China reshapes the global automotive landscape

In March 2022, when Prince William and Princess Kate arrived in the Bahamas, their airport motorcade did not feature the usual Jaguars or Rolls-Royces. Instead, it consisted of BYD Tang vehicles.Chinese electric vehicles have moved to center stage at auto shows worldwide. The shift has been striking enough that Jim Farley, chief executive of Ford Motor Company, has repeatedly traveled to China and even brought several Chinese models back for reverse engineering. His objective has been clear – to better understand the country’s technological and cost edge.

Taken together, these developments reflect a broad recognition of China’s growing dominance in electric vehicles, putting Europe’s automakers on alert. At the same time, it is widely acknowledged that this progress has been underpinned by sustained state intervention and non-market or hybrid industrial policies.

China’s rise as the leading automotive exporter

In 2025, China’s automobile exports reached 7.1 million units, a 21.8 percent annual increase that consolidated its position as the world’s largest automotive exporter. The country has now held this lead for three consecutive years, having overtaken Japan in 2023 to claim the top spot.

Backed by a combination of state support and advancing technological capabilities, China has also moved ahead of Japan and Germany in the electric vehicle sector, while narrowing and in some segments surpassing the United States.

China’s strength lies in electric vehicles (EVs). Driven by policy support and the competitive inspirations from Tesla, China’s automotive electrification advanced rapidly. Unlike traditional automakers, which long relied on imported core technologies like engines and transmissions, China leapfrogged development stages in the “three electrics” (battery, electric motor and electronic control systems), securing global leadership.

The adoption of EVs requires not only affordable electricity but also sufficient charging infrastructure. Consequently, in emerging markets, demand for traditional vehicles remains higher than for electric or hybrid vehicles. This dynamic explains why exports of new energy vehicles (EVs and hybrid cars) continued to rise in 2025, but traditional internal combustion engine (ICE) vehicles still accounted for a significant share of total exports.

China’s automobile exporters have become increasingly active in emerging markets in recent years, as trade barriers in the U.S. and Europe have constrained access to developed economies.

More recently, however, the European Union has begun to open its market to Chinese electric vehicles, creating a more complex dynamic that poses strategic challenges for European manufacturers. Looking ahead, China’s automobile exports are set to expand further, supported by competitive pricing, scale advantages and continued policy backing. The Iran war since February 2026 has spurred a new wave of demand in EVs because of the rocketing price of oil. Chinese automakers are likely to view the crisis as further validation of their long-term strategy.

To understand how this expansion unfolds in practice, it is useful to examine two contrasting cases: Russia and Brazil. The former illustrates a rapid, opportunistic market capture driven by geopolitical disruption and short-term supply gaps, while the latter reflects a more deliberate long-term strategy anchored in China’s industrial policy and its urgent need for external market growth. Together, they show the range of approaches Chinese automakers deploy as they scale globally and adapt to different political and economic environments to expand.

Chinese EV exports to Russia

Following the Russian invasion of Ukraine, the withdrawal of Western manufacturers – combined with sanctions-driven disruptions to logistics and finance – created a short-term gap in Russia’s domestic vehicle production. This helps explain why Russia quickly became the largest export market for Chinese automobiles.

Although Moscow has strengthened localization policies since 2023, sanctions and technological constraints have limited tangible progress. Following Moscow’s invasion of Ukraine in 2022 and Western automakers halting deliveries to Russia, Chinese brands rapidly emerged as the primary suppliers in the Russian market. Exports surged from 158,000 units in 2022 to 902,000 units in 2023.

This growth proved short-lived. Exports reached approximately 1.15 million units in 2024 before falling sharply to 579,000 units in 2025, a decline of nearly 50 percent. Several factors explain the reversal. Russian consumers showed limited interest in electric vehicles, while Chinese manufacturers struggled to meet the demands of Russia’s harsh climate and road conditions. Chinese internal combustion engine technologies remain less competitive than those of established automotive producers.

