Crack-up boom – the end of a currency regime

A breakdown occurs. The crack-up boom appears. Everybody is anxious to swap his money against “real goods”, no matter whether he needs them or not, no matter how much money he has to pay for them.

Ludwig von Mises

• The term crack-up boom has been trending in the financial media recently.

• The expression gained fame after Austrian School economist Ludwig van Mises wrote about it in his famous treatise Human Action.

• The most prevalent symptoms are hyperinflation in consumer prices and uncontrolled stock market rallies as a flight into real values takes place. Other side effects are disruptions in supply chains and a seizure of the loan markets.

• The end result is typically the loss of trust in a currency, its failure, and the subsequent emergence of a new one.

• Examining all currencies currently in circulation, their average lifespan as of 2023 amounts to approximately 74 years. In comparison, the life of an average S&P 500 company is much shorter, standing at 18 years as of today.

• With the invention of Bitcoin, we are now witnessing a live experiment in monetary invention.

The term crack-up boom has been trending in the financial media in recent years. Impelled by unconstrained inflation and lofty stock price levels, learned investors sought past historical orientation via analogues with the World War II period as well as the 1970s. The term crack-up boom actually has its origin in academic treatises by the Austrian School economist Ludwig von Mises, but it is certainly relevant to the current global economic environment.

Money is a societal institution – with all the weaknesses of human nature

As has been highlighted in great detail in previous In Gold We Trust reports, money is a societal institution serving an economic function, allowing us to obtain the things we need and want in a specialized world. Money is after all uniquely human and it “allows humans to structure life in incredibly complex ways that were not available to them before the invention of money”.1 Thus, the introduction of the usage of coins in ancient Lydia almost three thousand years ago, paving the way for the emergence of a mercantile market system, sparked a revolution.

What began in commerce quickly spread to all other areas of life from politics to religion to academics as the use of numbers and of counting propelled a new level of rationalization in human thought. And even though the Lydian kingdom under Croesus disappeared after its conquest by Cyrus the Great, the new money system prevailed and was a key factor that made possible the classical civilizations of the Mediterranean. The next quantum leap in the history of money was triggered by invention of banking and paper money in the banks of Renaissance Italy, facilitating the capitalist economy as we know it today, while most recently the invention of electronic money added a further dimension to money as a societal institution.

CHOCOLATE AS A CURRENCY

Cacao beans emerged as the primary medium of exchange during the Aztec Empire (1400 AD). In fact, chocolate became so valuable that it was counterfeited by criminals who hollowed out cacao beans and filled them with mud. Cacao was a highly prized commodity in Mexico and Central America which could be traded widely or consumed. Its value was based on the local cultural context because when the first European pirates seized a cargo of cacao beans, “they mistook the cacao beans for rabbit dung and dumped the entire cargo in the sea” (Weatherford). It is often forgotten that currencies can also share beauty (gold) or taste (chocolate)in addition to their economic features of trust, divisibility, portability and standardization.

