China’s plan to challenge global leadership

As the North Atlantic political sphere spent the last few years focused on elections in Europe and the United States, as well as Russia’s war on Ukraine, China has made a remarkable resurgence. After displaying significant vulnerabilities during the Covid-19 pandemic and its immediate aftermath, the country rebounded.

While it currently faces major economic and trade challenges and the resilience of its recovery is anything but certain, Beijing has strengthened its position on the world stage through strategic international relations, deepened economic ties and engineered a distinctive approach to artificial intelligence leadership.

The pandemic exposed significant weaknesses in China’s economic and social fabric. The country’s erstwhile economic growth of 6 percent plummeted to 2.2 percent in 2020 as the government’s zero-COVID policy hindered consumer demand, production, investment and international trade. The collapse in consumption was especially devastating to growth.

CCP plan for growth

The Chinese Communist Party’s (CCP) stringent pandemic management, in place in 2021 and most of 2022, further complicated the recovery. Any community with an infected individual was classified as a high-risk area and inhabitants were forbidden to go out. These measures, while initially effective in controlling the virus, severely hurt economic activities, particularly for small and microenterprises. The sudden policy reversal in November 2022 to laissez-faire led to a peak in infections and another sharp decline in economic activity.

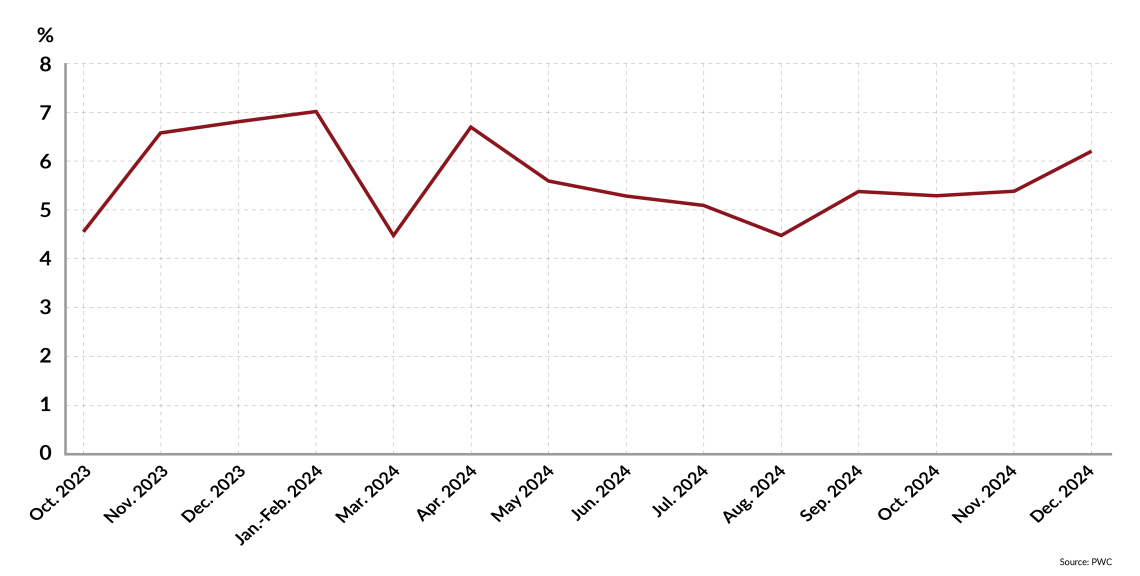

Facts & figures: Industrial output in China

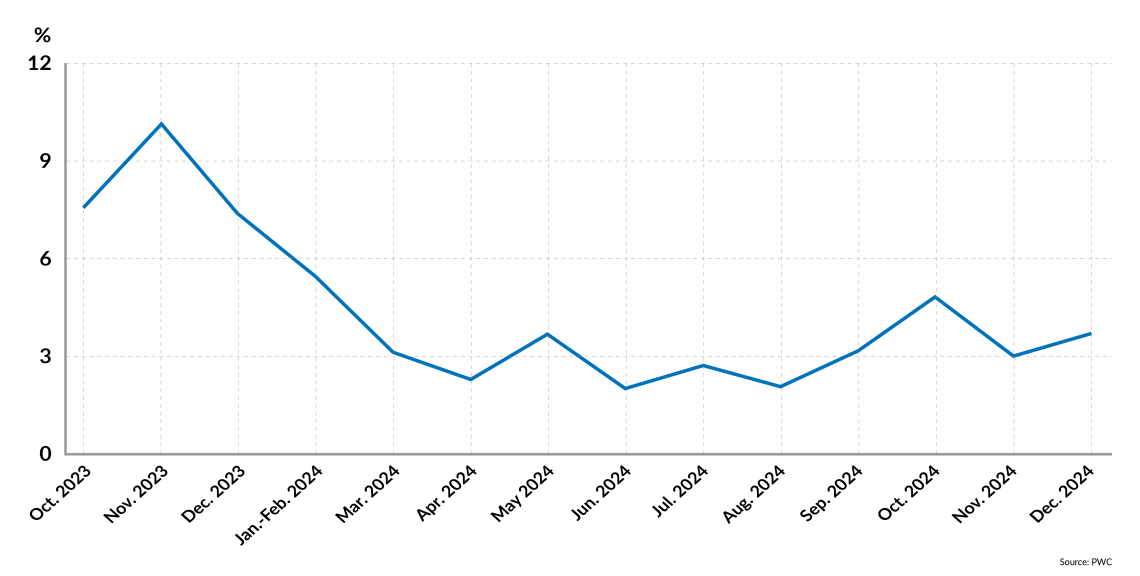

However, 2024 marked a decisive turning point. China’s gross domestic product (GDP) expanded by 5.4 percent in the final quarter, taking full-year growth to 5 percent, meeting the official target. This recovery has been driven in part by growth in manufacturing and exports, with the former rising 6.2 percent annually in the final quarter of 2024, up from 5 percent in the third quarter. Yet at the same time, retail sales failed to keep pace with production rises, averaging just above 3 percent for most of last year. As such, the Chinese economy remains at the mercy of export growth. Net exports contributed 30 percent to GDP growth in 2024, their highest share since 1997, producing a record trade surplus of nearly $1 trillion.

Government stabilization efforts launched in late 2023 paid dividends last year, and in the first quarter of this year, GDP again rose by 5.4 percent. Reforms, several rounds of fiscal stimulus to encourage consumption and innovation-driven measures bolstered domestic confidence. The real estate sector, which had long been a drag on growth, showed tentative signs of recovery following key policy interventions, including adjustments to housing purchase restrictions and reductions in mortgage interest rates. To be sure, the value of new home sales was down over 20 percent annually in June, following a decline in May.