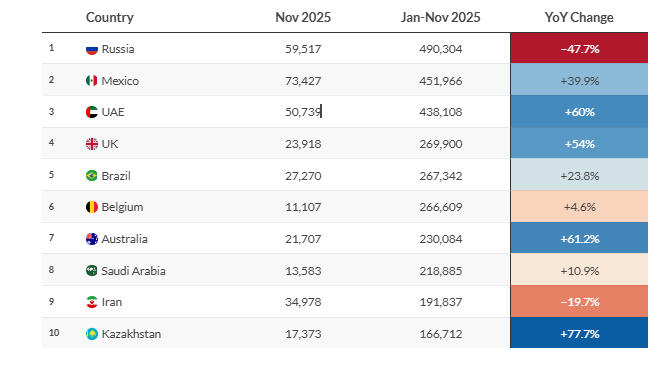

Facts & figures: Exports of Chinese passenger vehicles by country

Despite close political ties, China has consistently avoided transferring core automotive technologies to Russia. Russian policymakers, wary of overdependence on Chinese imports, have responded with a series of restrictive measures. On July 30, 2025, the country’s technical regulator banned several truck models from Chinese manufacturers on safety grounds. The following month, authorities sharply increased recycling fees on imported vehicles to between 70 and 85 percent, significantly eroding price competitiveness.

Additional requirements have further tightened market access. From mid-2025, all imported vehicles must undergo mandatory testing in Russian laboratories and provide documentation confirming integration with the Russian-owned GLONASS satellite navigation system. Parallel import routes via Central Asia have also been curtailed, closing key channels for re-exported Chinese vehicles.

While Russia has encouraged Chinese firms to establish local production with technology transfer, progress has been limited. Sanctions exposure, payment constraints and security risks have reduced the attractiveness of such investments. As a result, Chinese automakers have shown little willingness to meet Moscow’s demands and are increasingly redirecting their focus toward other emerging markets to offset losses in Russia.

Opportunities and constraints in Brazil

For many Chinese automakers, Brazil has evolved from a testing ground into one of their most important international markets, in some cases becoming the primary source of overseas profits. Since 2009, China has been Brazil’s largest trading partner, and the relative stability of bilateral relations has provided a degree of predictability for long-term positioning.

Unlike the surge in Russia, China’s growing engagement with Brazil reflects a structural shift rather than a short-term response. It is driven by changes in global trade patterns and a broader effort by Chinese firms to diversify away from Western markets, reduce exposure to trade friction and expand across the Global Majority. As the world’s sixth-largest automotive market and the largest in Latin America, Brazil has emerged as a key destination, with new energy vehicles at the forefront of this expansion.

China’s initial approach focused on exports, but this has shifted toward apparent localization. In 2025, BYD and Great Wall Motors launched their first passenger vehicle plants in Brazil, while Chery Automobile, present since 2014, is upgrading its facilities and preparing to host additional Chinese brands. This development is gradually reshaping local perceptions of electric mobility.

Following his return to office in 2023, President Luiz Inacio Lula da Silva placed green reindustrialization and the digital economy at the center of Brazil’s economic policy. The objective is to strengthen resilience through industrial upgrading while reducing reliance on commodity exports. Within this framework, localization requirements for foreign automakers have become increasingly explicit.

Brazil has sought to leverage Chinese investment to revitalize its domestic manufacturing base. For years, it maintained zero or near-zero tariffs on electric vehicles, facilitating imports from Chinese brands. However, expectations that market access would translate into substantial technology transfer have not been fully met. As a result, policy has shifted. Since January 2024, tariffs on new energy vehicles have been gradually reintroduced due to the limited localization of Chinese production, with rates set to converge with those for conventional vehicles at 35 percent by mid-2026.

The reluctant shift by Chinese firms toward local manufacturing reflects both regulatory pressure and confidence in market potential. Similar localization requirements have also been imposed by countries such as Algeria and Indonesia. Yet in Brazil, concerns continue to grow despite China’s apparent compliance. Domestic producers and workers recognize the difficulty of competing with China’s scale and cost efficiency, fueling fears of job displacement and industrial erosion.

So far, Brazil has remained cautious about imposing the stringent local content requirements that China itself once applied in the 1980s, partly out of concern that doing so could deter Chinese investment. In contrast, Mexico, under pressure from the U.S., has adopted a more restrictive stance toward Chinese manufacturers. While Chinese firms generally prefer a model based on Chinese components and overseas assembly, future policy in Brazil remains uncertain.