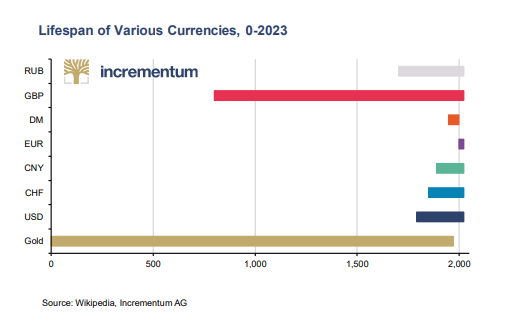

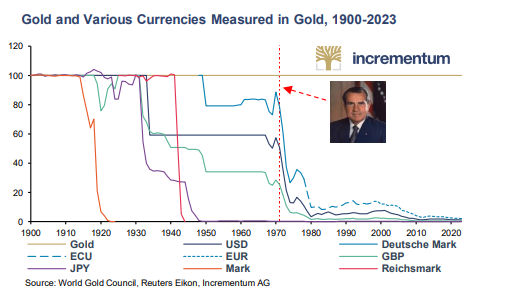

During those 3000 years in the history of money, not only did human culture undergo profound transformations but multiple currency regimes appeared and disappeared. The longest-serving currency in use today is by far the British pound at about 1200 years, albeit at the cost of significant devaluation. While in 1257 one fine ounce of gold stood at GBP 0.89,2 today its price is above GBP 1500. The second and third oldest currencies in circulation, unknown to many, are the Russian ruble and Serbian dinar, both in use since the 13th century. Over the centuries both the ruble and the dinar have undergone numerous devaluations and revaluations. Comparatively young in comparison is the US dollar, which was introduced in 1792 under the Coinage Act passed by the US Congress. The Swiss Franc is even younger, being introduced in 1850 by the first Federal Coinage Act of the new Swiss Federal Constitution. Still in its infancy is the euro, which was launched only in 1999 by the European Central Bank. Nevertheless, since then its currency has devalued by 85% when measured against gold. In other words, the price of gold in euro terms has increased by 555% since the euro’s inception.

Most currencies are very young

Paper money eventually returns to its intrinsic value – zero.

Voltaire

The realization of how short-lived most currency systems are leads usto the question of how and why a currency system will not only emerge but, more importantly, end. For some time, an internet meme circulated that the average lifespan of a fiat currency amounted to only 27 years. However, as critics pointed out, this was taking into account only currencies that are no longer in circulation. Examining all currencies currently in circulation, their average lifespan as of 2023 amounts to approximately 74 years (own calculation). In comparison, the life of an average S&P 500 company is much shorter, standing at 18 years as of today.

Regarding the end or “death” of a currency, three scenarios come to mind. First, it may occur upon conquest by a foreign power, whose currency is subsequently imposed. One example for this is the so-called Japanese invasion money, officially known as Southern Development Bank Notes, which was introduced to occupied countries by Japan during World War II. Or a

currency may die through the introduction of a new currency due to political reasons such as the advent of the euro, which replaced the existing currencies in the participating countries of the newly established currency union, including the German mark, the Italian lira, and the French franc. Lastly, perhaps the most infamous scenario is currency failure, most often in the form of hyperinflation.

Currency, whether composed of paper cash, coins, or an electronic ledger, is simply an ephemeral form of money of money that is popular and useful in a location for a limited period of time. Gold and silver are money, too, but they are of a different sort, often referred to as metallic standards. All currencies are finite, and some have had very short life spans. With the invention of Bitcoin and other cryptocurrencies, we are now witnessing a live experiment in monetary invention, and it will be interesting to observe how it will play out over the course of the next decades.

As per Wikipedia, a currency is “a standardization of money in any form, in use or circulation as a medium of exchange, for example banknotes and coins” or more generally, “a system of money in common use within a specific environment over time, especially for people in a nation state”. Since 1978 the International Organization for Standardization (ISO) has published ISO 4217, a standard encompassing every world currency by means of the ISO 4217 Currency Code.

One great advantage of money is its function as of a generally accepted unit of account. Economic calculation, encompassing everything that is exchanged against money, becomes possible. Thus, prices of goods and services became denominated in money, either units of gold and silver or the prevailing currency. Today, all prices are denominated in fiat currencies – the euro, US dollar, pound sterling , yen – with the US dollar serving as the reference value for all other currencies.

In his What Has Government Done to Our Money, Murray Rothbard pointed out, “Money [currency] does not measure prices or values; it is the common denominator for their expression. In short, prices are expressed in money [currency], they are not measured by it”.

If a currency becomes too volatile or loses trust in its redeemable value, it can no longer serve as money. To fulfill its economic function as a medium of exchange, unit of account and store of value, a currency necessarily needs to have a minimum level of trust and stability. Today, most central banks in their role of issuers of respective national currencies, have adopted a technique called inflation targeting, with a depreciation target of 2%. This 2% target is widely considered to be low enough in volatility and implied trust (against depreciation or counterfeiting) to keep the currency viable as a form of money. However, when the inflation rate rises over 2%, it becomes difficult for economic actors to make productive and rational decisions, and central banks may fear a bank run on their national currency.