Facts & figures: Retail sales in China

Thus, caution is warranted when examining Chinese economic data, which often suggests a greater alignment with CCP politics than with empirical reality. However, if additional stimulus is introduced and export growth can be sustained – American trade policy and corporates moving manufacturing from China to other countries amid derisking make that uncertain – the economic indicators may stabilize, signaling a recovery.

Bolstering international relations and economic ties

Last year, President Xi Jinping attended major domestic and overseas events, facilitating talks with global leaders to converge interests as China sought to strengthen its global position. China’s concept of building what it calls “communities with a shared future” gained traction: New partnerships were established with Brazil and Serbia, and an “all-weather China-Africa community with a shared future for the new era” was announced. On the global governance front, since its launch in 2022, 82 countries have joined the so-called Group of Friends of the Global Development Initiative, while over 100 countries have voiced support for the Chinese-led Global Security Initiative. Both aim to position Beijing at the center of the Global Majority.

President Xi’s Belt and Road Initiative (BRI) recorded over $70 billion in construction contracts and $5 billion in investments last year, setting a new peak for the program. Since its inception in 2013, the BRI has facilitated $1.18 trillion in funding worldwide, primarily through loans from Chinese banks and development institutions directed toward infrastructure projects. Last year, Middle Eastern countries were the biggest recipients of BRI investment and lending at $39 billion, followed by Africa at $29.2 billion and Southeast Asia at $25.1 billion.

The number of foreign companies investing or setting up operations in China also rebounded with growth of nearly 10 percent last year. In contrast, the total value of foreign direct investment fell by double digits. In November 2024, Beijing cut the number of fields that are off-limits to foreign investors on its “negative list” to 29 and eliminated market access restrictions for foreign investors in the permitted sectors of manufacturing.

AI leadership through vertical innovation

Perhaps most significant when looking forward, China has positioned itself as a leading force in AI through a distinctive approach to vertical innovation. Unlike Western competitors, who often focus on developing the most advanced models, China has prioritized creating a vertically integrated ecosystem that spans materials, hardware and software.

This strategy dates back to 2017, when Beijing outlined its long-term AI strategy, aiming to become the global leader by 2030. Government funding aligned corporate interests with national priorities, and by 2024, AI had become central to business objectives, consumer behavior and economic growth. Morgan Stanley research projects China’s core AI industry to reach $140 billion by 2030, with related sectors potentially increasing that figure tenfold.