If leadership in Brasilia changes following elections in October 2026, Brazil’s approach could shift toward stricter requirements. Concerns over the impact of Chinese expansion on employment and domestic industry are intensifying, suggesting that today’s relatively open framework may not endure.

China’s expansion strategy, as illustrated by its activities in Russia and Brazil, prioritizes market access over short-term profitability, with the state guiding firms along differentiated paths while retaining strict control over core technology transfer. Exports remain the preferred mode of entry, followed by assembly, with full local manufacturing and supply chain development used only when necessary.

At the same time, Chinese companies are rapidly improving their capabilities, combining cost competitiveness with speed and adaptability. While affordable electric and hybrid vehicles can benefit emerging markets, they also create tensions by undermining domestic industries and embedding Chinese standards, components and dependencies within local economies.

Ultimately, this outward push reflects Beijing’s need to compensate for domestic overcapacity and sustain growth, a dynamic likely to persist unless constrained by stronger policy responses in host countries.

Advances into European markets

Despite notable gains in emerging markets, China continues to prioritize Western developed economies. These markets offer stronger policy support for decarbonization, higher consumer purchasing power and more mature infrastructure, making them structurally attractive for electric mobility.

In 2025, China exported just over 1 million vehicles to the EU, accounting for roughly 6-7 percent of the market, with higher penetration in specific countries and electrified segments. Europe’s proactive stance on the energy transition has created favorable conditions for Chinese electric and plug-in hybrid vehicles, which are gaining market share at a rapid pace.

Efforts to curb this expansion through tariffs have had limited impact. While the EU raised duties on Chinese battery electric vehicles in 2024, exports have continued to grow as manufacturers adjusted their product mix toward hybrids, which were not subject to the same measures. This shift has sustained overall export growth and reinforced China’s position in the European market.

On January 12, 2026, Brussels and Beijing reached a preliminary understanding centered on price commitments for Chinese EV exports, reflecting an attempt to manage trade tensions within the framework of the World Trade Organization while avoiding further escalation.

The EU’s longer-term objective remains to attract Chinese manufacturing investment within its borders, through joint ventures that would facilitate technology transfer – echoing the model China once imposed on foreign automakers. Chinese firms, however, have shown limited willingness to relinquish control over core technologies. On March 4, 2026, the European Commission published the draft Industrial Accelerator Act, a broad legislative initiative aimed at strengthening Europe’s industrial base. If approved by the European Parliament, the proposal could impose the most stringent localization and technology transfer requirements Chinese firms have yet faced abroad.

China operates through coordinated state support and strategic direction, while the EU relies on decentralized corporate responses. As quality differentials narrow, price has become the decisive factor. China’s cost advantage now represents a structural challenge in Western markets, and given the central role of the automotive sector in Europe’s industrial economies, the ability to withstand this pressure will be key in determining the region’s economic trajectory.

Scenarios

Likely: EU automotive sector adapts under pressure

The most favorable outcome for the EU would involve a recalibration of the bloc’s policy. This would need to be paired with accelerated automation or partnership with foreign carmakers to reduce production costs, alongside credible frameworks to support workers displaced by technological change.

Recent developments point in this direction. BMW Group has begun introducing “physical AI” into its European production systems, deploying robots capable of operating continuously with high precision. Even so, such advances are unlikely to close the gap quickly. China is expected to retain a clear advantage in electric vehicles across Europe for at least the next five years. Meaningful technology transfer from Chinese firms is unlikely to occur unless the EU can exert sufficient leverage in negotiations.

Equally likely: Stagnation in China’s expansion and defensive measures

If EU policy remains fragmented, its innovation insufficient, and China successfully resists the EU’s localization requirements, Europe’s existing structural weaknesses are likely to persist. In such a scenario, European manufacturers would struggle to compete on cost, efficiency and technological catch-up. Tariffs would remain the last available policy instrument, though they would offer only partial relief and could trigger further trade friction.

Overall, Europe’s trajectory will hinge on whether it can successfully align industrial policy, innovation and cost structures quickly enough to respond to an increasingly state-backed and price-competitive Chinese automotive sector.