Hyperinflation – the failure of a currency

Plenty of examples exist, however, of currencies failing their prescribed function sooner or later. The most extreme examples fall into the category of hyperinflation, whose initial definition, by Phillip Cagan, is still widely used: “[B]eginning in the month before the monthly rise in prices exceeds 50 per cent and ending in the month before the monthly rise in prices drops below that amount and stays below for at least a year”.3 A monthly inflation rate of 50% is equivalent to an annual rate of 12,975%. For reference, the annual inflation rate at the end of 2022 was 64% in Turkey, 95% in Argentina, 156% in Venezuela, and 244% in Zimbabwe.

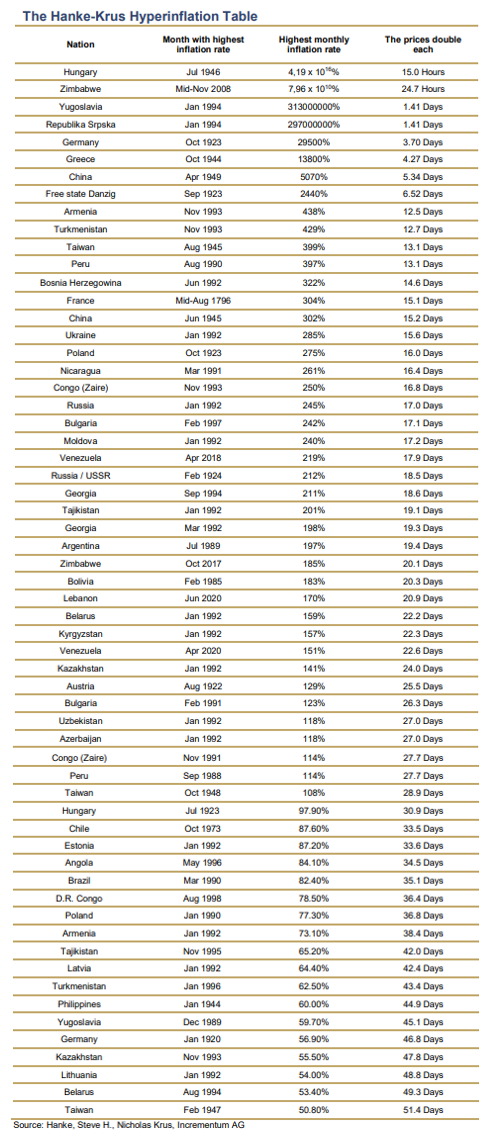

Steve H. Hanke, Professor of Applied Economics at John Hopkins University, has further refined Cagan’s definition of hyperinflation as “inflation in which the inflation rate exceeds 50% per month for at least thirty consecutive days”. Based on this refined definition, Hanke and Nicholas Krus created the so-called HankeKrus hyperinflation table. This was first published in 2013;4 as of January 2023, it comprises the following episodes:

The most egregious current example of hyperinflation is found in Zimbabwe, where consumer price inflation reached 285% year-on-year in August 2022 but had fallen to a tidy 75% by April 2023. Venezuela, Argentina, Turkey, and Lebanon might also come to mind when thinking about hyperinflation environments; however, as of 2023 their rates lie below 50% and thus do not meet the criteria of Cagan and Hanke. Nevertheless, people in those countries are facing huge challenges due to the ongoing devaluation of their currencies. In the case of Lebanon, the Banque du Liban (the central bank of Lebanon) repegged the value of the Lebanese pound against the US dollar at the opening of 2023, thus devaluing the currency by about 90%.

Yet, this new exchange rate is still far off the black-market rate, by which many people in the country trade and calculate.

Notably, all of the above examples, occurred in the presence of discretionary paper money regimes and were caused by government budget deficits that were financed by excessive currency creation.5 However, the final trigger of an unconstrained accelerating inflation rate is adverse political and societal conditions, rather than the absolute level of credit creation.

The crack-up boom

The Austrian School of Economics is particularly well known for their research into money and price theory. Thus, it should come as no surprise that Ludwig von Mises bears responsibility for coining the moniker crack-up boom, or Katastrophenhausse in German, although earlier mentions of the German expression can be found, such as for example in Moriz Dub’s 1922 article “Die weitere Entwicklung der Katastrophenhausse in Oesterreich mit Streiflichtern auf Deutschland” (“The further development of the catastrophe boom in Austriawith spotlights on Germany”).6 Mises, having lived through the crisis years of the 1920s and 1930s in Austria, which were similar but prior to the developments in Weimar Germany, was deeply aware of the distortionary effects of the artificial provision of money and credit to the economy. The 100-year anniversary of the German hyperinflation this year could be reason enough on its own to reinvestigate the topic.