Government funding aligned corporate interests with national priorities, and by 2024, AI had become central to business objectives, consumer behavior and economic growth.

China’s vertical integration approach capitalizes on four key advantages: vast data from its 1.4 billion citizens, an expanding energy supply (with more coal and nuclear power plants under construction than the rest of the world combined), resilient computing capabilities despite U.S. export controls, and human resources (with 47 percent of the world’s top AI researchers and more than 50 percent of AI patents).

Leading Chinese tech companies have embraced this vertical strategy. Tencent invested nearly $9 billion in R&D in 2023 and developed a proprietary large language model, Hunyuan, which has been piloted across more than 600 internal business units. Thanks to its AI solutions and autonomous driving, Baidu, a multinational tech company focused on the internet and AI, secured the second spot in the 2025 China Corporate Technology Index (an assessment of digital transformation and technology adoption of Chinese companies, not an index of publicly traded shares). Xiaomi has developed one of the world’s most extensive AI-powered Internet of Things ecosystems, with half of its workforce dedicated to AI, IoT and innovative hardware development.

Challenges and China’s future outlook

China’s efficiency-driven and low-cost approach creates a different path to return on investment compared to Western competitors. However, this also raises concerns over dumping practices and unfair treatment of workers, even in countries friendly with China or in BRICS member states.

Beijing aims for Chinese AI investments to break even in 2028 and achieve a return on invested capital of over 5 percent by 2030. This focus extends to applications such as humanoid robots, where China’s comprehensive supply chain gives it a significant edge in lowering production costs.

However, not all projections about China align with reality. While the government supports AI, there is limited room for market-driven innovation, as markets play a secondary role behind state security in China’s AI efforts. This is only one of the hurdles ahead.

Despite the stimulus-driven economic resurgence, China continues to face persistent challenges. Domestic consumption remains low despite government efforts, with no signs of structural reforms that could securely and sustainably boost demand. The middle class bears the brunt of the manufacturing-focused strategy, with weak consumption and real estate woes destroying asset values and dampening economic prospects.

Geopolitically, China’s record trade surplus is triggering pushback from global partners, such as the U.S. and the European Union, with trade tensions intensifying under the administration of President Donald Trump. Questions also persist about the reliability of Chinese economic data, with some analysts suggesting figures may overstate actual growth.

Scenarios

Most likely: Chinese clout to grow but still remain behind the U.S.

The most likely scenario for the next few years is that China will maintain its position as a strong global number two behind the U.S. As its capabilities for value-added growth increase, Beijing will persist in challenging Washington economically and politically, yet will remain unable to equal or overtake it. In specific economic sectors, such as energy and AI, China could even become the global leader. Its international initiatives will continue to gain traction, especially as countries worldwide face trade and security pressures under the Trump administration.

Still, China will not supplant the international system established by the United Nations and its agencies, as well as by the U.S.-led formal and informal institutions. The reason China has not ascended to primacy is the CCP. Its top-down leadership over the country and its industries makes learning from markets and international relations difficult, slowing China’s adaptability to economic and international changes.

Possible but unlikely: China becomes the global hegemon

There is a second – possible but unlikely – scenario in which China overtakes the U.S. as the global superpower. In this scenario, economic growth and AI leadership, as well as Chinese-led international institutions, are the reasons for the reversal. For this to occur, however, several somewhat unlikely factors must come into play.

It would be necessary for China to maintain continued economic growth and its emerging leadership in AI while establishing a network of international organizations and initiatives working to Beijing’s benefit. Additionally, China would need an economic crisis in the U.S. that spills over to Canada, Mexico and Europe, to weaken the North Atlantic link and enable the emergence of orthogonal AI – the technology applied to vast realms in everyday life, politics and policy.

Least likely: Chinese policymaking becomes more erratic, hurting stability

In a third, though also unlikely scenario, China stumbles on itself, reverting to its stagnation and decline seen in 2020-2022. In recent years, the CCP has reversed many of its policies. This back-and-forth has already left a negative mark on markets and investors. If such policy reversals intensify, Beijing will be regarded as an erratic partner, which, in turn, leads to a diminished international posture and economic recession due to rising risks without potential benefits.

This scenario would most likely unfold if the CCP attempts to further tighten its grip, fearing a loss of control over the country. What makes this scenario unlikely is that the party has already established control on the Chinese economy and society through the use of AI.

This report was originally published here: https://www.gisreportsonline.com/r/china-challenge-global-leadership/