However, there is an argument to be made that most, if not all, of these problems and dangers at least partially stem from the scourge that is financial illiteracy.

Ignorance is bliss?

According to a recent Eurobarometer survey published in July 2023, “only 18 percent of European Union citizens have a high level of financial literacy, 64 percent – a medium level, and the remaining 18 percent – a low level. There are, however, wide differences across member states. In only four Member States, more than 25 percent of people score highly in financial literacy (the Netherlands, Sweden, Denmark and Slovenia).” The gap was even more pronounced among certain demographic groups, namely “women, younger people, people with lower income and with lower levels of general education who tend to be on average less financially literate than other groups.”

These figures may not seem alarming at first – until one dissects what the researchers defined as a “high level of financial literacy.” When assessing financial knowledge, the participants were deemed “top of the class” if they could answer four out of five basic questions correctly, with questions ranging from “(do you) understand that an investment with a higher return is likely to be more risky” to “(do you) understand the link between interest rates and bond prices.” Only 20 percent of those surveyed in total got the second one right.

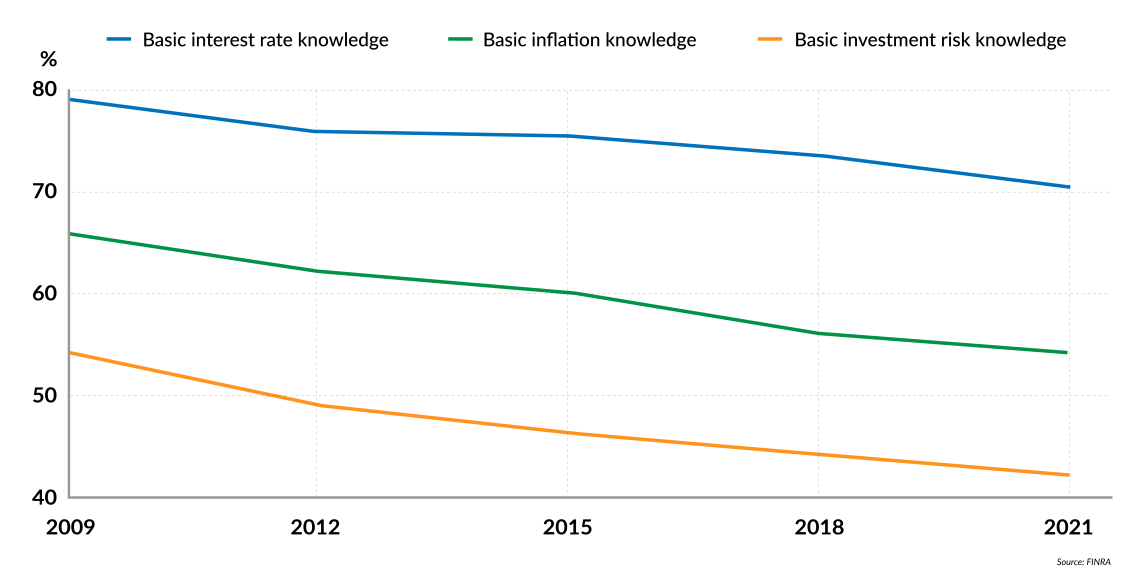

In the United States, the level of financial literacy is even lower. Research by the Financial Industry Regulatory Authority (FINRA) showed that approximately two-thirds of Americans cannot pass a basic test with questions on simple concepts like inflation and interest, similar to those posed by Eurobarometer.

Facts & figures

Financial literacy levels in the United States

As might be expected, this lack of understanding of finance, basic economic concepts and even elementary math has a very real and direct impact on financially illiterate individuals and their families. As the latest National Financial Educators Council (NFEC) report highlighted in April, the average American lost $1,819 to personal financial errors last year. The main traps for those on the lower end of financial literacy are credit card interest rates and fees, which cost consumers $120 billion in 2022.

With interest rates higher now, these mistakes have become costlier and costlier. Overdraft fees are another popular black hole for a lot of people’s money: “Americans spend $17 billion a year on overdraft and non-sufficient funds (NSF) fees,” according to the Consumer Financial Protection Bureau (CFPB).

Far-reaching implications

The damage that financial illiteracy can inflict on those who suffer from it is obvious. A lifetime of financial woes, struggling to make ends meet and living from paycheck to paycheck is the most common scenario, but it can get a lot worse. With no rainy-day funds to act as a buffer in cases of unforeseen expenses, getting laid off or even having a medical emergency can easily lead to spiraling debt. Descent into real poverty is a common outcome for many people in such positions, which in turn often leads to social marginalization, generational disadvantage and social immobility. As a result, the next generation is often denied a quality education and the opportunity to acquire financial literacy for themselves, which feeds into a vicious cycle.

The consequences, however, do not affect the individual and their families alone. Financial illiteracy, especially when it is this prevalent in any society, effectively kneecaps the democratic system itself and virtually guarantees that real growth and prosperity will forever remain elusive.

Put simply, if the majority of voters cannot decipher and assess basic metrics and understand fundamental concepts like interest rates, consumer price inflation figures, government budgets, money creation and monetary policy decisions and interventions, how are they supposed to make an informed, rational choice come election time?

In fact, as a 2020 survey showed, the majority of Americans do not understand how banks work: “38 percent of respondents believed that banks had to have the exact amount of customer deposits in their reserves at all times.” Most of those who had heard of fractional reserve banking had no idea about the true extent of it.

If the body politic as a whole has little to no grasp over even the simplest principles of money creation and fiat money in general, what is to stop any voter from being lured in by populist agendas and “free lunch” promises by politicians? Under these conditions, ideas based on the lowest common denominator, instant gratification and low time preference are bound to emerge victorious every time.

Voters are left defenseless. In this context, it is not surprising that misguided concepts like Modern Monetary Theory and Universal Basic Income are gaining traction. In a world where, until recently, negative interest rates were the norm without any public resistance or at least apprehension, anything goes.

As for the leaders themselves, their motives for peddling easy solutions to complex problems are clear (that is, populist promises get the popular vote), but not much else about their reasoning is. It could be that political and institutional leaders fully realize and eagerly exploit this knowledge differential and take advantage of the public’s lack of understanding to advance their own interests.

This opinion was originally published here: https://www.gisreportsonline.com/r/financial-illiteracy/