Artificially inflating the supply of money will result in a drop in interest rates, misleading investors to invest in projects that appear profitable even though they are not. As banks continue to pour credit into the economy, prices and wages as well as asset prices will rise, giving the false impression of strong economic growth. At the same time, the inherent problem of misallocated capital persists. The longer the credit expansion lasts, the greater the distortions in the overall economy become. Unprofitable business ideas are pursued, and nonproductive individuals are rewarded. In today’s terms, we would speak of the zombification of the economy.

Contrary to most economists, scholars in the tradition of the Austrian School of Economics consider the artificial boom triggered by central banks’ downward manipulation of interest rates as a worrisome process of bringing an economy out of balance, while the ensuing recession is the unavoidable process of returning the economy into balance. This wave-like development of the economy must not be confused with secular growth, which depends on the quantity of real savings available in an economy.

Various scholars have written about the consequences of this distortion. They all arrive at the same conclusion: Sooner or later the correction will come. It will certainly come once the credit expansion is no longer accelerating any further and market participants begin to struggle to service their debt. When the private misallocations of capital become exposed, oftentimes government attempts to intervene by bailing out companies and keeping the credit expansion going through quantitative easing, i.e., outright purchase of bonds, or credit easing, the loosening of the financing conditions for commercial banks. Amongst the most recent examples are the Targeted Long Term Financing Operations (TLTRO) of the ECB, with the explicit goal of “preserving favorable borrowing conditions for banks and stimulating bank lending in the real economy”. The unwillingness of both private and government actors to acknowledge an investment loss leads to an absurd level of credit expansion. The expansion continues with the reckless printing of money until the entire economic system collapses in a crack-up boom.

While Mises clearly has brought fame to the moniker crack-up boom, his definition was somewhat vague, placing the phenomenon in the context of a rapid fall of purchasing power triggered by credit expansion and resulting in a flight into real goods: “The monetary system breaks down; all transactions in the money concerned cease; a panic makes its purchasing power vanish altogether”.

Thus, and contrary to common assumptions, for Mises the crack-up boom really described the overall breakdown of the economy caused by “the panic of the currency catastrophe”, which goes far beyond the panic rally on stock markets, although this constitutes one of the various symptoms of the currency breakdown. In Weimar Germany, the government even had to respond to the ensuing chaos by issuing a “state of siege”. In general, the ceasing of the functioning of the economy can be observed in the following areas:

- Loan markets: Interest rates rise rapidly, well above any level of entrepreneurial investment.

- Asset price boom: Inflation of asset prices surges above any historical performance levels of cash-flow.

- Supply chains: Seizure of B2B transactions, the supply chains stop

functioning, and intermediate goods become scarce. - Consumer prices: runaway inflation causing disorientation (hyperinflation).

Hyperinflation is the easiest symptom of the breakdown of the currency system to observe and measure. Published consumer prices are much easier to observe than supply chain disruptions, scarcity of intermediate goods, and loan denial. Furthermore, everyone holding the currency is directly exposed to hyperinflation. Therefore hyperinflation is the most common financial symptom associated with a crack-up boom, but it is clearly not the only economic symptom.

Murray Rothbard described the resulting behaviour as follows: “A frantic rush ensues to get rid of money at all costs and to buy anything else. In Germany, this was called a ‘flight into real values’. The demand for money falls precipitously almost to zero, and prices skyrocket upward virtually to infinity”.

At this stage, “the increase in the quantity of money causes a fall in the demand for money”, as Mises explained in his magnum opus Human Action. This also indicates the loss of trust in the currency. As a further consequence of the rapid fluctuations in prices, other forms of exchange, such as barter, begin to fulfill the former role of the dead currency. Oftentimes, other currencies will be adopted as substitute currencies.

The second most associated symptom of a crack-up boom is probably the explosion of asset prices – in particular stock prices – and the term crack-up boom is used to denote precisely those astronomical and skyrocketing price increases, although Mises used the expression to encompass the overall breakdown of the currency system.

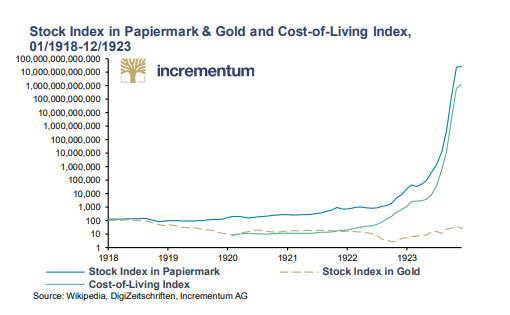

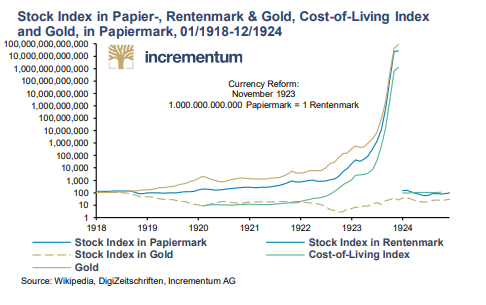

The development of the German equity index in the 1920s is infamous. It increased from roughly 100 at the beginning of the year 1918 to 26,890,000,000,000 at the end of 1923. Notably, when measured against gold, the German equity index, in the run-up period to the hyperinflation as well as in its initial phase (until autumn 1922), lost value in real terms, and only increased again in the later course of the hyperinflationary destruction of the paper mark.

To give a specific example, the stock of Siemens-Schuckert (since 1966 Siemens AG) stood at 216 as of July 25, 1914. By September 1921 it had increased to 4,650, and only a few weeks later, at the end of November 1921, it had reached 14,000. In US dollar terms, however, the valuation of the stock remained almost unchanged.7

The search for value drives asset prices up, fueled by fear and despite a dire economic environment. Contemporary witness reports of the runup to the German hyperinflation are highly illustrative. Notable are the descriptions of Moriz Dub, who already in 1920, in the aftermath of World War I, had observed an inverted correlation between the devaluation of the currency and the stormy upward movements on the German and Austrian stock exchanges.8 Only two years later, he attested a further intensification of what he described as a “peculiar dynamic”. In particular, he emphasized the general interest in stock market movements, a generally low disposition towards saving, a scarcity of goods, and a redistribution of wealth within society from the poor to the rich.

These observations perfectly herald the German hyperinflation – or crack-up boom – of 1923. While in 1914 the US dollar was valued at 4.20 German Reichsmarks, by 1922 the Reichsmark had declined to only 1/1000 of its prior value, before, in November 1923, trading at 4.2 billion Reichsmarks to the US dollar. Behind this absurd and disastrous devaluation of the currency was the Reichsbank, then the German central bank, which acceded to the clamor for ever more money in response to the accelerating prices.

Reichsbank director Rudolf Havenstein explained the ever-growing pressure the Reichsbank faced in running its currency printing press absolutely at capacity: “The wholly extraordinary depreciation of the mark has naturally created a rapidly increasing demand for additional currency, which the Reichsbank has not always been able to fully satisfy. A simplified production of notes of large denominations enabled us to bring ever greater amounts into circulation. But these enormous sums are barely adequate to cover the vastly increased demand for the means of payment, which has just recently attained an absolutely fantastic level, especially as a result of the extraordinary increases in wages and salaries. The running of the Reichsbank’s noteprinting organization, which has become absolutely enormous, is making the most extreme demands on our personnel.”9

Bresciani-Turroni described the feverish situation with the German stock exchange: “It was in the autumn of 1921 that business on the German Bourse reached such a condition as to put in the shade even the classical examples of the most violent fever of speculation. The technical equipment of the German exchanges was insufficient for the increasing mass of transactions.”

And Moriz Dub observed: “In the price sheets we find shares which have remained without yield for years and yet have the highest ratings. Imagination takes the place of calm calculation.”10

Less obviously visible is how an unpredictable, risky environment sooner or later affects credit markets and private lenders of money, who become more and more cautious, demanding higher interest rates, provided they are still willing to lend at all. Even Karl Marx noted that “The rate of interest reaches its peak during crises, when money is borrowed at any cost to

meet payments”. As a result the loan and capital markets will shrink in volume and duration, further harming the already weak economy. For example, in Germany in 1922 “a scarcity of the means of payment began to be felt […]Deposits in the banks diminished rapidly because of the progressive depreciation of German money. That obliged the banks to restrict credits”. In another example, during the hyperinflation in Argentina in the 1980s, credit markets with a duration longer than 14 days simply ceased to exist.11

The disruptions and frictions can persist in the economy for a long time. As Mises explains, “The wavelike movement affecting the economic system, the recurrence of periods of boom which are followed by periods of depression, is the unavoidable outcome of the attempts, repeated again and again, to lower the gross market rate of interest by means of credit expansion. There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of a

voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.”

However, once a threshold is reached, the crack-up boom ensues. Everybody is anxious to swap his money against “real” goods, no matter whether he needs them or not, no matter how much money he has to pay for them. Within a very short time, within a few weeks or even days, the things that were used as money are no longer viable as media of exchange. They become scrap paper. Nobody wants to give away anything against them.

Conclusion

Money is a societal institution, facilitating human interaction and collaboration. Currencies, in the form of coins and paper bills, as well as deposit money, constitute the most widely used form of money today. However, their eligibility for artificial credit expansion makes the economies in which they operate highly vulnerable to the resulting economic distortions, such as volatile prices, interrupted supply chains, and dried-up markets. Eventually, too-great distortions will impede the functioning of the economy. This, then, is the crack-up boom. The most commonly observed symptom of the crack-up boom is its monetary expression, hyperinflation, although there are many other forms of economic malaise, such as a seizure of the credit and investment markets and disruption of supply chains of goods and services. The end result is typically the loss of trust in a currency, its failure, and the subsequent emergence of a new

one.

According to Mises, throughout the early stages, the path towards a crack-up boom can still be abandoned by stopping all further credit expansion and allowing for self-correction of the distortions in the economy. Otherwise, “hitting rock bottom” can only be postponed but not avoided. On a more positive note, as the Manchester banker John Mills pointed out so perceptively, “As a rule, panics do not destroy capital, they merely reveal the extent to which it has previously been destroyed by its betrayal into hopelessly unproductive work”.

Despite the recent surge in awareness of the potential for a crack-up boom, it still needs to be highlighted that current inflation rates, albeit elevated, lie far below the dangerous territory of what is considered hyperinflation. At the same time, however, there is observable friction in our monetary set-up, and more challenges likely lie ahead. This was even acknowledged by the IMF in its January 2023 World Economic Outlook Update: “The balance of risks remains tilted to the downside…[…] the global economic outlook has deteriorated materially”.

ABOUT THE AUTHORS

Ronald-Peter Stöferle, CMT

Ronnie is managing partner of Incrementum AG and responsible for Research and Portfolio Management. He studied business administration and finance in the USA and at the Vienna

University of Economics and Business Administration, and also gained work experience at the trading desk of a bank during his studies. Upon graduation he joined the research department of Erste Group, where in 2007 he published his first In Gold We Trust report. Over the years, the In Gold We Trust report has become one of the benchmark publications on gold, money, and inflation. Since 2013 he has held the position as reader at scholarium in Vienna, and he also speaks at Wiener Börse Akademie (the Vienna Stock Exchange Academy). In 2014, he co-authored the international bestseller Austrian School for Investors, and in 2019 The Zero Interest Trap. He is a member of the board of directors at Tudor Gold Corp. (TUD), and Goldstorm Metals Corp. (GSTM). Moreover, he is an advisor to Matterhorn Asset Management, a global leader in wealth preservation in the form of physical gold stored outside the banking system.

Mark J. Valek, CAIA

Mark is a partner of Incrementum AG and responsible for Portfolio Management and Research. While working full-time, Mark studied business administration at the Vienna University of Business Administration and has continuously worked in financial markets and asset management since 1999. Prior to the establishment of Incrementum AG, he was with Raiffeisen Capital Management for ten years, most recently as fund manager in the area of inflation protection and alternative investments. He gained entrepreneurial experience as co-founder of philoro

Edelmetalle GmbH. Since 2013 he has held the position as reader at scholarium in Vienna, and he also speaks at Wiener Börse Akademie (the Vienna Stock Exchange Academy). In 2014,

he co-authored the book Austrian School for Investors.

Incrementum AG

Is a boutique investment and asset management company based in Liechtenstein. Independence and self-reliance are the cornerstones of our philosophy, which is why the five partners own 100% of the company. Our goal is to offer solid and innovative investment solutions that do justice to the opportunities and risks of today’s prevalent complex and fragile environment.

https://www.incrementum.li/en

This material was originally published here: https://ingoldwetrust.report/nuggets/crack-up-boom-the-end-of-a-currency-regime/?lang=en

——————————————————

1 Weatherford, Jack: The History of Money – From Sandstone to Cyberspace, Crown Publishers Inc., 1997, p 43

2 Weale, Martin: “1300 Years of the Pound Sterling”, National Institute Economic Review, No. 172 (2000): 78–89, p. 78

3 Cagan, Philip: “The Monetary Dynamics of Hyperinflation”, in: Friedman, M. (Ed.): Studies in the Quantity Theory of Money, The University of Chicago Press, Chicago, 1956, pp. 25-117, p. 25

4 Hanke, Steve H. and Krus, Nicholas: „World Hyperinflation“, in: Parker, Randall and Whaples (Hg.): The Handbook of Major Events in Economic History, 2013, pp. 367–377. Steve Hanke and John Greenwood were probably the first ones, by using the Quantity Theory of Money, to accurately forecast where inflation was going to go in the United States. On July 20, 2021, they wrote in “Too Much Money Portends High Inflation” that “the year-over-year inflation rate will be at least 6% and possibly as high as 9%”. They were pretty close. The peak was 9.1% per year. Tehy also got the downside. In their February 14, 2023 op-ed, “High Inflation Will End Soon,” they used the Quantity Theory of Money, a theory that has been cancelled by Powell and the Federal Reserve, to conclude that “we think inflation is knocking on death’s door and a recession may be on the way.” Also, they put, as they always do, specific numbers on our forecast. They concluded that the year-over-year inflation rate would fall to between 2% to 5% by the end of 2023. They could be the only ones that have put numerical values on a forecast, a forecast that looks like it’s going to hit the bullseye.

5 Bernholz, Peter: Monetary Regimes and Inflation – History, Economic and Political Relationships, Edward Elgar,

2003, pp. 19, 69, 73

6 Dub, Moriz: “Die weitere Entwicklung der Katastrophenhausse in Oesterreich mit Streiflichtern auf Deutschland“ (“The further development of the catastrophe boom in Austria with spotlights on Germany“), in: Finanz- und Volkswirtschaftliche Zeitfragen, Heft 80, 1922

7 Dub, Moriz: “Die weitere Entwicklung der Katastrophenhausse in Oesterreich mit Streiflichtern auf Deutschland“ (“The further development of the catastrophe boom in Austria with spotlights on Germany“), in: Finanz- und Volkswirtschaftliche Zeitfragen, Heft 80, 1922, p. 10

8 Dub, Moriz: “Die weitere Entwicklung der Katastrophenhausse in Oesterreich mit Streiflichtern auf Deutschland“ (“The further development of the catastrophe boom in Austria with spotlights on Germany“), in: Finanz- und Volkswirtschaftliche Zeitfragen, Heft 80, 1922, p. 7

9 Havenstein, Rudolf: “Address to the Executive Committee of the Reichsbank, August 25, 1923”, translated in: Ringer, Fritz K. (ed.): The German Inflation of 1923, New York: Oxford University Press, 1969, p. 96

10 Dub, Moriz. 1922, Die weitere Entwicklung der Katastrophenhausse in Oesterreich mit Streiflichtern auf Deutschland, S 6 in: Finanz- und Volkswirtschaftliche Zeitfragen, Heft 80, 1922, Verlag von Ferdinand Enke in Stuttgart

11 Bernholz, Peter: Monetary Regimes and Inflation – History, Economic and Political Relationships, Edward Elgar,

2003, p. 93